When interest rates are high and the broader stock market feels top-heavy, income-oriented investors almost always migrate toward the hidden corners of private credit. But let’s be crystal clear about this. They often migrate there because someone in the professional advisory space directed them to it. And the vehicle of choice is usually the VanEck BDC Income ETF (BIZD).

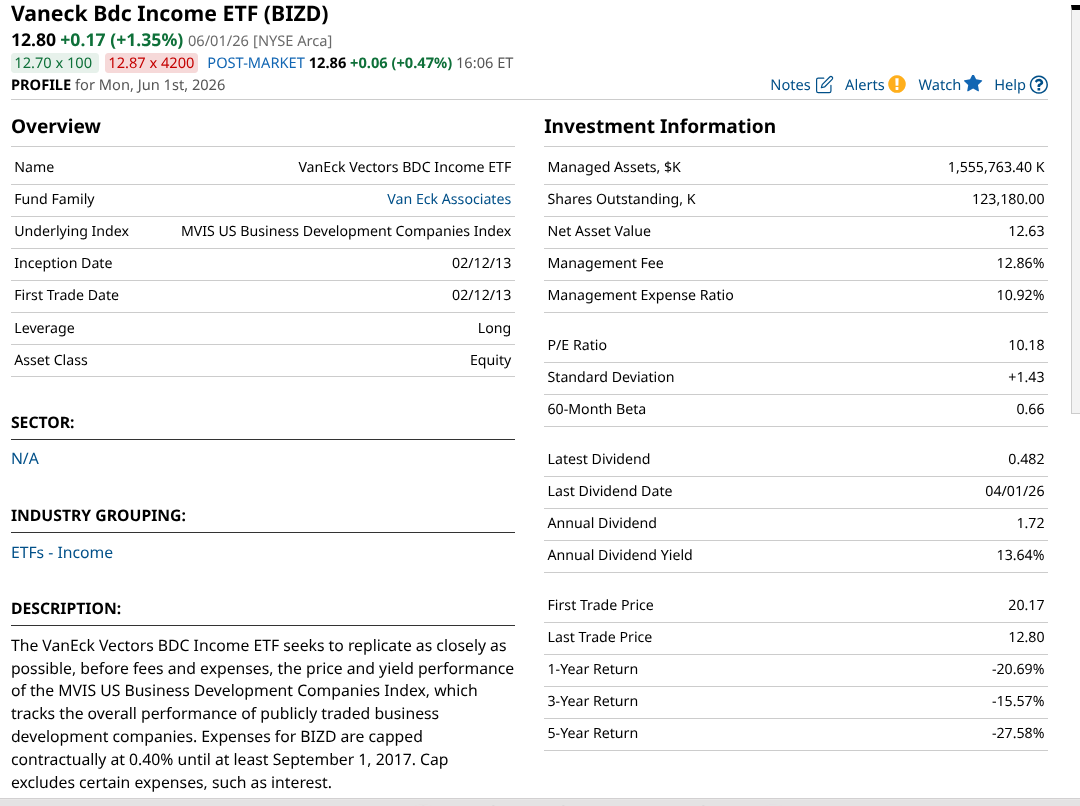

BIZD tracks business development companies (BDCs), publicly traded entities that function as closed-end investment funds, lending capital directly to middle-market private corporations. Because BDCs are legally mandated to distribute at least 90% of their taxable income to shareholders, BIZD currently pays a dividend distribution yield of over 13%.

But looking past that hefty dividend reveals a sector under severe pressure. BIZD is down roughly 10% year-to-date

The primary credit rating agencies, including Fitch Ratings, have officially shifted their 2026 sector outlook for BDCs to “deteriorating.” The easy money in private credit has been made, and the industry has entered a much more complicated, high-risk phase. That word, deteriorating, looks more like an understatement every week.

In part, that’s because BDCs have enjoyed a golden era so far this decade. That’s common in the financial markets. It is often dawn before it gets very, very dark.

BDCs lent money to mid-sized corporations using floating-rate senior secured loans. There was a time in my career where those loans were considered the next best thing to cash. Back in my advisory days, I actually used a senior loan ETF as a bond surrogate, as they paid a more reasonable yield. However, as is often the case on Wall Street, they became too popular. That produced some nice returns for a while, but the market is no longer as safe as it was during those lower leverage years. There’s just too much liquidity moving around to make me comfortable with that type of loan. High return potential? Sure. High risk? Very sure!

