Box (BOX) has pushed its way back into Wall Street conversations after CEO Aaron Levie turned up the heat around artificial intelligence (AI) agents and enterprise automation. The stock looked dead in the water for months, though recent gains finally gave investors a reason to dust off the bull case.

The company wants investors to see it as far more than a digital filing cabinet. Box is now aiming to position itself as an AI-driven workflow platform that helps businesses manage content, automate tasks, handle e-signatures, and organize metadata in one connected system.

At the center of that strategy is Box Automate, though Wall Street rarely hands out gold stars for promises alone. Customers need to adopt these products in meaningful numbers before sentiment turns into sustained confidence.

This puts serious pressure on Box’s Q1 FY2027 earnings report scheduled for Tuesday, May 26, after the opening bell. Investors would be scanning the results for signs of stronger adoption, better upselling, and growing demand for premium offerings like Box AI and Enterprise Advanced.

About Box Stock

Based in Redwood City, California, Box operates a cloud driven content management platform that allows businesses to securely store, share, organize, and collaborate on files across any device.

Carrying a market cap of $3.56 billion, its software powers workflows, e-signatures, and custom application development while helping businesses tighten operations and improve productivity across global teams.

Box’s shares have tumbled 19.4% over the past 52 weeks and remain down 14.98% so far this year, which hardly makes for easy reading no matter how compelling the future narrative sounds.

But the last three months told a different story, with the stock climbing 11.2%, signaling that investors have slowly started warming up again as AI chatter is pushing Box back onto Wall Street’s radar.

Valuation adds another interesting wrinkle. BOX stock is currently trading at 16.35 times forward adjusted earnings along with 2.80 times sales. Both figures sit below the industry average and below the company’s own five-year historical averages, which signals a discount to its usual price tag.

Box Surpasses Q1 Earnings

March 3 was a good day to own BOX stock. The company reported Q4 FY2026 results that surprised investor, with the stock jumping 1.44% on the day and then tacking on another 10.16% the very next session.

Revenue hit $305.9 million, growing 9.4% year-over-year (YOY) and beating analyst estimates of $304.3 million. Non-GAAP net income rose 12.8% YOY to $71.9 million, and adjusted EPS came in at $0.49, blowing past analyst forecasts of $0.34 by 16.7%.

Customers paying Box at least $100,000 annually grew 9% YOY. Enterprise Advanced, the company's highest-tier suite that launched just a year ago, already accounts for 10% of total revenue, which is a faster ramp than the timeline suggested it would be.

Box ended Q4 with remaining performance obligations (RPO) of $1.7 billion, up 17% YOY. Short-term RPO grew 12% YOY, driven by longer contract durations and mid-contract upgrades. The company expects to recognize roughly 55% of total RPO over the next 12 months, giving it a very visible revenue runway heading into FY2027.

For Q1 FY2027, management has guided revenue to approximately $304 million, representing 10% YOY growth, with non-GAAP diluted EPS expected at approximately $0.36. For the full year FY2027, Box is guiding revenue to approximately $1.275 billion, up 8% YOY, with non-GAAP diluted EPS of approximately $1.55.

On the other hand, analysts are projecting Q1 FY2027 EPS growth of 100% YOY, landing at $0.06. For the full FY2027, the bottom line is estimated to grow 30.8% from the prior year to $0.34, and FY2028 EPS is expected to climb another 58.8% from the prior year to $0.54.

What Do Analysts Expect for Box Stock?

DA Davidson is not hedging its bets here. The firm reiterated its “Buy” rating and held its $45 price target on BOX stock, stating that it came away from its work with increased confidence in Box's ability to push revenue growth toward its long-term targets of 10% to 15% YOY.

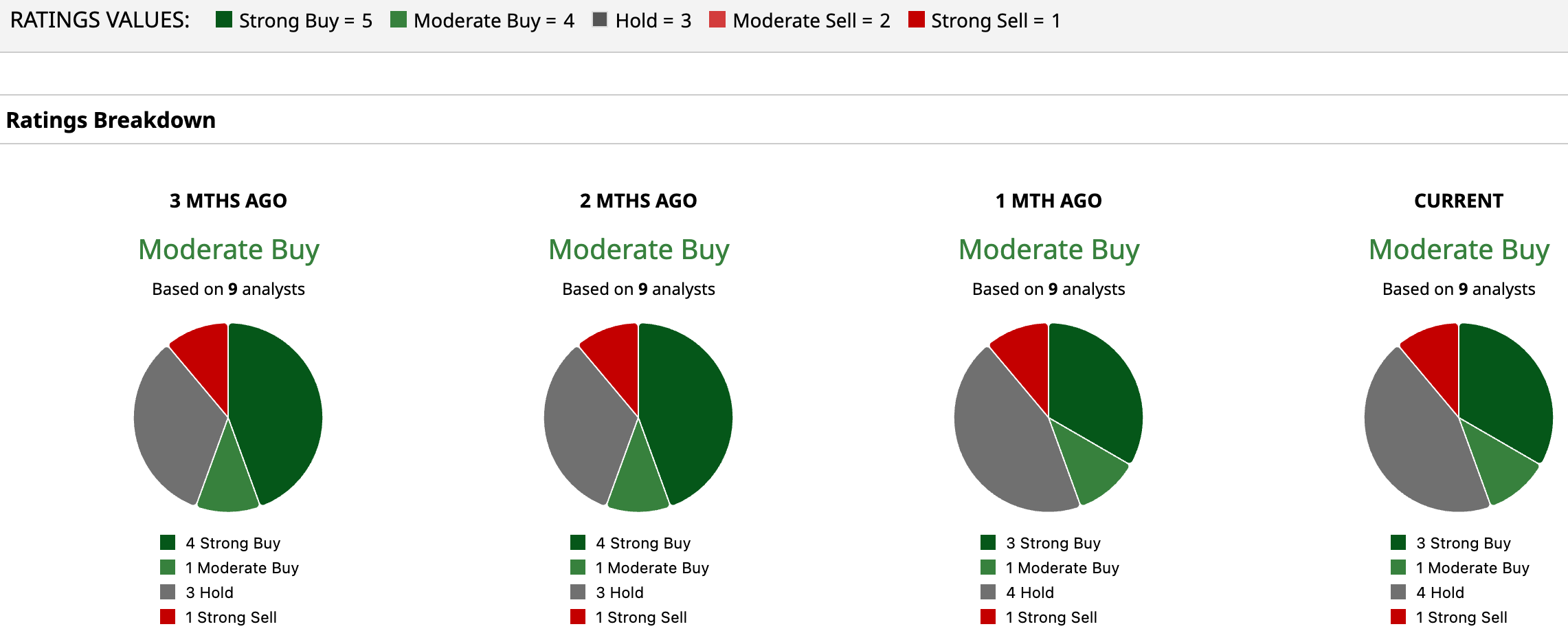

The broader analyst community has landed on a collective "Moderate Buy" rating for BOX stock. Of the nine analysts covering the stock, three have assigned it a "Strong Buy," one recommends a "Moderate Buy," four are sitting on "Hold," and one has gone ahead and stamped a "Strong Sell" on it.

The average price target on the street sits at $33.28, pointing to meaningful upside of 31.18%, while the Street-High target of $45 from DA Davidson suggests a gain of 77.4% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)