Howdy market watchers!

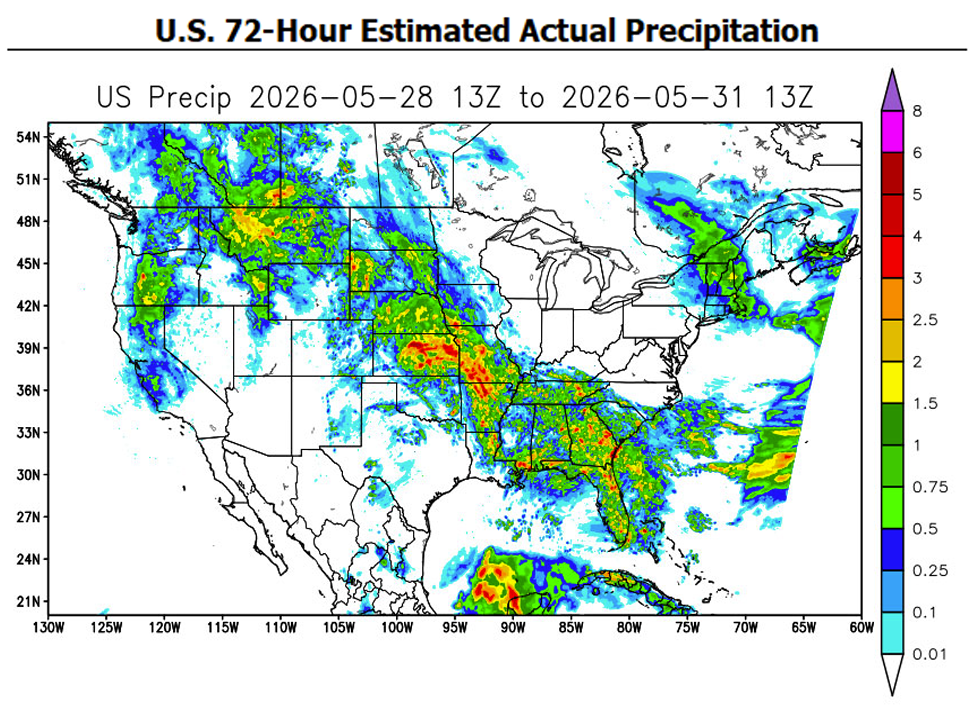

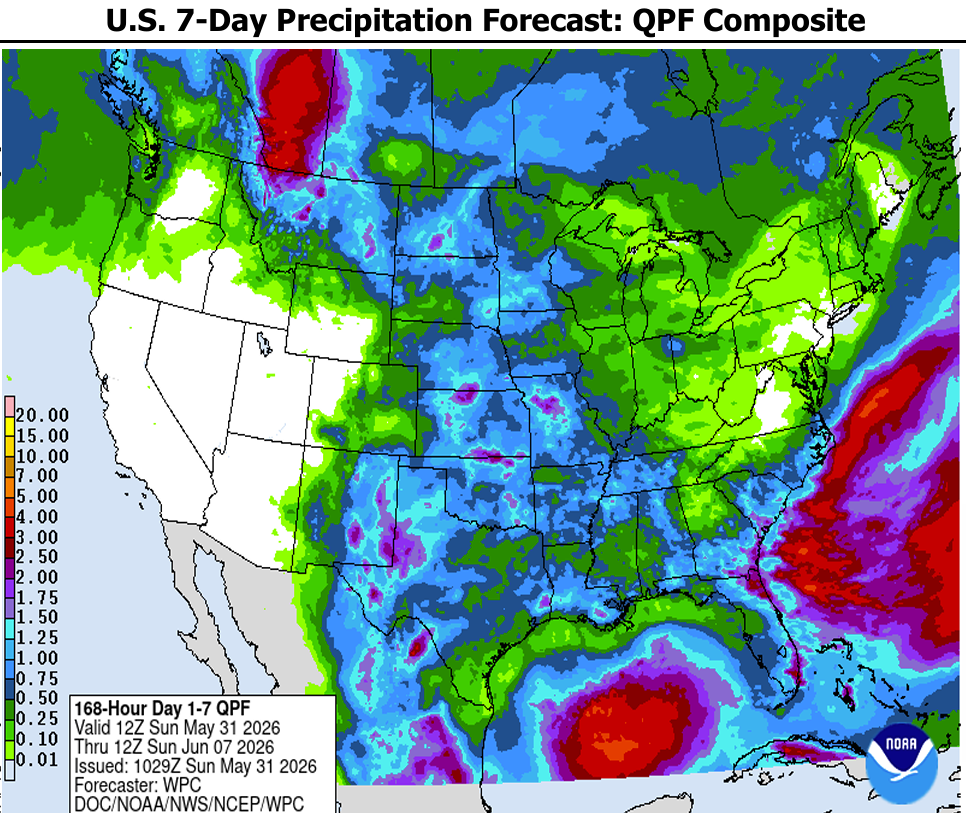

We are very thankful for the rain. While there is much more needed before meaningful drought relief can be achieved, it is a great start and a reversal of the ever dryer trend.

