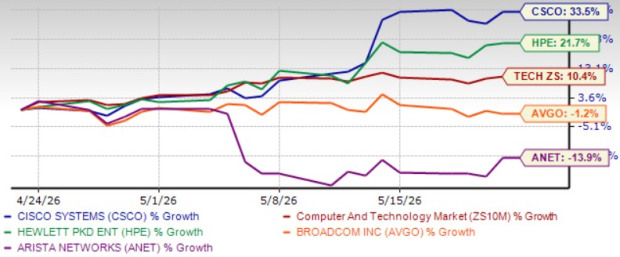

Cisco Systems CSCO shares have risen 33.4% in a month, outperforming the broader Zacks Computer & Technology sector’s return of 10.4%. The company has been benefiting from a strong AI push despite stiff competition from the likes of Hewlett Packard Enterprise HPE, Broadcom AVGO and Arista Networks ANET. While shares of Hewlett Packard Enterprise have returned 21.7%, Broadcom and Arista Networks have dropped 1.2% and 13.9%, respectively. All three stocks have lagged CSCO over the same timeframe. So, should investors buy CSCO stock now? Let’s find out.

CSCO Stock’s Price Performance

Image Source: Zacks Investment Research

CSCO’s Prospects Ride on Strong AI Networking Demand

Cisco is benefiting from strong demand for AI infrastructure and campus networking solutions. Networking product orders continued to accelerate, growing more than 50% in the third quarter of fiscal 2026, driven by triple-digit growth in service provider routing and compute and double-digit growth in data center switching, campus switching, wireless, enterprise routing and industrial IoT products. AI infrastructure orders taken from hyperscalers totaled $1.9 billion in the reported quarter compared to $600 million in the year-ago quarter, with strong growth across Silicon One systems and market-leading Acacia Optics.

Total product orders increased 35% year over year overall and 19% excluding hyperscalers, indicating broad-based demand strength in the third quarter of fiscal 2026. Order from hyperscalers jumped triple digits, with product orders from enterprise, public sector, as well as service provider and cloud customers rising 18%, 27%, and 105% year over year, respectively. Year to date, hyperscaler AI orders have already reached $5.3 billion. Telco orders grew 9% as customers prepare their networks to handle the scale, speed and complexity of AI. Cisco emphasized that customers are upgrading networks to support inferencing, agentic AI workloads, and higher traffic volumes. Wi-Fi 7 adoption is accelerating quickly, representing half of the wireless mix in the third quarter of fiscal 2026.

Cisco raised its fiscal 2026 hyperscaler AI infrastructure order outlook from $5 billion to $9 billion and increased expected AI infrastructure revenues from $3 billion to $4 billion. Management highlighted strong momentum in Silicon One systems and Acacia optics, along with five new hyperscaler design wins during the quarter. Cisco repeatedly emphasized Silicon One as a major competitive advantage with hyperscalers because it improves supply chain control and performance differentiation. Acacia optics surpassed $1 billion in quarterly orders, and Cisco has already shipped more than 750,000 400G and 40,000 800G coherent pluggable optics. The company is increasingly positioned as a strategic AI networking supplier rather than a traditional enterprise networking vendor.

CSCO Offers Positive FY26 Guidance

For fiscal 2026, CSCO expects revenues to be in the $62.8-$63 billion range compared with $56.7 billion reported in fiscal 2025. Non-GAAP earnings are expected between $4.27 per share and $4.29 per share compared with $3.81 per share reported in fiscal 2025.

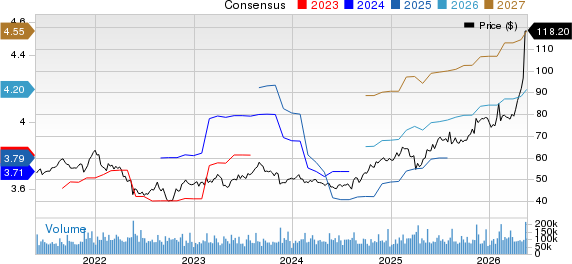

The Zacks Consensus Estimate for CSCO’s fiscal 2026 revenues is pegged at $62.77 billion, indicating growth of 10.8% from fiscal 2025. The consensus mark for CSCO’s fiscal 2026 earnings is currently pegged at $4.20 per share, up by a couple of cents over the past 30 days, indicating year-over-year growth of 10.2%.

Cisco Systems, Inc. Price and Consensus

Cisco Systems, Inc. price-consensus-chart | Cisco Systems, Inc. Quote

Cisco Suffers From Stiff Competition, Lower Gross Margin

Cisco is suffering from stiff competition from Hewlett Packard Enterprise, Broadcom and Arista Networks. Hewlett Packard Enterprise benefits from the Juniper Networks acquisition, elevating HPE’s competitive stance by expanding its networking domain in AI, cloud and hybrid solutions. Broadcom is experiencing strong momentum fueled by growth in AI semiconductors and continued success with its VMware integration. The versatility of Arista Networks’ unified software stack across various use cases, including WAN routing, campus and data center infrastructure, sets it apart from its competitors.

Non-GAAP gross margin declined 260 basis points (bps) year over year to 66%, while product gross margin fell 330 bps due to AI hardware mix and elevated memory costs. Management acknowledged that the mix shift toward lower-margin AI infrastructure is the biggest pressure point, and future AI scaling could continue weighing on profitability.

Moreover, Security is suffering from Splunk’s transition from on-premise licenses to cloud subscriptions. These continue to create a near-term revenue drag. While management expects improvement, software growth currently trails hardware growth materially.

Cisco Shares Are Trading at a Premium

Cisco shares are trading at a premium, as suggested by the Value Score of F. In terms of the forward 12-month price/sales, CSCO is trading at a premium of 7.18X, higher than the Zacks Computer & Technology sector’s 6.81X and Hewlett Packard Enterprise’s 1.08X.

However, Cisco shares are trading at a discount compared with Arista Networks and Broadcom. In terms of the forward 12-month P/S, Arista Networks and Broadcom shares are trading at 14.97X and 15.05X, respectively.

CSCO Stock’s Valuation

Image Source: Zacks Investment Research

Conclusion

An expanding portfolio makes Cisco well-positioned for sustained growth in an evolving tech landscape. AI push is noteworthy, along with an expanding networking portfolio. These trends are expected to help the stock rally and bode well for CSCO’s long-term prospects.

CSCO currently carries a Zacks Rank #2 (Buy), suggesting that it is the right time to start accumulating the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>This article originally published on Zacks Investment Research (zacks.com).

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Abbott%20Laboratories%20vials%20and%20Logo-by%20Melniov%20Dmitriy%20via%20Shutterstock.jpg)

/Intuit%20Inc%20logo-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)