As the Federal Reserve jacked up interest rates, the rates on those loans automatically rose, handing BDCs record-high net investment income (NII). But more recently, that mechanical tailwind has completely reversed. Recent interest rate cuts are flowing straight through to the loans, aggressively pressuring BDC earnings and shrinking their dividend coverage. And there’s no urgency for the Fed or the bond market to reduce that rate situation any time soon. This adds heightened risk.

Furthermore, the industry just hit a dubious milestone in the non-listed sector.

For the first time in history, quarterly redemption requests ($6.9 billion) exceeded new fundraising ($4.9 billion). This means liquidity is tightening across the space. That, in turn, forces managers to increase their use of more expensive secured credit lines, right at the time a huge amount of unsecured corporate debt matures.

Why isn’t the market concerned about this? I have no idea! But as is the case with modern markets, issues build up well beyond the point of reason. That’s why calling tops, which used to be a brave investor’s game, is now a useless exercise for all.

Despite the industry headwinds, a bullish path remains for BIZD, entirely dependent on market consolidation and a revival in corporate deal-making. Private equity firms are currently sitting on mountains of unused capital. If corporate mergers and acquisitions (M&A) pick up steam later in 2026, deal flow will surge. This gives BDCs an immediate opportunity to originate high-quality, fresh loans on favorable terms.

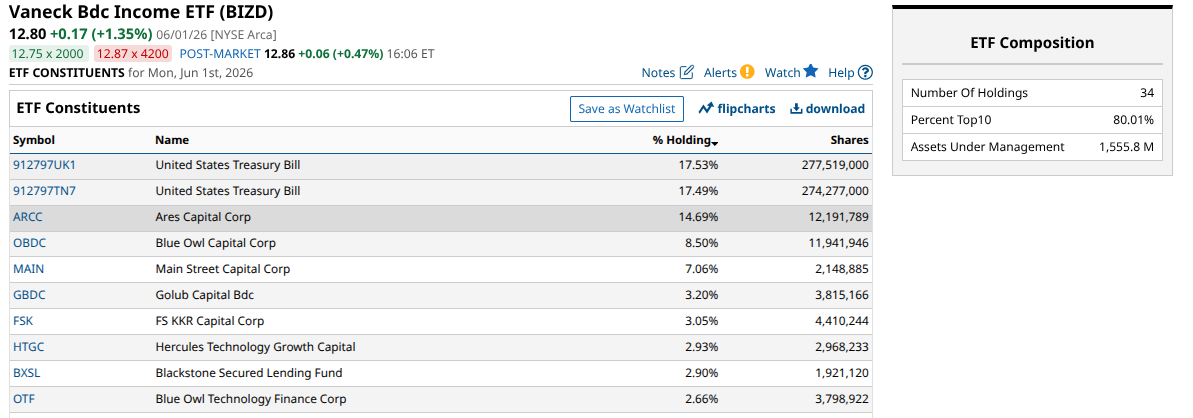

And, the major players whose stocks sit at the top of BIZD are not small, reckless lenders. They are institutional firms with scale and deal flow coming to them. That may explain why the above technical chart is hanging in there, even looking at a possible mini bounce.

The bearish case for BIZD is a straightforward exercise in corporate credit gravity. Middle-market private companies are reaching their breaking point. Years of restrictive interest rates have permanently eroded their cash reserves, and the credit metrics are flashing severe warnings. So-called non-accruals (loans where the borrower has completely stopped making interest payments) are rising well above historical averages.

Then there’s the fees attached to investing in these vehicles. Due to complex SEC disclosure rules regarding “Acquired Fund Fees and Expenses” (AFFE), BIZD’s total expense ratio is… get this… 9.7%. While this includes the internal operating costs of the underlying BDCs rather than a direct fee subtracted from your brokerage account, it highlights just how capital-intensive and expensive private credit management truly is. And it reminds us that BIZD is far from trafficking in the blue-chip space. It is essentially mining for opportunity by levering up smaller companies.

What’s the next shoe to drop here? It could be that some of these stocks cut their big dividends. Or that they blunt their upside by having to reserve capital for distributions. And, there’s my “not-so-conspiracy theory” regarding the trio of headliner IPOs coming up. When Spacex, OpenAI, and Anthropic are all public companies, will that mark the end of this cycle? Put a bookmark on that one for now, and watch BIZD as a sentiment indicator for the market overall.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob’s written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)