After dropping in the first two days of trading this week, the S&P 500 has battled back, gaining 0.2% on Thursday. The index is now up 0.5% through the first four days, with the futures pointing higher as I write this pre-market.

The index’s high for the day of 7,465.96 was 51.16 points shy of the all-time high of 7,517.12 set last week. Could it set another record today?

The big number out today is the University of Michigan Consumer Sentiment Index’s reading for May. Economists expect it to remain unrevised at 48.2, down slightly from 49.8 in April, and 7.7% from May 2025.

Despite consumer sentiment that’s lower than it’s been in the past decade, the markets keep moving higher. The market melt-up over the past two months hit a speed bump earlier this week, but now appears to be back on track.

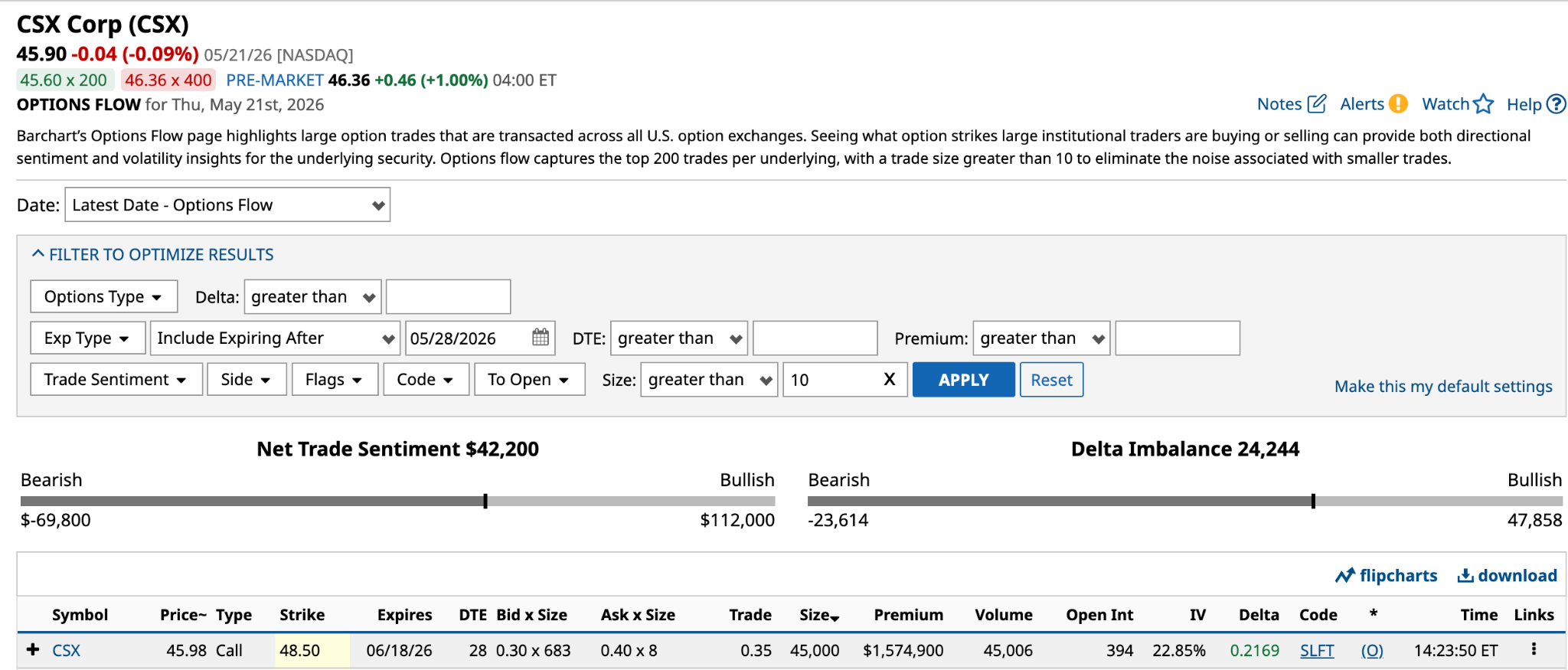

In yesterday’s options market, volume was 59.66 million, about 2.0 million less than the 90-day average. Calls accounted for 62% of contracts traded, with 55% of those being single-leg trades.

One of the single-leg trades yesterday was for a stock that also happened to have the most unusually active option on the day with a Vol/OI (volume-to-open-interest) ratio of 118.49.

Read on as I consider why one institution was so hot to trot for railroad operator CSX (CSX).

