CarMax (KMX) has spent years building itself into America’s biggest used-car retailer, with giant lots, nationwide reach, and a brand most car buyers instantly recognize. But lately, the company has looked more like it is stuck in traffic. Slowing demand, pricing pressure, and rising competition crushed momentum, sending KMX stock lower and leaving investors wondering how the industry leader lost control of the wheel.

That’s where activist investor Starboard Value entered the picture.

Led by billionaire investor Jeff Smith, Starboard recently revealed a fresh 6.2 million-share position in CarMax worth roughly $258 million, after first disclosing its stake in the company back in March. This was not some random trade. The hedge fund had already been pushing for changes behind the scenes, even nominated two directors to CarMax’s board.

Starboard Value believes CarMax still has the foundation to win, but management needs to move faster. The activist investment firm sees opportunity in tightening costs, modernizing pricing systems, and improving CarMax’s online trade-in process as more shoppers compare deals digitally. Starboard believes smarter real-time pricing and leaner operations could help CarMax regain market share and restore growth momentum.

With KMX trading near long-term lows and nearly cut in half from its 52-week highs, investors are wondering whether CarMax could become a serious turnaround play again. So, should investors start buying into the activist-driven comeback story, or stay on the sidelines a little longer? Let’s take a closer look.

About CarMax Stock

Founded in 1993 and based in Richmond, Virginia, CarMax has grown into one of America’s biggest names in used-car retail. The company sells everything from everyday commuter cars to luxury, hybrid, and electric vehicles through its nationwide network. Beyond vehicle sales, CarMax also runs financing operations through CarMax Auto Finance, helping customers across different credit profiles secure loans.

The company additionally offers auctions, repair services, and protection plans, building a full-service ecosystem around the used-car business. CarMax currently carries a market capitalization of roughly $5.14 billion.

