Howdy market watchers!

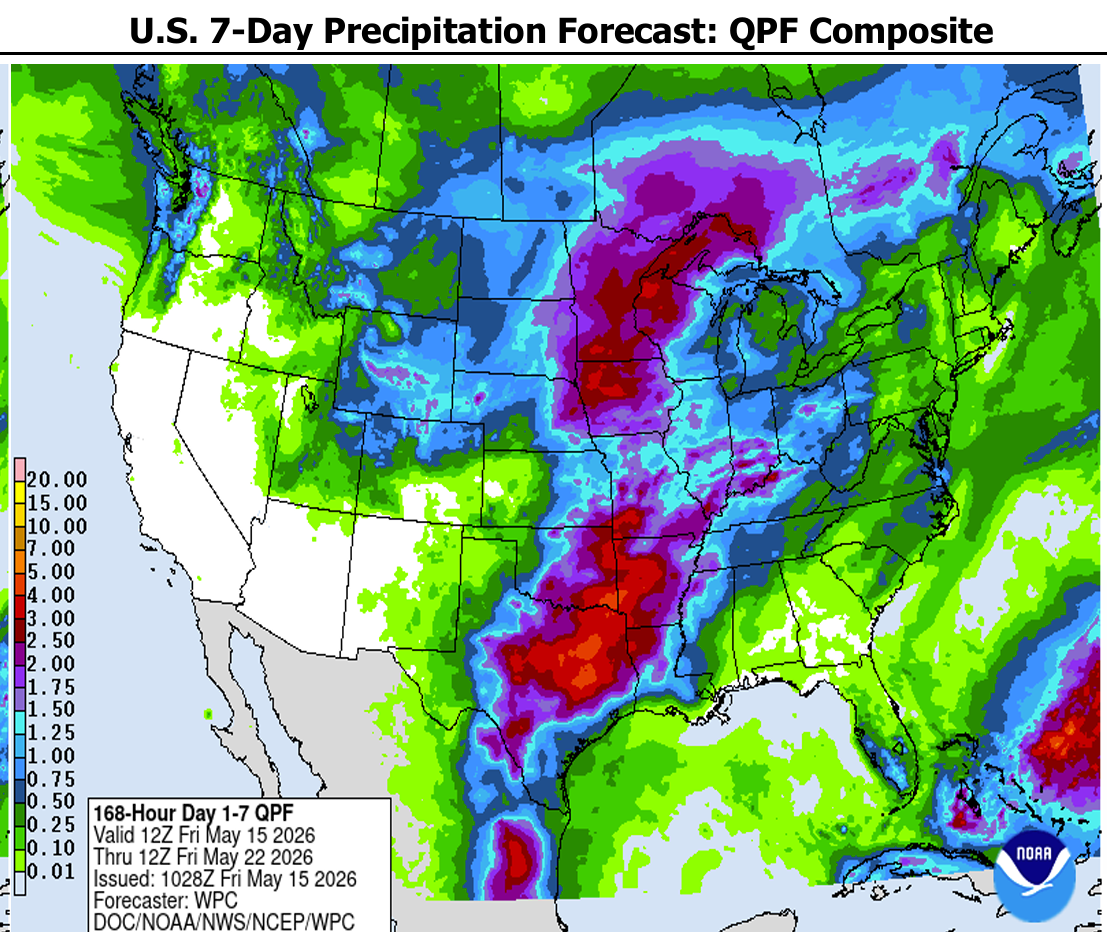

There are finally some meaningful rainfall chances in the nearby forecast for the Southern Plains! Praise the Lord! Western Kansas, the Oklahoma and Texas Panhandles however largely miss out.

In a “normal” year, this would be perfect to help the winter wheat crop heads and berries finishing filling. We are at least two to three weeks ahead of “normal” and the wheat crop is basically ripe! In fact, harvest has already begun in south and central Oklahoma.

All the old timers that I’ve talked to have never seen the crop this mature this early. The end of May is usually the earliest that we cut wheat in northern Oklahoma, but we could be starting by this weekend or early next week if it doesn’t rain.

