Happy Memorial Day weekend market watchers!

While this weekend marks the official unofficial start to summer, it is the time we remember, honor and thank our fellow countrymen and women who serve in the line of duty to keep our country free and allow us all to pursue our ambitions. At a time when chaos seems to be returning to the world, we pray for those who sacrifice their time and lives to keep our families and freedoms protected.

Pay attention to all the American flags that are an unwavering reminder of their commitment and to all of those who have come and gone before. It will also be a weekend of additional rainfall chances across the Plains that have been devoid of spring precipitation and caused severe drought from Texas all the way to Nebraska and west. What an unusual weather year it has already been.

Here we are at Memorial Day thinking that the wheat harvest would be well underway with the earliest maturity in multiple decades from heat and drought and now we’re waiting for dryer weather. The irony is thick. In an ordinary year, the rain and cooler temps would be ideal for winter wheat to fill and yet it is ripe and ready to harvest and now raining. However, I think we have learned to never complain about rain and the grass pastures, corn and soybeans are sure welcoming the change.

Winter wheat conditions slipped again this week to just 27 percent Good-to-Excellent while expectations were 28 percent. The wheat market also cooled down after a lack of fresh bullish news and heavy selling pressure in the crude oil market weighed on grains this week.

The above chart gap filled on the US dollar index this week as inflationary concerns strengthened the currency and raised bond yields that put downward pressure on the stock market. The continued back and forth between President Trump and the idea of an imminent deal to “end” the war brought about significant volatility to the crude oil markets that brought down bond yields and rallied the stock market near record highs into the weekend even as there is still no deal with Tehran.

President Trump held a White House ceremony on Friday to swear in the new Federal Reserve Chairman, Kevin Warsh. The page has now turned and the market will be closely watching and trading the actions of new leadership for the Central Bank. While crude oil prices closed the week below $100 per barrel, the chart remains in a bullish channel. Even the slightest change in rhetoric can spike the markets as reserves around the world are said to be quickly depleting, making quick price shocks more likely.

As summer travel plans begin, we will all be more mindful of fuel prices as we hit the road and as harvest and then field work gets underway. Without a near term resolution to the Middle East conflict and reopening of the Strait of Hormuz, inflationary pressures driven by fuel and fertilizer will put upward pressure throughout the supply chain all the way to consumers.

President Trump’s recent trip to China was, in part, intended to garner support from Beijing to apply pressure on Iran to reopen the Strait without toll charges and other conditions. China is heavily dependent on oil and other supplies from that region and paying the price of restricted supply and elevated costs. Without any specific announcements on purchase commitments upon Trump’s departure from Beijing, the ag markets were disappointed in the absence of such as seen here in the corn chart.

However, on Sunday evening, the White House released news of broad commitments and agreements that were finalized at the end of the trip. Agriculture was, in fact, a central part of the agreements. Firstly, China agreed to purchase at least $17 billion per year for 2027 and 2028 and prorated for the remainder of 2026, that is in addition to the annual soybean commitments agreed to in October 2025. Secondly, China has restored US beef market access by renewing expired licenses for more than 400 US beef facilities and permitted new listings. This was a point of confusion during the trip with the news followed by plants being delisted after being relisted. The lifting of facility suspensions will take time to unravel between US and Chinese regulators. Thirdly, China will resume imports of US poultry from states that the USDA determines are free of highly pathogenic avian influenza. These are all important steps for US agriculture and meaningful progress. Link to full White House release here: Fact Sheet: President Donald J. Trump Secures Historic Deals with China, Delivering for American Workers, Farmers, and Industry – The White House

We may also soon hear that China will lower import tariffs on other ag products and begin announcing a variety of purchases. Here’s where it gets interesting. One of President Trump’s asks to President Xi was to not send military equipment to Iran. Well, this is at a time when the US is in the process of sending military equipment to Taiwan, which is a frequent customer. US support of Taiwan is now somewhat of a bargaining chip for China with President Trump needing China’s cooperation regarding Iran.

In a political staging move, President Xi welcomed Russian President Putin to Beijing immediately after Trump giving him the very same warm invitation that profiled China as a global mediator on the world stage. China and Russia also signed numerous trade deals to represent cooperation. President Trump may very well lean on China to help resolve the Russia aggression in the Ukraine and to find some stability of the Iranian situation. The more I see the Administration touting that a deal is near and then the Iranians making an extravagant threat, the more concerned I get that there is no good deal for the US to make in this situation. However, the polarization of the upcoming US election is such that some type of resolution is needed in a timely fashion and without further military action. Better leverage is needed to force a desirable conclusion.

The more prolonged this conflict, the more inflation and tighter monetary policy will be needed. There is increasing discussion that higher fertilizer prices could restrict production in Brazil and other economies that could in turn push prices higher. As we know, commodities are also considered a hedge against inflation as they rise with inflation. All these factors may indeed lead to a coming bullish cycle in agriculture, energy and precious metal commodities that have already made a meaningful move.