At the beginning of this month, I was expecting to have weeks of thorough wheat harvest reports with commentary that harvest was mostly complete before the beginning of June. However, here we sit along with the combines, with very limited acres cut. There is plenty of ripe wheat in the field, but rain, though welcome, and humidity have kept moisture high unless there was disease or freeze damage or grazed acres. And there is more rain on the way!

In the USDA’s weekly crop conditions and progress report as of May 24th, but released on Tuesday due to markets being closed for Memorial Day Monday, winter wheat ratings were again reduced to 26 percent, one percent below the prior week and two percent below expectations that were calling for a slight increase. The bulk of the decline was in the Pacific Northwest while conditions in the Great Plains stabilized, but at historically low levels.

Normally, precipitation in mid-to-late May is ideal for winter wheat, but continued moisture at this point can begin to lower test weights. While the corn, soybeans and grass pastures are thriving from recent rains, we need a dry window to get wheat out of the field. Yields and quality will be highly variable this year with a lot of very poor in contrast to pockets of good yields and test weights. Protein may be high across the board with the stress this crop has endured.

Regardless of your situation, I would recommend getting your seed wheat reserved now for planting this fall. There are many areas with low to no seed wheat available and so demand will likely be high in all areas.

Spring wheat planting is now 86 percent complete, slightly below expectations, but ahead of average. Corn planting is also at 86 percent, three percent below expectations likely due to rain, but also ahead of average. Soybean planting has also lagged expectations at 79 percent versus 82 percent, but well ahead of the 68 percent average. Suffice it to say, there is no extra premium for planting delays in this market although we have heard some replanting will take place due to recent heavy rains. The first corn, soybean and spring wheat crop ratings will be released in next week’s USDA reports on Monday at 3 PM CDT.

There has been very little love for agriculture commodities since the oil markets peaked on May 18th. The relentless news cycle of on-again, off-again peace and trade deals with Iran, China and Russia and domestic policy have resulted in a significant level of volatility creating exhaustion among fundamental producers and users throughout the supply chain.

The recent rally, especially in the wheat market made US origin relatively expensive on the world market amidst a historically low new crop wheat crop that is about to be harvested. With harvest delayed, but getting underway, there is the typical harvest pressure, but weakness in crude oil and a steady, firm US dollar as inflationary pressures persist.

While lower crude and fuel prices will begin to relieve some pressure, the volatility and uncertainty will not. We’re also hearing more about declining reserves around the world as countries replace high priced, limited supply imports with domestic reserves to cushion the full impact from their economies. However, this strategy has a time limit as reserves dwindle.

All week and again on Friday, President Trump posted about a deal being imminent as the major aspects having been largely negotiated and “agreed.” There was news on Friday of President Trump going into the “Situation Room” with other leadership for a “final determination” that so far has not been announced.

While the Iranian regime indeed needed dismantling, seeing it all the way through is going to be more complicated and take more time and resources than is desired by many American voters given higher priority topics closer to home that are more immediate and personal. We will just have to see what comes of the Memorandum of Understanding that is apparently being circulated and negotiated. President Trump is rightly concerned that any agreement is not reneged on by Iran later and at potentially an even more critical time in the election cycle. I believe that is going to be the most difficult aspect given the threat of further attacks and prolonged involvement by US forces may be more unpopular in the US than its threat to the Iranian regime.

Between these negotiations and the resulting movement in oil prices and weather, the grain markets could remain under pressure despite export strength until these other factors turn supportive.