While rain is too late for this year’s winter wheat crop, it is critical timing for grass pastures as well as recently planted corn, soybeans, milo and other crops soon to be planted. Given the heat and poor conditions, wheat harvest will likely be underway from Texas all the way to Nebraska around the same time.

It will be a difficult year for custom harvester crews as fewer acres as well as yields limit the revenue side while higher fuel, insurance and other operating costs have risen significantly. In fact, all of agriculture and other businesses that operate heavy equipment are all in the same boat, as we say.

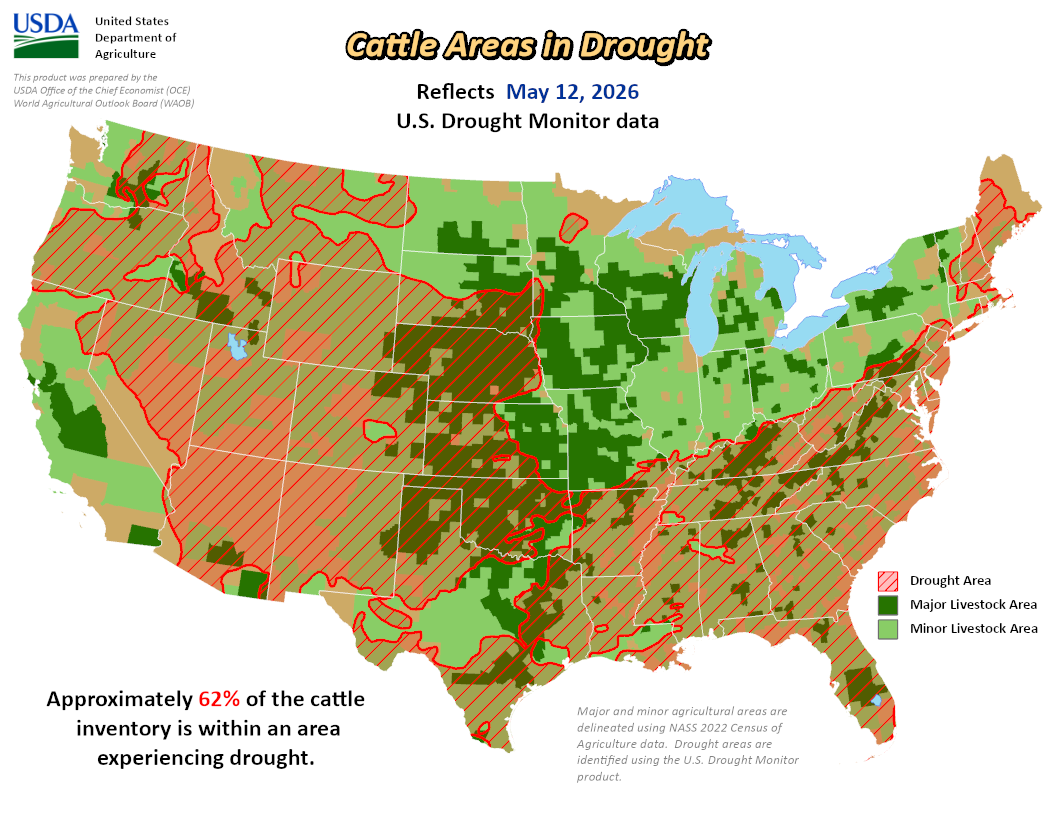

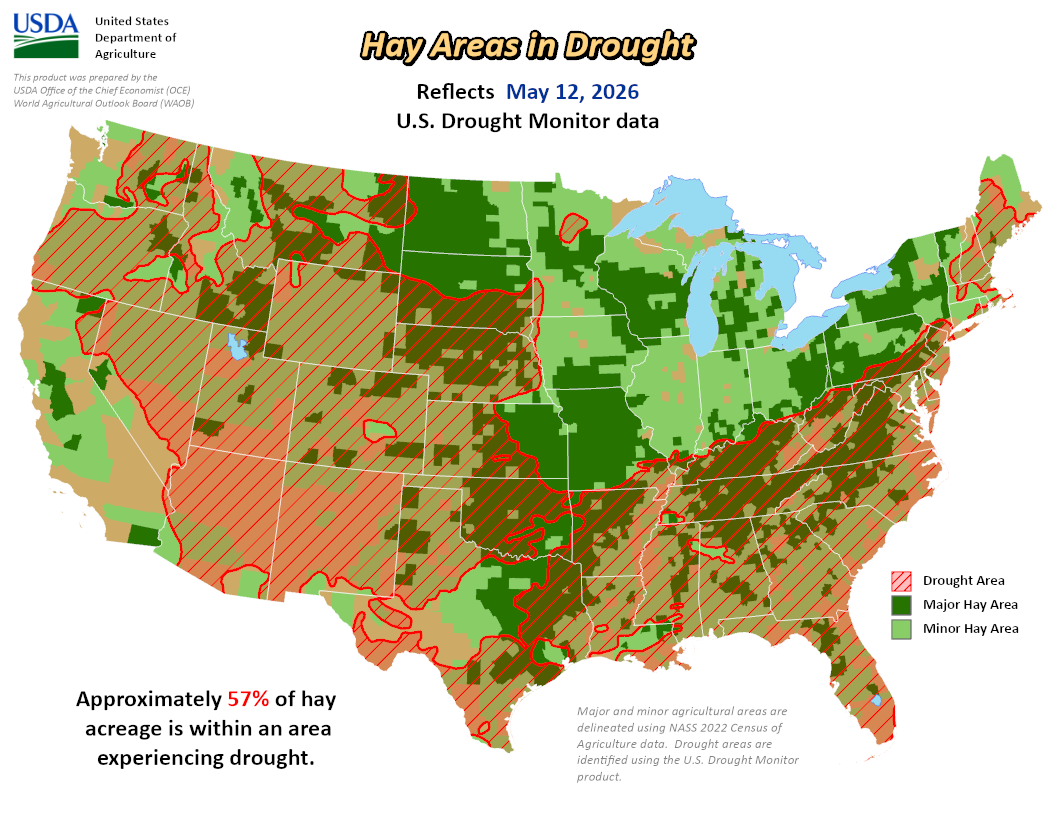

With cattle prices elevated, it is time to retain heifers and grow the cow herd, but the worsening drought across the Plains is beginning to impede the ability of even the most willing to be able to do so. Wildfires and the lack of spring rains have severely limited the availability of grass as we transition from winter forage to summer grazing. Without precipitation soon, the condition of pastures is going to really start going backwards with the need for hay potentially returning if herds are retained.

We’ve been hearing more talk of additional culling in Nebraska and parts of Texas in recent weeks due to persisting drought conditions given the lack of spring green up. This situation will only postpone the rebuilding of the US cow herd that is already at a 75-year low.

The biggest story in grain production at the moment is that of the US winter wheat crop. Conditions have continued to deteriorate on a weekly basis with this week’s Good-to-Excellent rating at just 28 percent versus 32 percent expected and 54 percent last year. In one week, Texas G/E ratings declined 6 percent to just 10 percent. Oklahoma declined another 7 percent to just 9 percent G/E. Kansas declined another 5 percent to 17 percent G/E and Nebraska declined 6 percent to only 5 percent G/E. This is indeed a year for the record books.

The USDA released its monthly Crop Production and World Supply and Demand reports on Tuesday as well as the first Winter Wheat Production reports for 2026. Every single state in the nation saw a reduction in winter wheat production relative to last year largely driven by expectations for harvested acres in addition to yield declines. Kansas wheat production was reduced by 132.2 million bushels, Oklahoma by 42.0 million bushels, Texas by 37.5 million bushels, Colorado by 37.46 million bushels and Nebraska by 21.595 million bushels. For all wheat classes, production is expected to be 354.044 million bushels below last year although we did have a big crop last year. To put this into perspective, this is expected to be the smallest wheat crop in the US since 1972 and the smallest hard red winter wheat crop in the US since 1957! Now that is saying something!

