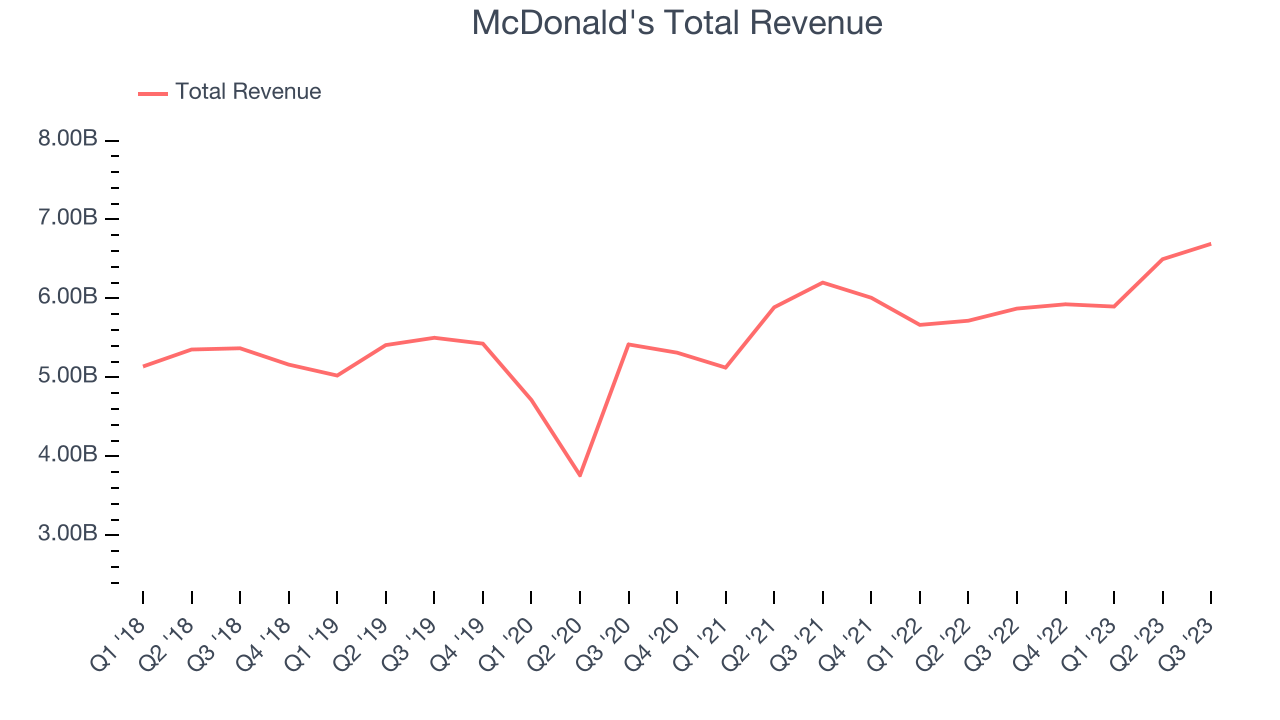

Fast-food chain McDonald’s (NYSE:MCD) reported Q3 FY2023 results exceeding Wall Street analysts' expectations, with revenue up 14% year on year to $6.69 billion. Turning to EPS, McDonald's made a non-GAAP profit of $3.19 per share, improving from its profit of $2.68 per share in the same quarter last year.

Is now the time to buy McDonald's? Find out by accessing our full research report, it's free.

McDonald's (MCD) Q3 FY2023 Highlights:

- Revenue: $6.69 billion vs analyst estimates of $6.55 billion (2.16% beat)

- EPS (non-GAAP): $3.19 vs analyst estimates of $2.99 (6.52% beat)