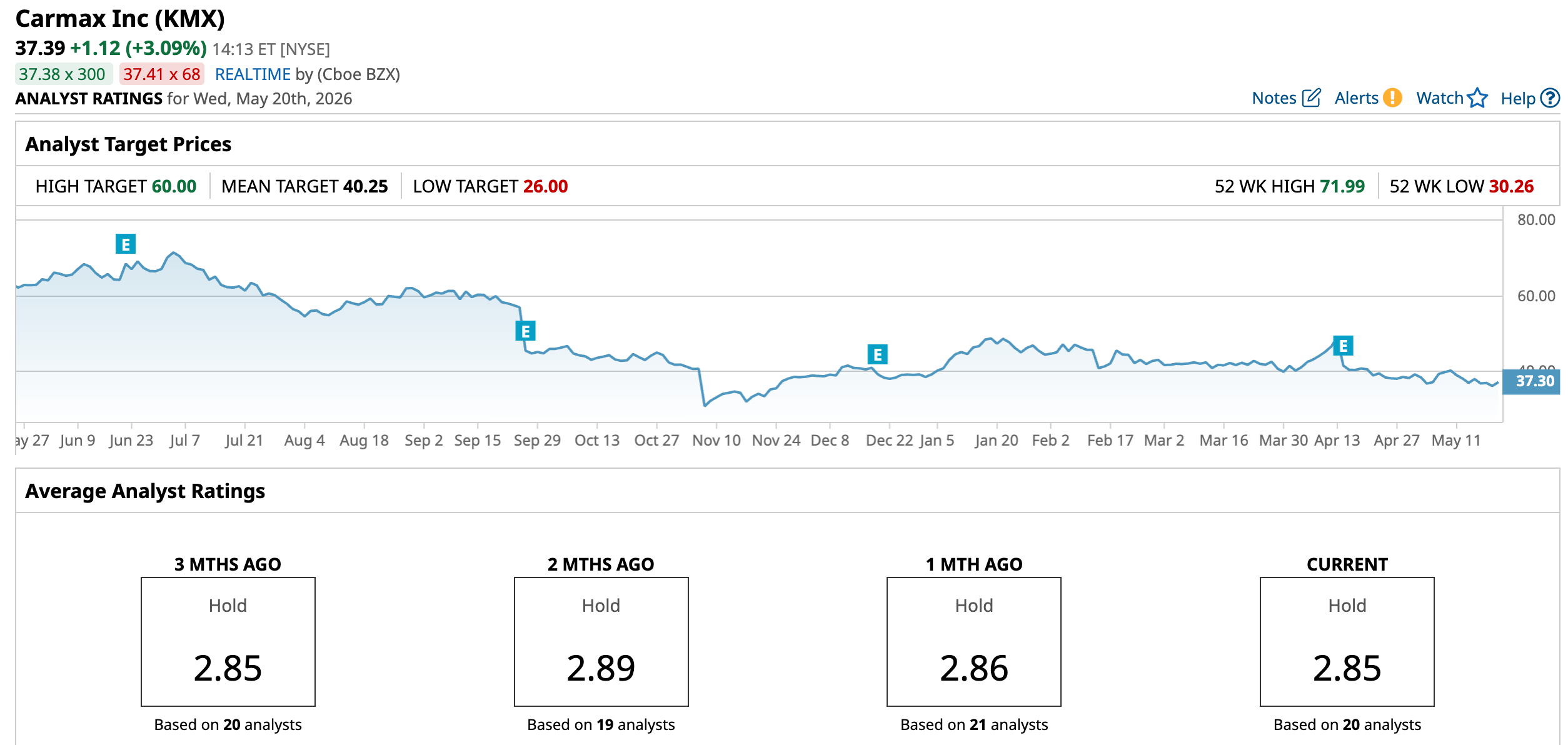

Shares of the used car dealership chain have been stuck in a long downtrend, showing the difficulty of the current car market. KMX plunged to a 52-week low of $30.26 in November before staging a modest rebound. Even after climbing 23.7% from those lows, the stock is still down 44% over the past year. And since peaking at a high of $71.99 last July, shares have been cut almost in half.

Still, the chart is beginning to show a few early signs that selling pressure may be cooling off. The 14-day RSI has cooled to 43.77 after briefly nearing overbought territory in April, suggesting the stock has pulled back enough to ease some of the overheated buying pressure. While KMX is not yet in deeply oversold territory, the current reading indicates momentum has weakened considerably, and the recent selloff may be starting to stabilize.

Meanwhile, the MACD indicator is flashing an early bullish signal. The MACD line recently crossed above the signal line, while the histogram has moved back into positive territory, and that’s often viewed as a sign that momentum could slowly be shifting back in buyers’ favor.

Valuation-wise, CarMax presents a mixed picture. KMX stock trades at roughly 16.11 times forward adjusted earnings, still slightly above many sector peers, suggesting investors continue to value its scale and brand strength. But its forward price-to-sales ratio of just 0.20 times sits below both the industry average and the stock’s historical median.

A Closer Look at CarMax’s Q4 Report

CarMax’s fiscal Q4 2026 earnings report, released on April 14, looked like one of those quarters where the headline numbers were not terrible at first glance, but investors quickly realized the deeper story underneath was far less encouraging. The used-car giant generated a revenue of $5.95 billion, down 1% year-over-year (YOY), though still slightly ahead of Wall Street's expectations. Adjusted EPS slipped 46.9% annually to $0.34, but exceeded estimates.

Once investors looked beyond those numbers, the pressure inside the business became harder to ignore. Retail sales were soft. CarMax sold 181,188 used vehicles during the quarter, while comparable-store used unit sales slipped 1.9% YOY. The bigger issue was profitability. Retail gross profit per used vehicle dropped to $2,115, down $207 from last year, after CarMax cut prices to improve sales trends and stay competitive.

Wholesale performance also showed cracks, with profit per unit falling by $105 to $940 even as wholesale vehicle unit sales rose 3% to 122,781.

That pressure hit margins hard. Total gross profit fell 9.4% annually to $605.3 million.

Then came the number that likely rattled Wall Street most. While CarMax reported positive adjusted earnings, its actual GAAP results showed a quarterly loss of $0.85 per share – a sharp contrast that raised concerns about the true earnings power of the business. Even for the full fiscal year, GAAP EPS dropped to $1.68 from $3.21 a year earlier.

Furthermore, investors appeared worried that CarMax is spending aggressively in a weak environment. The company continued repurchasing shares, buying back nearly $632 million worth during fiscal 2026, while ending the year with just $122.8 million in cash and cash equivalents against more than $2 billion in long-term debt. At the same time, management still plans to expand operations with new stores, auction centers, and roughly $400 million in capital spending during fiscal 2027.