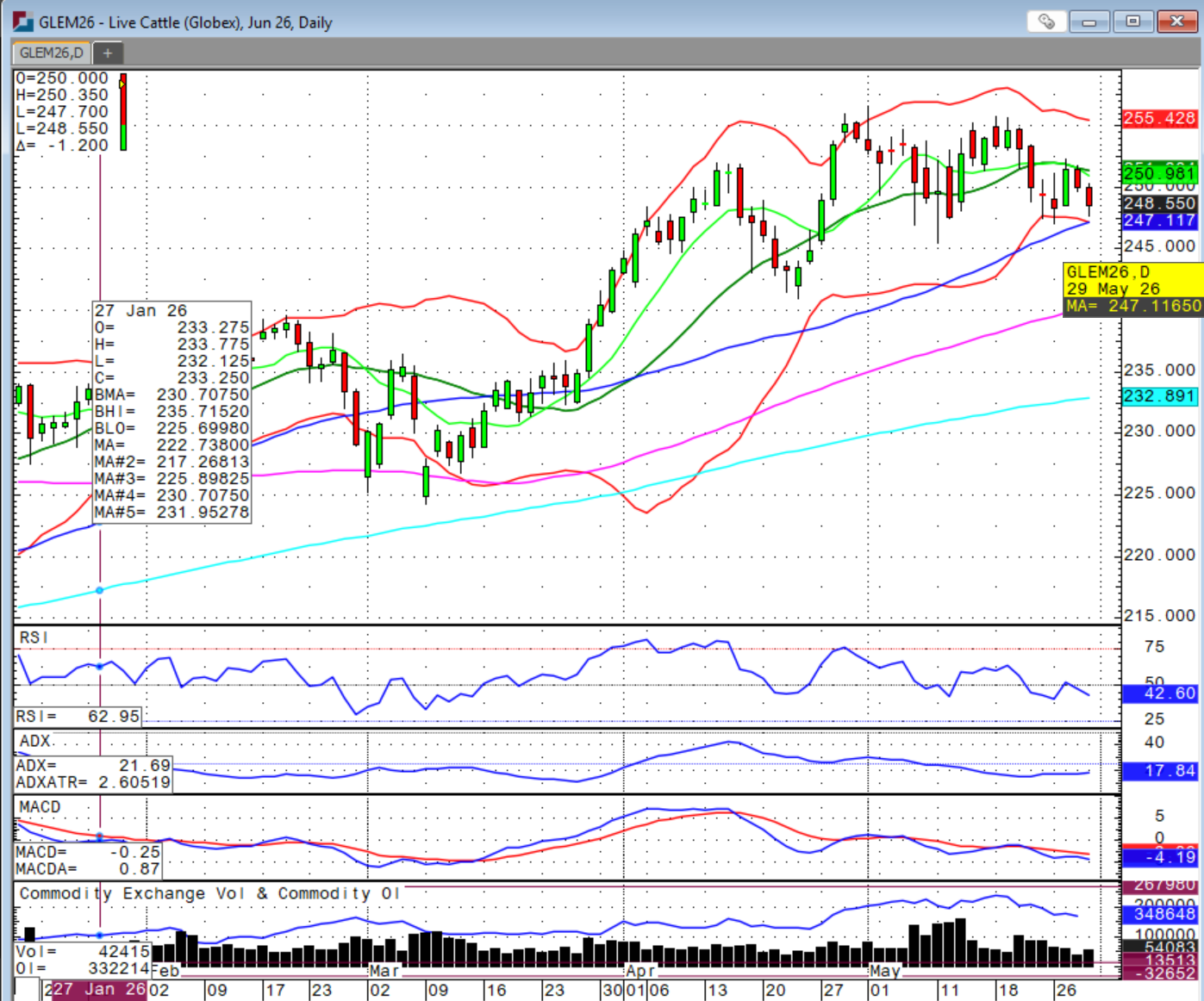

The cattle markets managed to find some support in the shortened trading week despite last Friday’s bearish Cattle-on-Feed reports. Interestingly, the chart gap above on feeders remains unfilled despite getting extremely close to filling on Wednesday. Despite Friday’s weakness, we held above last Friday’s low and believe we could see a rebound next week. Friday was the end of the month in addition to the week and I believe that was part of the pressure although the primary contributor was the detection of the nearest New World Screw Worm case to the US border. On Friday, the USDA announced that a case of the NWSW was found in Mexico, just 31 miles from the US border. With warmer temperatures here and cases getting closer, it is near inevitable that we will see a case in the US at some point in the future, as much as I hate to say it. Link to story: Flesh-eating screwworm found within 31 miles of US border, says USDA | Reuters

