BP plc BP and Enterprise Products Partners LP EPD are two major players in the energy industry with contrasting business operations. BP is an integrated energy company with operations spanning production, refining and commodity trading. The company delivered a quarterly earnings beat, supported by standout downstream and oil trading contributions. It is currently focused on expanding its upstream production through the start-up of key projects and prioritizing cost efficiencies and operational improvements to lower its structural cost base, enhancing its resilience.

Enterprise Products operates an integrated, midstream asset network for the transportation and storage of crude oil, natural gas, natural gas liquids (NGLs), petrochemicals and refined products. The partnership’s midstream assets connect suppliers from some of the largest basins in the United States, Canada and the Gulf of America to various domestic and international markets.

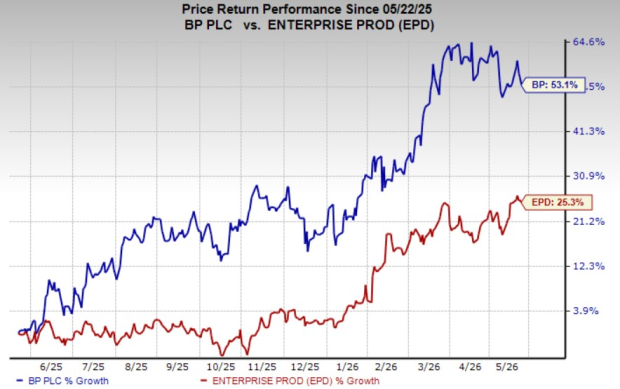

Over the past year, BP shares have rallied 53.1%, outperforming Enterprise Products’ 25.3% gain. Price performance alone does not fully capture a stock’s attractiveness, as it merely reflects investor sentiment across business cycles. Hence, it is essential to assess the fundamentals and broader operating environment of both stocks before arriving at an investment decision.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Diversified Asset Base and High Oil Prices Support BP’s Profitability

BP noted that a key factor determining the strength of its business is the depth of its upstream portfolio. It benefits from a strong and diversified global asset portfolio. The company has a major presence in the United States that contributes to production, and its future growth in the United States is expected to come from the Paleogene development and BPX operations. It also pointed to major discoveries, such as Bumerangue in Brazil, which may emerge as a significant long-term growth driver.

Additionally, BP’s exploration successes bring more growth opportunities for the business. Since the start of 2025, the company has announced 14 discoveries, including two in Egypt and Angola in 2026. The company is focused on adding new upstream opportunities to its portfolio, which is expected to help counter natural production declines and support its target of achieving a 100% reserve replacement by 2027.

BP’s upstream activities have substantial exposure to rising oil prices, driven by the conflict in the Middle East and disruptions to energy flows through the Strait of Hormuz. Higher oil prices are expected to boost BP’s upstream earnings and cash flows. As a result, its overall upstream business outlook appears extremely favorable in the near term.

EPD’s Contract-Backed Business Model Ensures Stable Cash Flows

Enterprise Products owns and operates a pipeline network spanning 50,000 miles that transports crude oil, natural gas, natural gas liquids and refined products across North America. The partnership generates stable fee-based revenues, implying that its earnings are less vulnerable to commodity price swings. This allows EPD to generate predictable cash flows across business cycles. Notably, the partnership has highlighted that almost 90% of its long-term contracts include an escalation provision that protects its cash flows and distributions in inflationary business environments.

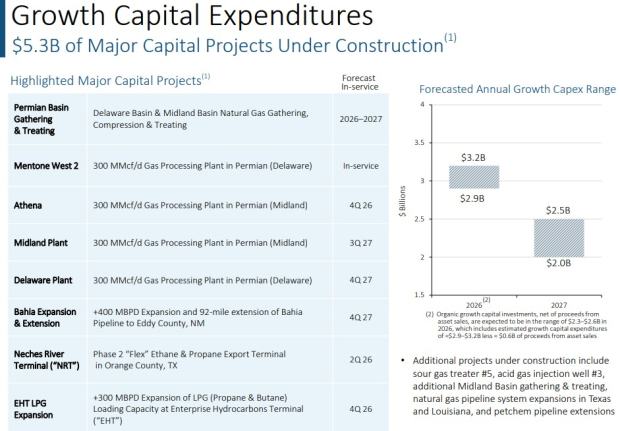

The partnership has major capital projects worth $5.3 billion under construction, which are expected to begin operations through 2026 and 2027. These growth projects are supported by favorable energy market fundamentals. These include rising global demand for hydrocarbon liquids, driven by higher petrochemical and LPG demand, along with the rising production of oil and natural gas in the Permian Basin through the end of this decade. These developments are expected to create sustained demand for EPD’s midstream services, thereby aiding its earnings and cash flows.

Image Source: Enterprise Products Partners L.P.

Image Source: Enterprise Products Partners L.P.

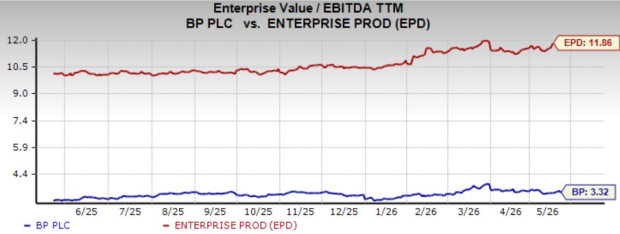

Valuation Snapshot

Considering the valuation snapshot, it has become evident that BP is currently trading at a discount compared with Enterprise Products. This is reflected in the fact that BP trades at a trailing 12-month enterprise value to EBITDA (EV/EBITDA) of 3.32X, below EPD’s 11.86X.

Image Source: Zacks Investment Research

BP vs EPD: Should You Buy or Wait?

BP and EPD have extremely different business models and strengths. BP offers stronger upside potential in the current environment due to its diversified upstream asset base and exposure to elevated oil prices. Meanwhile, Enterprise Products Partners provides greater business stability through its fee-based midstream model, long-term contracts and predictable cash flow profile.

As such, investors who want exposure to the oil price volatility and seek to gain from the higher upside from stronger oil prices may consider buying the BP stock, which sports a Zacks Rank #1 (Strong Buy) at present. At the same time, those who prefer stability and predictable cash flows should consider owning the EPD stock, currently carrying a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>This article originally published on Zacks Investment Research (zacks.com).

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Abbott%20Laboratories%20vials%20and%20Logo-by%20Melniov%20Dmitriy%20via%20Shutterstock.jpg)

/Intuit%20Inc%20logo-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)