That combination of falling profits in fiscal 2026, weaker margins, Q4 GAAP losses, and ongoing spending explains why KMX stock plunged 15.1% after the report. Investors were reacting to fears that CarMax may need much longer to fully stabilize its business in a tougher used-car market.

Analysts expect the company’s adjusted EPS for fiscal 2027 to decline 21% YOY to $2.30 before surging by 23% annually to $2.83 in fiscal 2028.

What Do Analysts Expect for CarMax Stock?

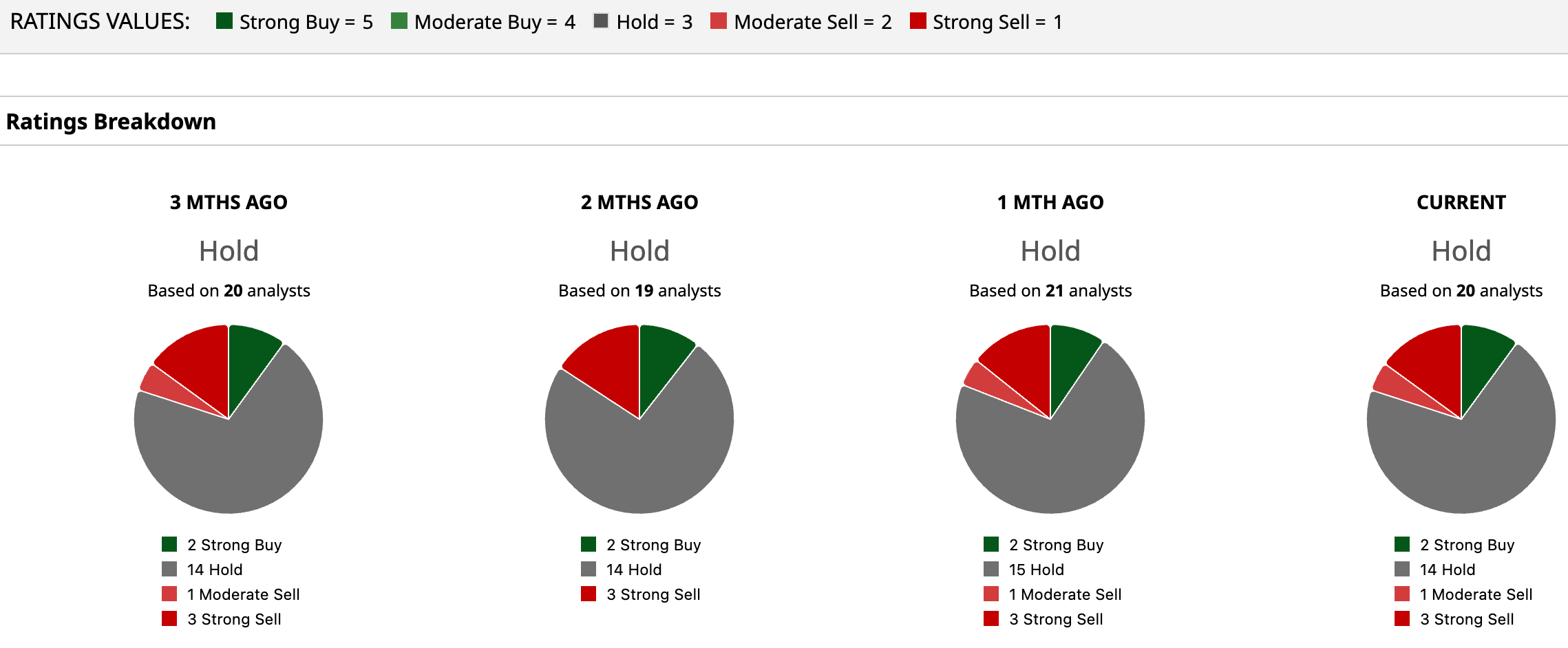

KMX stock currently carries a consensus “Hold” rating overall. Of the 20 analysts covering the stock, two advise a “Strong Buy,” 14 play it safe with a “Hold,” one suggests a “Moderate Sell,” and three are outright skeptical, having a “Strong Sell.”

While KMX’s mean price target of $40.25 suggest a rebound potential of 7.7% from the current price levels, the Street-high target price of $60 implies that the stock could rally as much as 60.5% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)