/NVIDIA%20Corp%20logo%20on%20phone-by%20Evolf%20via%20Shutterstock.jpg)

Nvidia (NVDA) will release its first-quarter fiscal 2027 financial results on Wednesday, May 20. Despite dominating the artificial intelligence (AI) boom, Nvidia stock is trading surprisingly cheap, and its valuation multiple fails to reflect the company’s solid growth trajectory driven by AI infrastructure spending.

Nvidia continues to benefit from a massive surge in demand for its advanced graphics processing units (GPUs), as hyperscalers and enterprises race to expand AI computing capacity. That demand wave appears far from over.

In fact, Nvidia management recently raised its expectations for next-generation AI chip platforms Blackwell and Rubin. Earlier, Nvidia projected cumulative GPU demand tied to those architectures at about $500 billion. Nvidia has now doubled that outlook, saying demand and purchase commitments could surpass $1 trillion by 2027.

That forecast highlights that a significant amount of capital is still flowing into AI infrastructure and suggests Nvidia may remain one of the biggest winners of the AI spending cycle for years to come.

With demand for AI chips remaining exceptionally strong, Nvidia could once again deliver explosive revenue and earnings growth in Q1, which may support its share price rally.

Nvidia: Blockbuster Q1 Ahead

Nvidia is poised to deliver another superstar quarter as demand for its GPUs continues to surge across hyperscalers, enterprises, and sovereign AI projects worldwide. The company’s data center business will once again account for the bulk of its revenue.

Notably, Nvidia’s data center business generated $193.7 billion in revenue in fiscal 2026, up 68% year-over-year (YOY). Nvidia’s management expects momentum to continue throughout calendar 2026, with sequential revenue growth throughout the year. In addition, Nvidia has secured sufficient supply and inventory commitments to support demand through 2027, which augurs well for growth.

A major driver behind Nvidia’s solid data center revenue is its next-generation Blackwell platform. Demand for both Blackwell and Blackwell Ultra systems continues to strengthen, positioning the company for solid growth. At the same time, Nvidia is still seeing healthy demand for its Hopper-based products. That broad adoption trend is helping Nvidia deepen its dominance across the AI ecosystem.

Beyond GPUs, networking is emerging as another powerful growth catalyst. Nvidia’s networking business surpassed $31 billion in fiscal 2026 revenue, driven by rising adoption of technologies including NVLink, Spectrum-X Ethernet, and InfiniBand.

Another rapidly expanding opportunity is sovereign AI. Revenue related to sovereign AI initiatives more than tripled YOY in fiscal 2026, surpassing $30 billion. Governments around the world are ramping up investments in domestic AI capabilities, creating a long-term tailwind that could significantly expand Nvidia’s addressable market over the next several years.

Looking ahead, Nvidia expects first-quarter revenue to reach $78 billion, up sharply from $44.1 billion in the same quarter last year. The data center segment is expected to remain the biggest contributor to that growth.

Profit growth is also expected to remain exceptionally strong. Wall Street analysts forecast earnings of $1.70 per share, representing a 120.8% YOY increase. Notably, Nvidia has beaten analyst EPS expectations in each of the past three quarters, raising expectations that it could again surpass Q1 estimates.

Nvidia’s Valuation Suggests More Upside

While Nvidia is likely to deliver solid growth in Q1 and beyond, NVDA stock trades cheap. The stock trades at 30.1 times forward earnings, which appears significantly low given its growth potential. Analysts expect Nvidia’s earnings growth of 71.6% in fiscal 2027, followed by a solid 34.1% jump in fiscal 2028.