Source: DTN

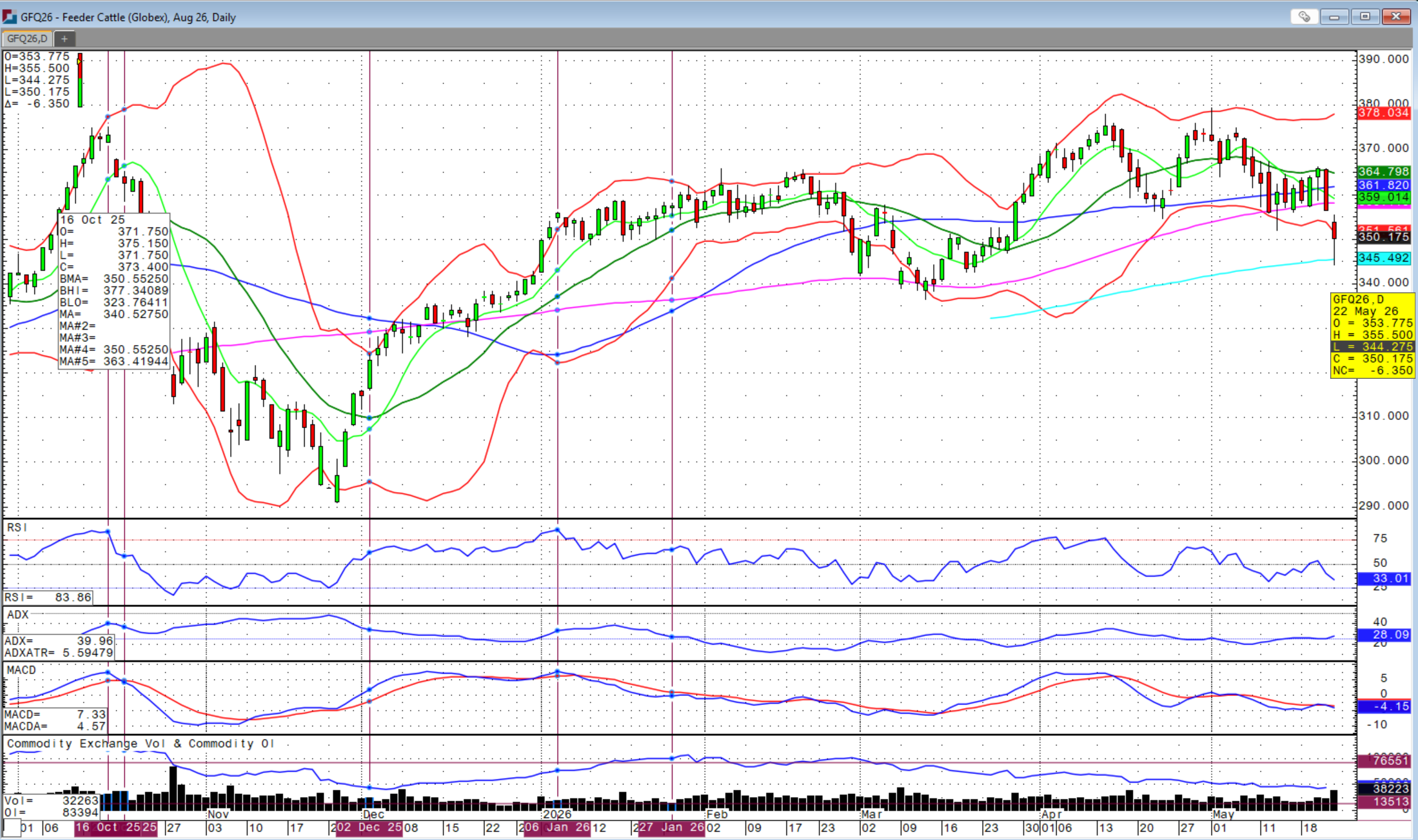

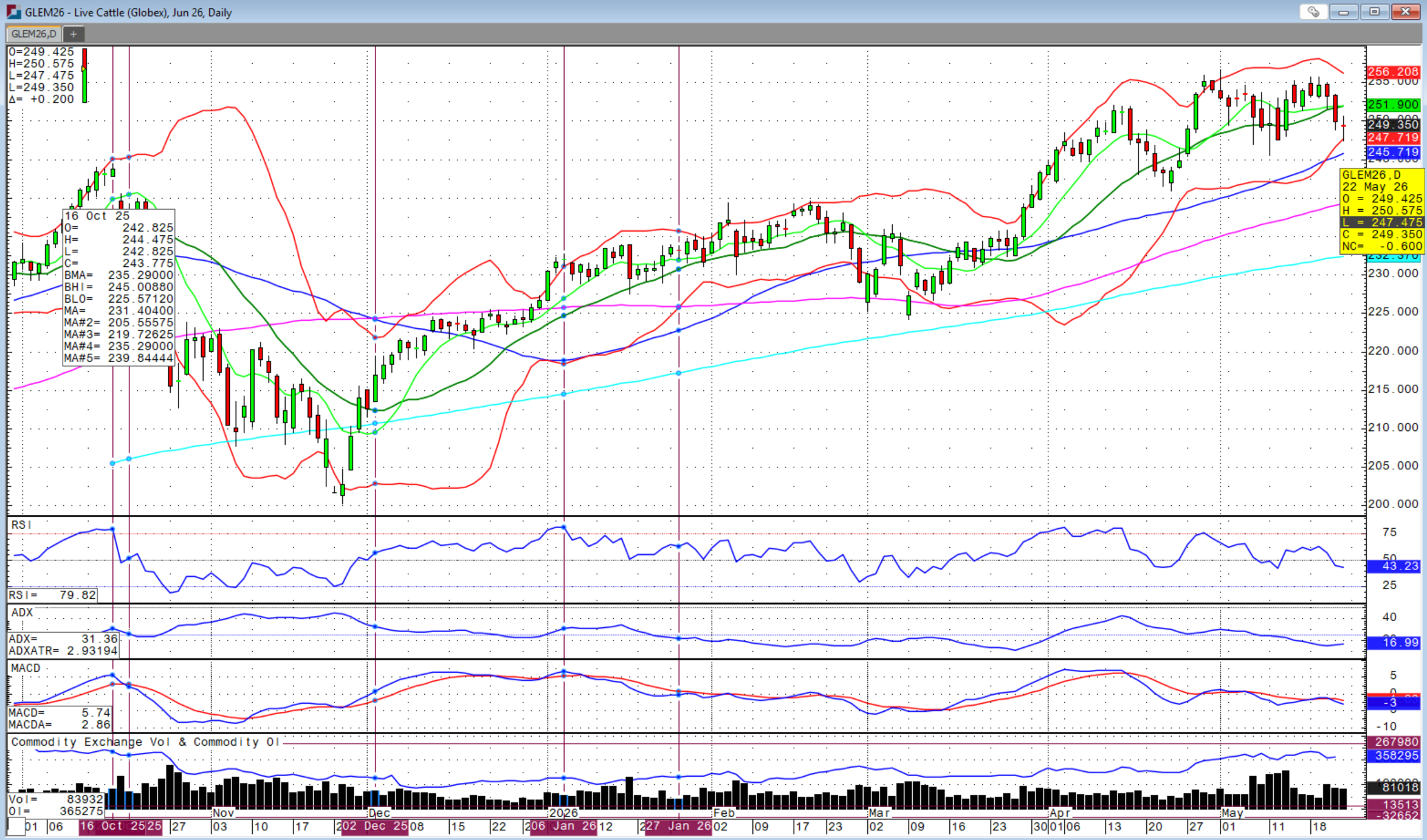

The cattle market began to suggest more topping action this week after its recent super cycle. Most of the market action this week was a choppy, but sideways affair with selloffs responded to with rallies. Tuesday’s action on feeder cattle was that of an outside reversal higher day on the charts suggesting further upside in the following session. Wednesday’s session started weaker and then much weaker only to recover strongly making a high above the prior day’s high and closing just above the 20-day moving average. All signs of a bullish reversal.

And then there was Thursday with August and later contracts finishing limit down at $9.25 per cwt! The result was no LRP except the 52-week option.

Then, Friday was the USDA’s Cattle-on-Feed report, a day which there is also no LRP offered. With expanded limits of $13.75 on feeders and $10.75 on fats, the market opened weaker on Friday and then continued to press for new lows, gapping lower from Thursday and selling all the way down to and briefly below the 200-day moving average at $345.492 on August feeders. The session lows were $344.275, but managed to recover well off the lows by the close, trading back above $350 to close the week at $350.175. Wow! That’ll get your attention!

Cargill’s Fort Morgan beef processing facility has been handling low to no cattle for awhile, but was officially closed and locked down this week that sparked fund liquidation. There were already expectations for a bearish on-feed report with anticipation of the first year-on-year increase in 18 