- Gross Margin (GAAP): 57.7%, down from 58.7% in the same quarter last year

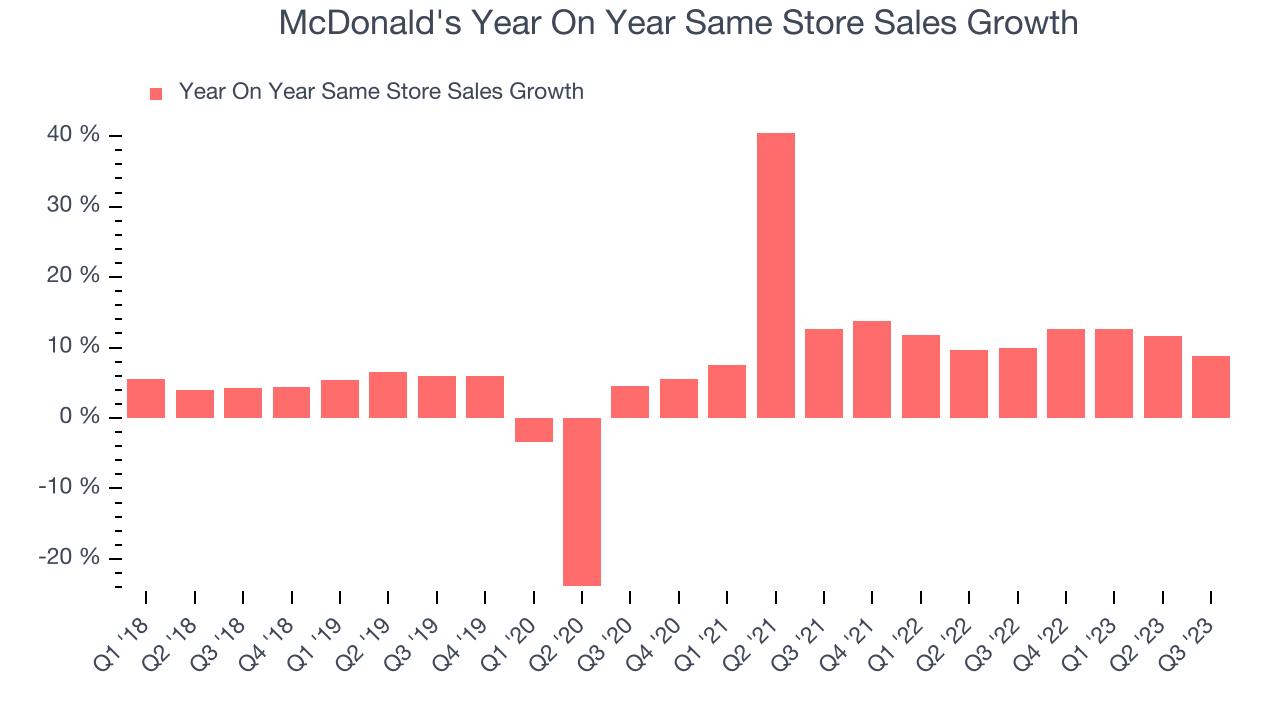

- Same-Store Sales were up 8.8% year on year (better than expectations of up 7.8% year on year)

"With global Systemwide sales growth of 11%, our third quarter results reflect our position of strength as the industry leader," said McDonald's President and Chief Executive Officer, Chris Kempczinski.

Arguably one of the most iconic brands in the world, McDonald’s (NYSE:MCD) is a fast-food behemoth known for its convenience, value, and wide assortment of menu items.

Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Sales Growth

McDonald's is one of the most widely recognized restaurant chains in the world and benefits from brand equity, giving it customer loyalty and more influence over purchasing decisions.

As you can see below, the company's annualized revenue growth rate of 4.35% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was mediocre as its restaurant footprint remained unchanged, implying that growth was driven by more sales at existing, established dining locations.

This quarter, McDonald's reported robust year-on-year revenue growth of 14% and its $6.69 billion of revenue exceeded analysts' estimates by 2.16%. Looking ahead, the analysts covering the company expect sales to grow 5.87% over the next 12 months.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

The number of dining locations a restaurant chain operates is a major determinant of how much it can sell and how quickly company-level sales can grow.

When a chain like McDonald's doesn't open many new restaurants, it usually means there's stable demand for its meals and it's focused on improving operational efficiency to increase profitability. As of the most recently reported quarter, McDonald's operated 40,000 total locations, in line with its restaurant count a year ago, although the company doesn't give an exact number of locations, only a rough one.

Taking a step back, McDonald's has kept its locations more or less flat over the last two years compared to other restaurant businesses. A flat restaurant base means McDonald's needs to boost foot traffic and turn tables faster at existing restaurants or raise prices to generate revenue growth.

Same-Store Sales

A company's same-store sales growth shows the year-on-year change in sales for its restaurants that have been open for at least a year, give or take. This is a key performance indicator because it measures organic growth and demand.

McDonald's demand has outpaced the broader restaurant sector over the last eight quarters. On average, the company has grown its same-store sales by a robust 11.4% year on year. Given its flat restaurant base over the same period, this performance stems from increased foot traffic or larger order sizes per customer at existing locations.

In the latest quarter, McDonald's same-store sales rose 8.8% year on year. This growth was a deceleration from the 10% year-on-year increase it posted 12 months ago, showing the business is still performing well but lost a bit of steam.

Key Takeaways from McDonald's Q3 Results

With a market capitalization of $184 billion, a $1.63 billion cash balance, and positive free cash flow over the last 12 months, we're confident that McDonald's has the resources needed to pursue a high-growth business strategy.

We were impressed by how significantly McDonald's exceeded analysts' revenue and EPS expectations this quarter. The company said that the macro is unfolding in line with its internal expectations, which is comforting. On the other hand, its gross margin missed analysts' expectations. McDonald's did not give guidance in the earnings release. Zooming out, we think this was a decent, albeit mixed, quarter, showing that the company is staying on track. The stock is up 2.67% after reporting and currently trades at $262.65 per share.

So should you invest in McDonald's right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)