At the Oklahoma State University Wheat Field Day in Lahoma, Oklahoma, on Friday at the Dr. Raymond Sidwell Research Facility, producers gathered to hear from Dr. Brett Carver and wheat breeders from private seed companies with the backdrop of trials that looked ready to harvest. Usually, there is still plenty of green still in the trials. By every stretch, this is a record year, but not one to brag about.

The 3-day Kansas wheat tour concluded this Thursday visiting over 400 fields across Kansas with a few in northern Oklahoma and southern Nebraska. As we saw from the prior week’s Oklahoma tour that pegged yields at just 23.11 bushels per acre, expectations were low. The average yield for Kansas by 60 scouts from 16 states was 38.9 bushels per acre. This was higher than I was expecting and higher than USDA’s 37.0 bpa from Tuesday’s report. The USDA expects Oklahoma’s average yield to be 28.0 bpa. We truly will not know until combines get into the field and harvest is complete.

Also, a lot of acres have been baled for hay after crop insurance called it a disaster. With limited foliage due to drought and hot temperatures since the beginning of the year, there wasn’t even much to bale.

Speaking with a fellow seed wheat dealer out of Hobart, Oklahoma, he said they will not even be getting the combine out of the barn this year and believe there is a 45-mile radius where that is the case. Just think about that for a minute. That is unheard of! There will undoubtedly be a shortage of seed wheat this year. We welcome the rains ahead, but a mature crop and rain can lead to reduced test weights. So far, I’ve heard test weights starting around 57-58 pounds per bushel. This is low for starting out with rain ahead.

Wheat prices spiked after the extent of USDA’s cut of the US wheat crop in Tuesday’s report that actually reached limit up of $0.45 per bushel! In my trading career, I have not seen wheat limit up, even during Russia’s attack on the Ukraine as I recall. Expanded limits of $0.70 per bushel were in place Wednesday, but it was relatively quiet session after making new highs and closing lower on the day.

The further surprise came from the downward action in the wheat market on Thursday, that was also the last trading day for May grain futures, and especially Friday. However, the gaps filled on the wheat charts, expect for the much lower gap at $6.09 on July KC wheat futures, with KC wheat closing back above the 20-day moving average. It is true that the wheat crop issue is largely in the US versus globally although there are issues elsewhere with high fertilizer prices beginning to be a concern in other countries. However, higher prices in the US should lead to lower exports out of the US due to competitiveness on the global market, which in turn can reduce prices with demand rationing due to higher prices. There was actually an outside key reversal lower in the Chicago wheat contract starting Thursday, but still managed to close above the 20-day moving average on Friday.

Having said that, the selloff was across the entire grain complex led lower by soybeans with the bulls expecting China purchase announcements from the US following President Trump’s meetings with President Xi on Thursday and Friday. There was no news on Thursday and then no news on Friday either except for some Boeing purchases. After the recent rally, the soybean, corn and wheat markets gave back much of it without fresh news to feed the bulls.

The US dollar has also rallied back quite a bit this week on hotter April inflation reports in the US, rising 0.6 percent from the prior month and 3.8 percent annually, the highest since May 2023. There is a higher chart gap on the US dollar index, which started to be filled on Friday, as I discussed in last week’s article as being a target. In fact, the US dollar index gapped higher on Friday’s open on Thursday evening and so now there is a lower gap in its wake.

We now have a new Fed Chair with Kevin Warsh's final confirmation by the US Senate. He comes in at a time with the President is seeking aggressive interest rate cuts when the data doesn't support that move. Say what you want, but Fed Chair Powell, having personally met the man several times, has been a very competent and responsible Fed Chair that has managed to fight for independence of the Federal Reserve from politics and keeping monetary policy steady at a time of stubbornly firm inflation, bolstered by the surge in oil prices.

Corn and soybean planting in the US are ahead of average while harvest of soybeans is complete in Brazil and back on track both there and in Argentina for corn and soybeans.

