Walmart (WMT) will release its first-quarter fiscal 2026 results on May 21. Tariffs, persistent inflation concerns, and rising gas prices have created a tougher environment for consumer-focused companies. However, Walmart could once again deliver strong growth driven by its diversified revenue mix.

Notably, Walmart shares have climbed 19% since the start of the year, despite concerns about inflation and macroeconomic uncertainty. The growth reflects the retailer’s ability to drive traffic across its brick-and-mortar and e-commerce channels and deliver profitable growth.

Here’s a closer look at the key metrics and trends investors should watch for in Walmart’s upcoming earnings report.

Walmart's Q1 Preview

Walmart appears well-positioned to deliver a strong Q1 performance, driven by steady momentum across its core businesses. The retailer continues to benefit from its scale, value-focused strategy, and rapidly expanding e-commerce operations. At the same time, higher-margin businesses such as advertising and membership programs are becoming increasingly important contributors to profitability.

E-commerce remains Walmart’s biggest growth engine. Management expects digital operations to lead overall revenue growth, supported by stable gains in store and club sales. Growth is also expected to be broad-based, with both U.S. and international markets contributing meaningfully.

In the United States., Walmart is likely to continue seeing strong comparable sales growth, driven by higher customer traffic in stores and online. Services like pickup and home delivery remain popular with consumers, helping sustain digital sales momentum. Advertising revenue is also emerging as a larger contributor to total revenue, reflecting Walmart’s ability to monetize its massive customer base and retail platform.

International operations are expected to remain another key strength. Higher transaction volumes and unit sales across multiple regions should help Walmart continue gaining market share globally. E-commerce growth has been particularly strong in India and China, where the company has aggressively expanded its digital presence.

Advertising is becoming one of Walmart’s most attractive long-term growth opportunities due to its high margins. In the U.S., Walmart Connect continues to attract more advertisers, while international ad growth is being driven largely by Flipkart in India. These businesses not only add revenue but also support stronger operating margins.

Membership income is also emerging as a meaningful earnings driver. Company-wide membership revenue is expected to increase, supported by strong international growth, especially at Sam’s Club China. In the U.S., Walmart+ continues to generate double-digit membership income growth. These recurring revenue streams help diversify earnings and create a more stable base of profitability.

For Q1, management expects constant-currency sales growth of 3.5% to 4.5%. Walmart’s earnings mix is also shifting toward higher-margin businesses such as advertising and memberships, which should support stronger bottom-line performance. Improving profitability in Walmart U.S. e-commerce operations and at Flipkart is adding further support.

Operating income is projected to rise 4% to 6% in the quarter, driven mainly by advertising and membership growth. Margins are expected to improve due to a more favorable business mix, productivity gains, automation benefits, and lower pressure from merchandise mix changes.

Walmart’s automation investments are also delivering results. More than 60% of Walmart U.S. stores now receive freight from automated distribution centers, while over half of e-commerce fulfillment volume is handled through automated facilities. These efficiencies are helping lower costs and strengthen margins.

Management expects Q1 adjusted EPS between $0.63 and $0.65, while Wall Street forecasts EPS of $0.65, representing roughly 6.6% year-over-year (YOY) growth.

Is Walmart Stock a Buy Ahead of Q1 Earnings?

Walmart is heading into the Q1 earnings release with multiple growth drivers working in its favor. Strong e-commerce momentum, rising advertising revenue, growing membership income, and increased automation efficiency could help the retail giant deliver another quarter of profitable growth.

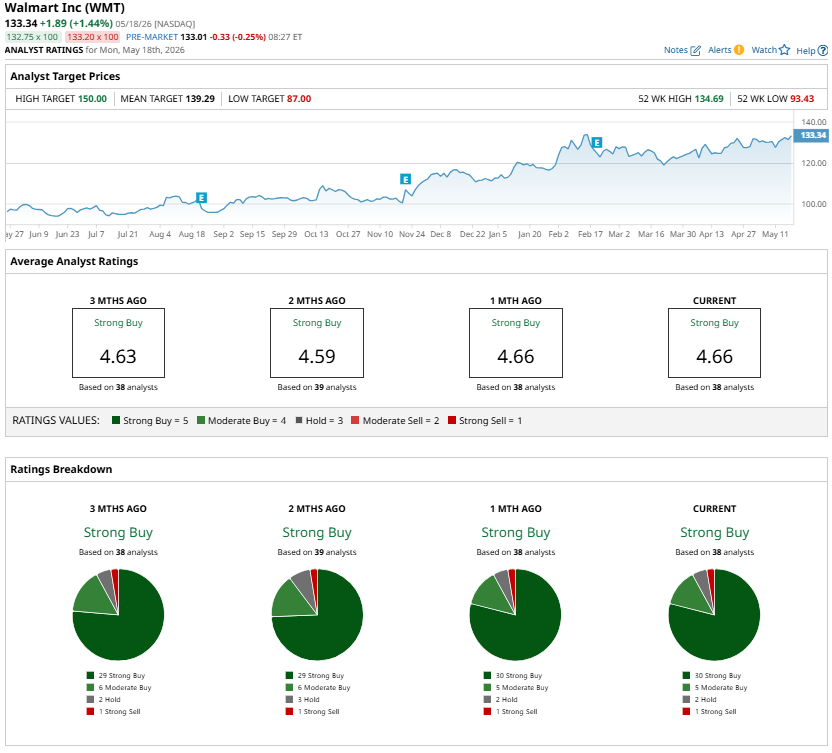

Wall Street analysts remain bullish on WMT stock ahead of earnings, strengthening its appeal as a long-term investment. However, there’s one key concern investors shouldn’t ignore: valuation. Walmart currently trades at a forward price-to-earnings (P/E) ratio of 46 times, suggesting much of the optimism may already be priced into the stock.

In short, Walmart could post strong Q1 results despite ongoing macro challenges, but a pullback could be a better buying opportunity.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)