months. I believe there is also expectations that President Trump is going to resume rhetoric on tamping high beef prices and investigating beef packers. While this Executive Order on beef imports was delayed prior to the China trip, it could return to the headlines at any time as affordability will definitely be a central issue of this campaign season.

The monthly USDA cattle-on-feed report was released at 2 PM on Friday, after the market close at 1:05 PM. As expected, the report had a bearish bias and was slightly more than expected. May 1st cattle-on-feed came in slightly higher than expected at 101.8 percent of last year versus 101.6 percent expected. April placements were also higher than expected at 105.5 percent versus 103.4 percent. Marketings for April were lower than expected at 90.0 versus 90.7 percent. There was some fed cattle cash trade this week that topped out at $260 in Kansas and Texas with one $265 early in the week in Nebraska and $258 late on Friday.

We will have to see if all of this bearishness was in fact priced in on the Thursday and Friday market move. We do have a chart gap above from Thursday’s low to Friday’s high. All ag markets will be closed Monday in observation of Memorial Day. Grains will open on Monday evening at 7 PM CDT. There will be some energy and equity futures trading on Monday, but with early closes.

LRP will resume on Tuesday assuming no futures trading limits are triggered. There have been updates made to LRP that will come into effect on July 1st and we will be outlining these changes in next week's article. Stay tuned!

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)