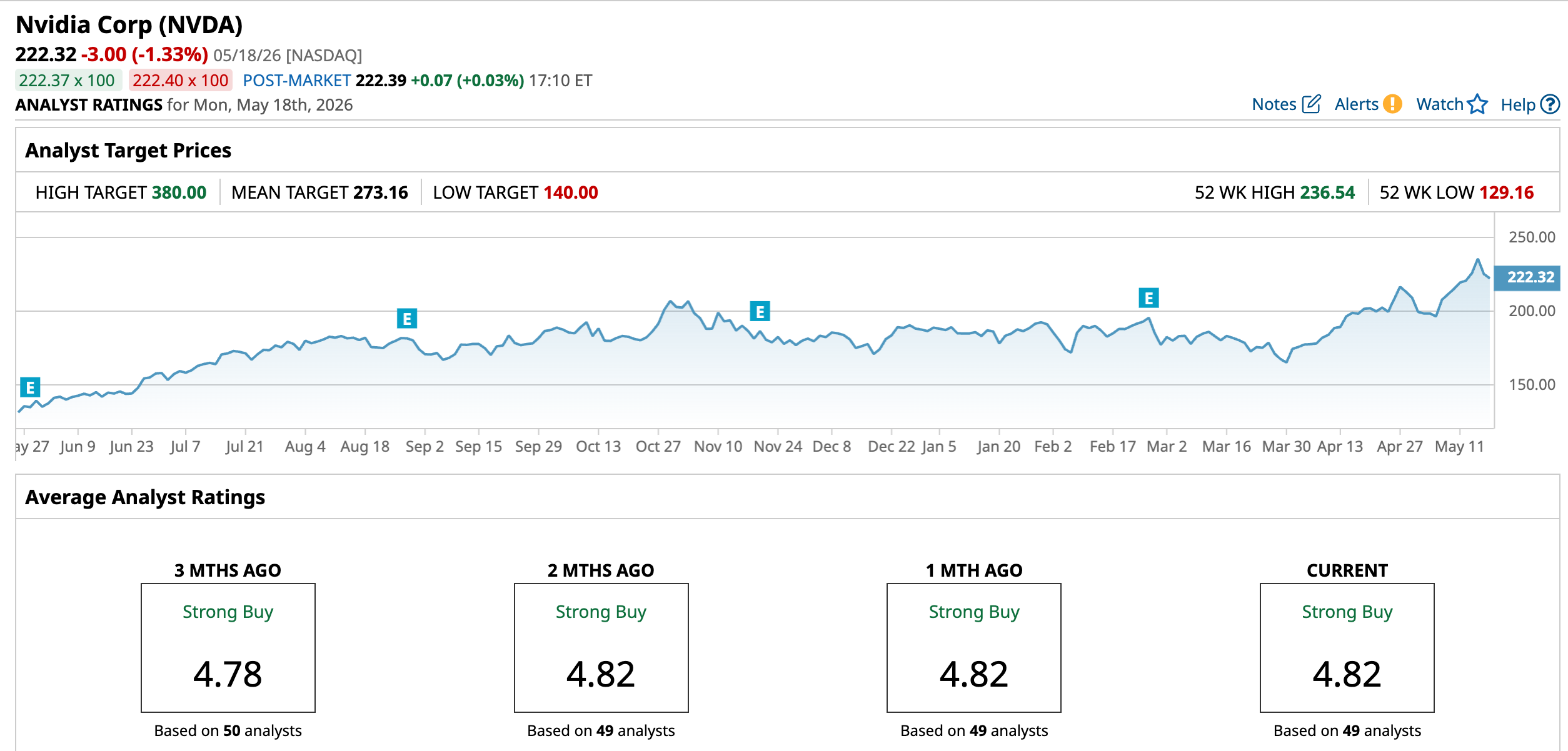

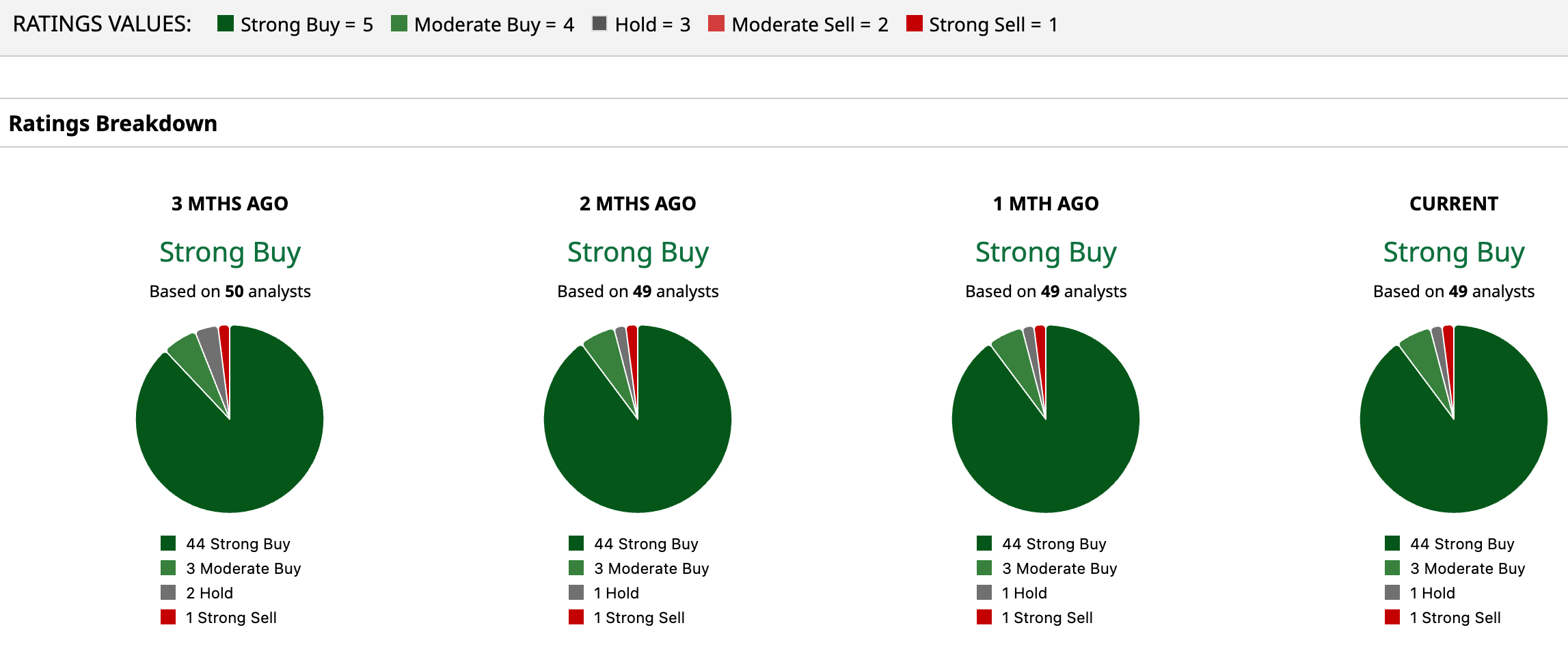

With AI spending continuing to soar, Nvidia’s expanding revenue base, pricing power, and leadership in next-generation chips position the company for continued upside. Its ability to deliver solid growth and relatively inexpensive valuation makes it too cheap to ignore ahead of Q1. Wall Street is bullish, maintaining a “Strong Buy” consensus rating for NVDA.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)