/Lam%20Research%20Corp_%20HQ%20sign-by%20Michael%20Vi%20via%20Shutterstock.jpg)

Investors have pushed Lam Research Corp (LRCX) stock sky-high as its free cash flow and semiconductor equipment revenue surge. A Barchart report shows investors piling into out-of-the-money LRCX put options.

LRCX is down today at $316.41, off 2.0% today, but it's still up 60% since the end of March (i.e., $199.93 on March 30).

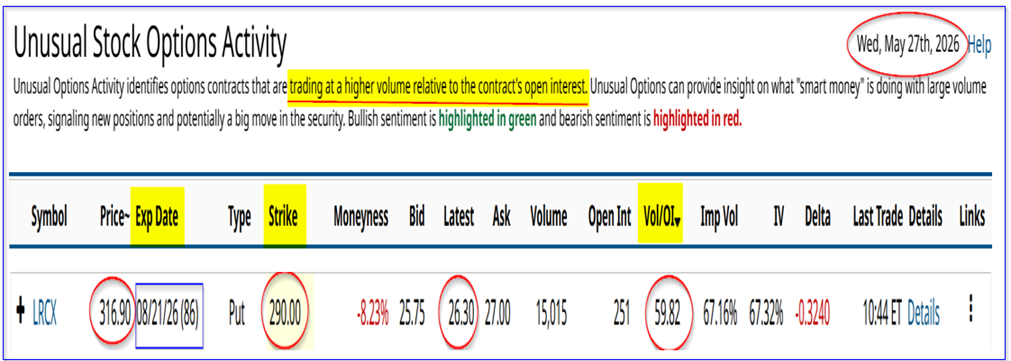

Investors are shorting out-of-the-money (OTM) Lam Research Corp (LRCX) put options to set a lower buy-in point and earn a 9% 3-month yield. This can be seen in a Barchart report that shows a 60x normal volume for an out-of-the-money LRCX put option.

The $290 LRCX put option expiring on Aug. 21, i.e., 8.34% below today's price (i.e., “out-of-the-money”), has a midpoint premium of $26.30. This put strike price has traded over 15,000 contracts traded today. That is 60 times the prior number of puts outstanding, a massive, unusual trading volume.

The Barchart Unusual Stock Options Activity Report today shows this massive trading volume in one put option contract. It seems to imply that some institutional investors are willing to buy LRCX at $290.00 and receive a huge income yield in return.

For example, one put contract shorted at $290.00 (i.e., an order to "Sell to Open) requires the investors to post collateral of $29,000. But, in return, the investor's account immediately receives $2,630. So, the short-put yield is:

$2,630 / $29,000 = 0.090689 = 9.0689% for the next 86 days (almost 3 months)

Moreover, the investor has a low breakeven point, even if LRCX falls 8.34% to $290.00:

$290.00 - $26.30 = $263.70

That is over 16.6% below today's LRCX stock price. In other words, the investor has a much lower potential buy-in. Meanwhile, their expected return is over 9% if LRCX stays over $290.00 for the next 86 days.

That is the same as buying LRCX and seeing the stock rise to $345 per share (i.e., +9%). In other words, these short-put investors are very bullish on LRCX.

Buyers of these puts must believe that LRCX will fall by over 16.6% for these puts to have any intrinsic value. That is a huge premium to pay to see a stock fall so much. This makes it more likely that the initiators of these put contracts were short-sellers bullish on LRCX stock. Let's look at why.

Strong Free Cash Flow Projections

Lam Research Corp., which makes semiconductor processing equipment and is benefiting from huge AI-related capex and investments by hyperscalers, reported that fiscal Q3 revenue rose 9.29% on a Q/Q basis (they don't even bother reporting the Y/Y numbers).

As a result, its revenue growth run rate could be over 36.1% (before compounding) over the next year. However, analysts are projecting a 32% FY revenue gain for the year ending June 30, 2027 (see below).

Moreover, diluted EPS was up 15.74% Q/Q, implying an annual run rate of 63% before compounding.

However, its free cash flow (FCF) fell 33.6% Q/Q to $809.82 million and -20.7% Y/Y. This was due to lower operating cash flow and higher capex. Nevertheless, its trailing 12-month (TTM) FCF was up 38% Y/Y to $6 billion (according to Stock Analysis). Moreover, its TTM FCF margin rose to 38.13% from 34.89% last quarter.

Based on analysts' revenue projections, FCF could surge next year. For example, analysts now forecast a 31.6% increase in FY 2027 revenue to $30.51 billion, up from $23.18 billion expected this fiscal year ending June 30, 2026.

So, if Lam Research can keep its TTM 38% FCF margin next year, FCF should rise to $11.6 billion (i.e., $30.51b x 0.381). That is 93% higher than the $6 billion over its most recent TTM period.

As a result, LRCX could be worth significantly more.

What LRCX Could Be Worth

Right now, Yahoo! Finance says Lam Research has a market capitalization of $398.5 billion. That implies that its TTM FCF of $6 billion represents a FCF yield of 1.50%:

$6b / $398.5 = 0.015 = 1.50% FCF yield

As a result, if we assume that the market values its expected FCF of $11.6 billion with the same yield, its market value could surge to $773 billion:

$11.6b / 0.015 = $773.33 billion

In other words, LRCX could see a huge 94% increase in the stock price:

$316.41 x 1.94 = $613.84 price target

That could be why investors have been pushing LRCX so high. And it also explains why investors are shorting out-of-the-money puts.

After all, if the short-sellers could repeat this 9.06% yield every 3 months for a year, they stand to make over 36.2%. That would be the equivalent of a price target of $431 per share.

That is lower than the $614 price target above, but shows why investors are bullish on LRCX stock.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/Sign%20of%20Intel%20at%20entrance%20%20by%20michaelmond.jpeg)