The USDA pegged 2026/27 US ending stocks for corn at 1.957 billion bushels versus 1.923 billion bushels expected. US soybean ending stocks came in lower than expected at 310 million bushels versus 355 million bushels expected.

Brazil and Argentine corn crops came in slightly higher than expected while soybeans were lower than trade guesses.

Globally, anticipated corn and wheat ending stocks for 2026/27 were quite bit lower than expected while soybeans were slightly smaller than expected. China corn imports were unchanged at 6.0 million metric tons while soybean imports are said to increase to 114.0 MMT, 2.0 MMT above last year.

There was a lot to cover on the grain markets this week, but there has also been plenty to cover in cattle as well and so here we go. The cattle markets have been very choppy since the new highs on May 1st. Consumer demand for beef has been surprisingly resilient, but financial stress must be increasing with higher fuel, grocery, rent, insurance and living costs. Despite this and fewer cattle to slaughter, demand has continued to march on relative to the cheaper, alternative proteins.

As inflation fears grow as the Mid-term elections approach, this topic is becoming more political by the day. We saw that this week when President Trump was rumored to sign an Executive Order to relax restrictions on beef imports from Brazil and all countries. The market plummeted on the news, but then recovered with news that Trump delayed signing such order after industry voices reached him. This is still a threat for the cattle market as the pressure to win in November amplifies while the Iran negotiations and resulting higher fuel prices seem further from a resolution with every round of “talks”.

The Iranian regime has lost a lot, but it seems they have less to lose at this point than the Trump Administration. This was discussed at a high level in China, a key player in this chess match, but we really don’t have enough leverage on China to forcefully ask them to direct the Iranian regime to capitulate. President Trump said that President Xi confirmed that China would not send military arms to Iran at a time when the US is said to be sending military arms to Taiwan. Iran is now leverage for China with the US over support of Taiwan.

There seemed to be a win for US beef in the PRC with the news that 200 processing plants had licenses renewed to export to China, but then it was said that all of these licenses were still seen as inactive on the Customs site.

The worsening drought situation in US cattle country is truly concerning and how we got here in the first place. It complicates this cattle cycle as it limits our ability to rebuild with the high-priced incentives offered by the market and is likely to force more imports that are likely to structurally change the US market indefinitely.

Cattle had a strong recovery on Friday with fed cattle cash trade throughout the week reaching new highs. I believe we could see further recovery in futures early next week, but it feels less likely that we are going to get back to the recent highs, at least at this stage.

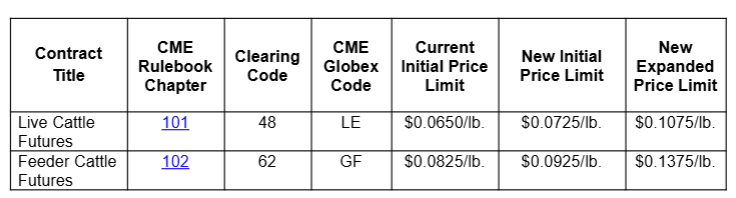

The CME will be increasing daily limits on cattle futures effective June 1, 2026. Live cattle futures daily limit will increase to $7.25 per cwt, where we’ve been before, from $6.50 with expanded limits at $10.75 per cwt. Feeder cattle futures daily limit will increase to $9.25 per cwt, where we’ve also been before, from $8.25 per cwt and expanded limits at $13.75 per cwt.

