Shares of Arm Holdings (ARM) have more than doubled over the past three months. The rally reflects surging enthusiasm around artificial intelligence (AI) infrastructure, particularly the company’s newly launched AGI CPU platform designed specifically for agentic AI workloads.

Thanks to the rally, ARM stock has recently climbed to an all-time high of $315. While the rapid rise has raised concerns about valuation, the company’s latest quarterly results and solid long-term projections suggest the AI opportunity is significant and could support its share price rally.

Arm’s Strong Financials

Arm recently announced a solid fourth-quarter fiscal 2026 performance. Revenue for the quarter climbed 20% year-over-year (YOY) to $1.49 billion. Furthermore, fiscal 2026 revenue reached $4.92 billion, up 23% YOY.

Fourth-quarter license and other revenue increased 29% to $819 million, driven by rising demand for next-generation chip architectures and deeper strategic partnerships with major customers. Annualized contract value (ACV), a key indicator of future revenue visibility, also rose 22% YOY.

Another catalyst is the increasing adoption of Arm-based processors in cloud data centers.

Major hyperscalers continue expanding deployments of Arm-powered server chips, while networking infrastructure products such as DPUs and SmartNICs are also gaining traction. The impact is already visible in the company’s royalty revenue. Royalty revenue for Q4 rose 11% YOY to $671 million. Management noted that data-center royalty revenue continues to more than double annually, with no indication of slowing momentum.

Cloud AI workloads were the largest contributor to this growth, indicating that AI infrastructure spending remains exceptionally strong despite broader macroeconomic uncertainties.

Beyond cloud AI, Arm is seeing growth across multiple end markets. Smartphone royalty revenue continued to expand despite weaker overall handset demand, largely due to higher royalty rates tied to the growing adoption of Armv9 architecture in premium devices. The company is also benefiting from the rise of physical AI, including advanced driver-assistance systems (ADAS) and autonomous technologies built on Arm-based platforms.

The Rise of Agentic AI Is Creating a Massive CPU Opportunity

Arm’s momentum is driven by the emergence of agentic AI. As these systems scale across industries, the computational demands placed on data centers are expected to increase dramatically. To address this shift, Arm introduced its AGI CPU at the company’s “Arm Everywhere” event earlier this year. The processor was purpose-built for agentic AI environments.

Management indicated that customer demand for the new platform has already exceeded expectations. The company now has visibility into more than $2 billion in customer demand spanning fiscal 2027 and fiscal 2028. Despite this strong pipeline, Arm is maintaining its current $1 billion near-term outlook as it works through supply-chain capacity constraints.

The company believes this business could eventually become huge. By fiscal 2031, management projects the AGI CPU segment could generate approximately $15 billion in annual revenue, alongside another $10 billion from intellectual property (IP) licensing. Combined, that would represent a potential $25 billion revenue opportunity and could translate into EPS exceeding $9 annually.

Arm’s Outlook Suggests Momentum Remains Intact

Arm expects Q1 fiscal 2027 revenue of approximately $1.26 billion, representing 20% YOY growth. Management also forecasts both royalty revenue and licensing revenue to grow around 20%, signaling that demand remains broad-based across its business segments.

Adjusted EPS is expected to reach approximately $0.40, significantly higher than analysts’ forecast of $0.18.

Overall, Arm's outlook reflects strong customer demand, an expanding product portfolio, and deeper enterprise engagements. These factors will continue to support its financials and share price.

Can Arm's Rally Sustain?

Arm provides foundational architecture that powers a wide range of AI infrastructure, from cloud servers to networking systems and edge devices. As agentic AI adoption accelerates, the need for energy-efficient, scalable CPUs will jump significantly, supporting Arm’s growth.

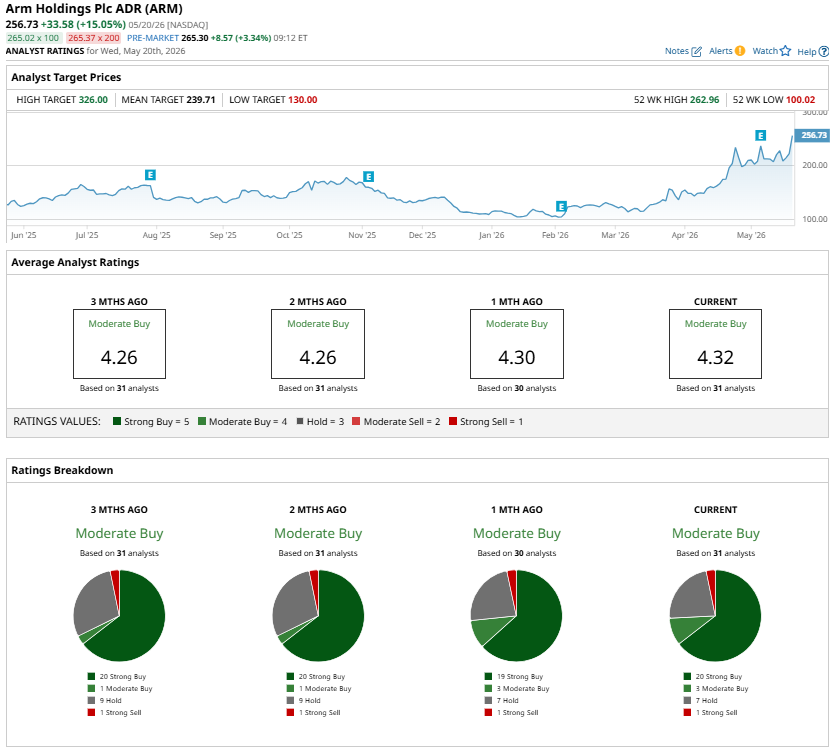

However, valuation remains a concern. ARM stock’s forward price-to-earnings (P/E) multiple of 228.7 times is expensive. Accordingly, Wall Street analysts remain cautiously optimistic with a “Moderate Buy” consensus rating.

All told, Arm’s long-term growth prospects remain strong, and ARM stock has the potential to move higher. Still, investors may find a pullback to be a more attractive entry opportunity.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)