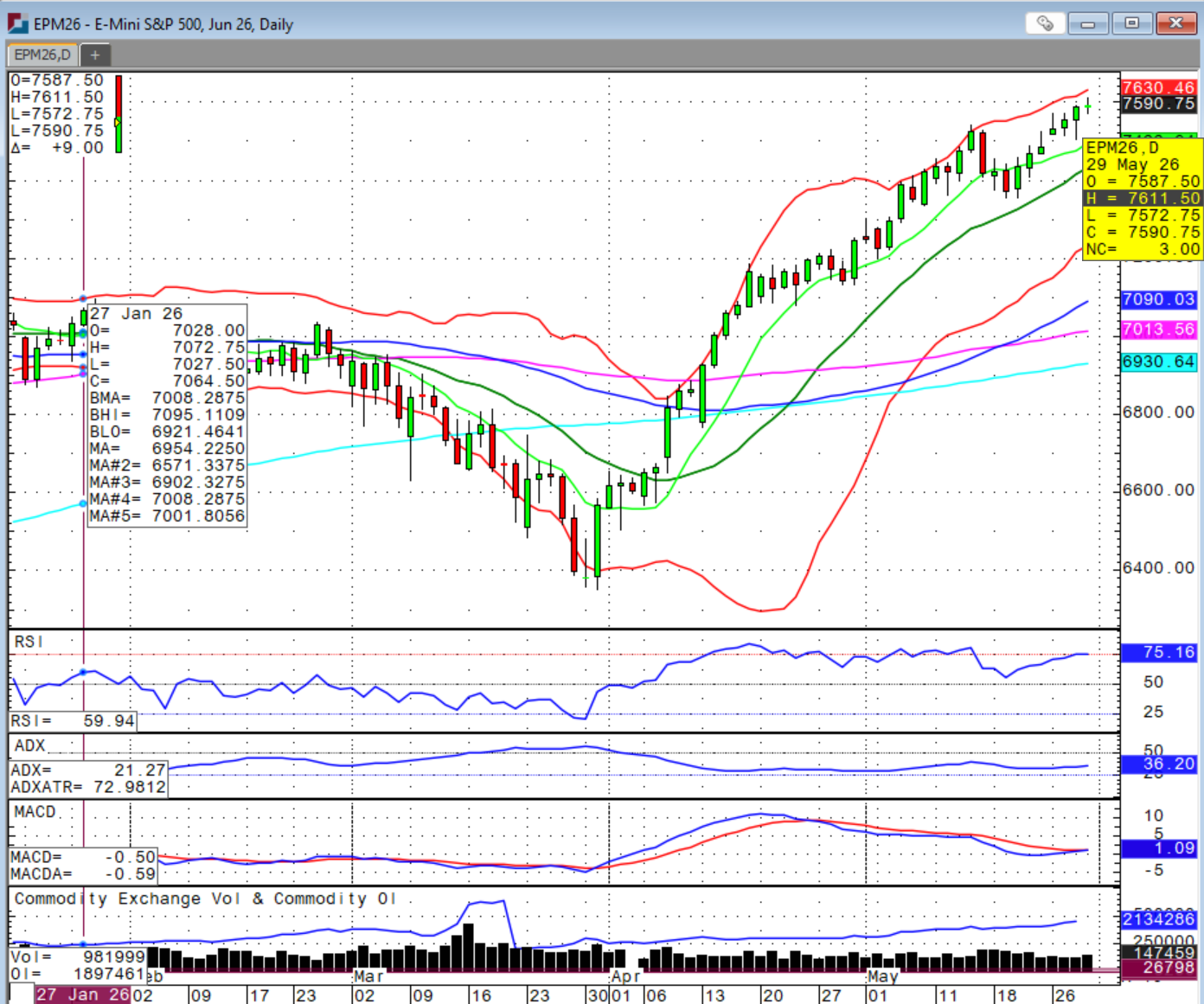

The equity markets were extra strong making and closing at new highs, which is unusual for the end of May, but was not enough to support the cattle futures complex. Just look at this chart of the recent upward momentum in the S&P 500!

Having said that, fed cattle cash trade did start developing late week and strengthened quickly on Friday to reach $257 in Texas, Kansas and Nebraska. This compares to the prior week’s high of $258 in Nebraska. There’s somewhat of a head-and-shoulders pattern in June live cattle and we would not want to see that 50-day moving average just above $247 violated. If fed cattle cash trade bottoms here and begins to climb higher, I think we could see the futures market strengthen especially with weaker corn prices and rainfall encouraging sale barn markets.

There will be several changes to the USDA’s Livestock Risk Protection beginning in the 2027 “crop year” that begins on July 1st. Categorically, the changes impact 52-week Cull Cow coverage, additional unborn feeder cattle options with higher weights up to 900 pounds that were previously capped at 599 pounds, expanded drought/forage disaster flexibility and higher Fed Cattle weight limits. The beginning farmer/rancher eligibility also expanded to 10 years. Please give me a call if you have any questions about how to best utilize LRP as well as futures and options to protect your price risk exposure in these volatile markets. Link to summary of changes: PM-26-024: Livestock Risk Protection, Livestock Gross Margin, and Dairy Revenue Protection - Modifications Effective for 2027 and Succeeding Crop Years | Risk Management Agency

There are so many outside factors influencing our agriculture markets that you must be prepared at a moment’s notice to act. When in doubt, protect your exposure to significant price swings. Note that feeder and live cattle limits expand starting Monday, June 1st as I previously outlined. Feeder cattle regular daily limits are now $10.75 per cwt with expanded limits to $16.00 per cwt. Live cattle regular daily limits are now $8.50 per cwt while the expanded limits go to $12.75 per cwt.

If consumer spending can maintain strength through these higher energy prices and the economy remains on stable footing, I think the cattle markets can find stability. However, I am getting more concerned that the situation is getting tighter and tighter for consumers with future sentiments coming under pressure that can change near-term spending behavior.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/International%20Business%20Machines%20Corp_%20logo%20on%20phone-by%20rafapress%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)