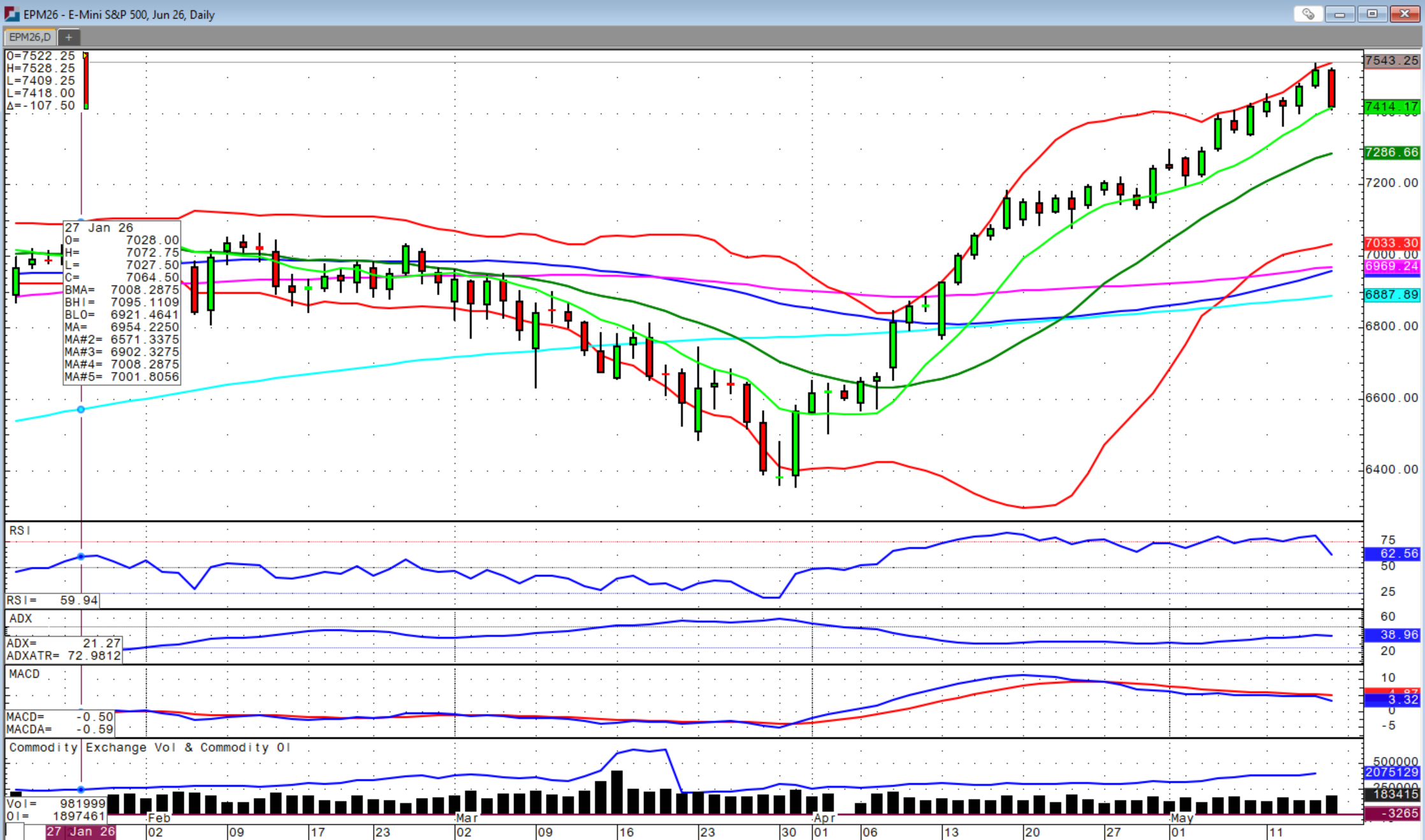

The old adage in equity markets of sell in May and go away (for the summer) may be different this year, but we need to be cautious of growing pressures on the economy to result in a correction in the stock market that spills over into cattle. The S&P 500 made new, all-time record highs this week above 7,500.

There is talk that the highs in the cattle market are not yet in and may not be until 2027, but just know that volatility in this market can appear at times when you need to sell that could coincide with a point of liquidation by the funds and take the cattle market to oversold levels. These levels are worth protecting, in my opinion, even though I do believe we could go higher under all the right circumstances. We can also always go lower and much lower for that matter.

Just look at the wheat market this week while conditions are historically low. Markets overextend on both the upside and downside and often more than we expect or is rational. If you don’t want to protect them all, protect a portion and sleep better as absolutely anything can happen in this very uncertain and volatile market environment.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Eli%20Lilly%20%26%20Co_%20by%20Tada%20Images%20via%20Shutterstock.jpg)