Have an excellent weekend.

The CSX Option in Question

CSX’s volume yesterday was 51,820, 3.5 times higher than its 30-day average. The unusually active June 18 $48.50 call option, mentioned above, accounted for 90% of that volume. A single trade for 45,000 took place at 2:23 ET. It accounted for 96% of the volume for the June 18 $48.50 call.

The options flow shown above highlights several things. First, the single-leg trade is flagged as “To Open” rather than “Buy to Open” or “Sell to Open,” leaving it up to investors to determine the intent or strategy of both sides of the trade.

Let’s consider the possibilities.

CSX Buy to Open

On the buy side of the 45,000-contract trade, the most plausible explanation is that an institution has opened a new position to gain exposure to CSX over the next month without committing significant capital. In this trade, they acquired the right to buy 4.5 million shares for $1.58 million or 0.7% of the cost to buy them outright.

A second possibility is that the institution already owns the stock and is buying the 45,000 call contracts as an overlay to boost its returns on the stock over the next month. The overlay assumes the institution expects a significant jump over the next 28 days.

For example, the expected move through June 18 is 4.31%. Based on the $45.98 share price at the time of the call trade, that would put CSX’s share price at $47.96 at expiration. That’s below the $48.85 breakeven [$48.50 strike price + $0.35 trade price], so it probably is looking for something more here.

That said, it could double its money by selling the calls to close the position before June 18 if the share price rises to $47.59, which is within the expected move. That’s a 1,304% annuallized return.

Not too shabby.

CSX Sell to Open

Another possibility is that the institution already owns CSX stock and is looking to generate income over the next month by opening a Covered Call strategy. Based on the $0.35 trade price, the return would be 0.8% [$0.35 bid price / $45.98 share price - $0.35 bid price]. Annualized, that works out to 10.0%.

Now, for an institution to do this, only 6.8% OTM (out-of-the-money), it must have bought CSX stock well below its current share price, because if it’s ITM (in-the-money) in 28 days, the buyer of the calls could exercise their right to buy the shares at $48.50.

CSX stock is up over 50% in the past year, so this covered call strategy could be what’s going on here.

The Other Side of the Trade

Sometimes, when looking at an options trade, it’s easy to forget there are two sides to every trade. Instinctively, when you see a large trade like this one, you immediately think someone is very bullish about the stock--and you’d be right.

So, what’s on the other side of this particular trade?

One likely scenario is that the institution owns CSX stock and is buying to close its open covered call position, which it originally sold to open to generate income.

The second possibility is that the institution is using a delta-hedging strategy, which market makers use to reduce or eliminate the directional risk of their positions.

In the example of the 45,000 calls, it is selling them short to the call buyer. While it generates a premium of $1.58 million on the trade, it’s not in the business of making directional bets. Its role is to provide liquidity for stock and option investors.

It achieves delta neutrality on these 45,000 calls by purchasing enough shares to offset the upside risk. So, given the delta of 0.2169, it would buy 976,050 shares [45,000 contracts * 100 * 0.2169 delta] to bring the delta to 0.0.

Let’s assume CSX’s share price moves $10 between now and the June 18 expiration. The market maker would lose approximately $22.1 million on the trade.

1. The short calls are deep ITM, generating a $32.09 million loss [$55.98 share price - $48.50 strike price - $0.35 trade price * 45,000 * 100].

2. The 976,050 shares bought have gained $9.76 million [$55.98 current share price - $45.98 purchase price * 976,050].

3. A $225,000 profit on bid/ask spread [$0.35 trade price - $0.35 bid price * 45,000 * 100].

In a real-world situation, the market maker would buy more shares to minimize the losses from a sharp move higher. This strategy is called Dynamic Hedging. It’s a critical part of a market maker’s toolkit.

Why CSX?

Of the 24 analysts that cover CSX, 16 rate it a Buy (4.21 out of 5). However, its target price of $46.15 is barely higher than its share price.

Analysts expect it to earn $1.89 and $2.13 in 2026 and 2027, respectively. Its shares trade at 21.6 times the 2027 estimate. Historically, they’ve traded in the mid-to-high teens, so it’s a little pricey, but not outrageously so.

Further, it has outperformed both Norfolk Southern (NSC) and Canadian Pacific Kansas City (CP) over the past 12 months, suggesting investors believe it has a better business in this economic environment.

Clearly, the buyer of the 45,000 June 18 calls thought so. I guess we’ll find out.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)