The market has spent the last two years rewarding almost any company tied to GLP-1 weight-loss drugs. Investors watched demand for treatments like Wegovy and Ozempic reshape health care, telehealth, and even food stocks. But what happens when growth stops being cheap?

That’s the question shareholders are suddenly asking after Hims & Hers Health (HIMS) reported first-quarter earnings that showed the hidden cost of chasing the hottest trend in health care. The telehealth company is still growing, still adding subscribers, and still expanding internationally. Yet the market focused on one number above all others — a surprise loss that erased the illusion that GLP-1 expansion would be painless.

Hims & Hers Just Hit a Profitability Speed Bump

Hims & Hers reported Q1 revenue of $608.1 million, up 4% year-over-year. Subscribers climbed 9% to nearly 2.6 million. Those are healthy growth figures for most health care platforms. But earnings told a different story.

The company swung to a net loss of $92.1 million, or $0.40 per share, compared to a profit of $49.5 million, or $0.20 per share, a year ago. Wall Street had expected a profit of $0.04, not a loss. Gross margin also narrowed to 65% from 73% last year.

That’s why the stock dropped roughly 14%.

Surprisingly, the problem wasn’t weak demand. It was the opposite. Hims is spending aggressively to transition from higher-margin compounded GLP-1 products to branded drugs supplied through its partnership with Novo Nordisk (NVO).

That shift matters because compounded drugs carry better margins. Branded drugs, though, bring more legitimacy and less regulatory risk — but they also come with thinner profits. Hims may make more revenue dollars but keeps fewer of them.

Management also booked roughly $33.5 million in restructuring and inventory-related charges tied to the GLP-1 transition.

The Novo Nordisk Deal Could Still Be a Long-Term Win

Investors shouldn’t ignore the strategic upside here. Earlier this year, Hims resolved its dispute with Novo Nordisk and secured access to branded Wegovy and Ozempic products through its platform. That instantly gave Hims credibility in one of the fastest-growing pharmaceutical markets in the world.

Granted, margins are taking a hit today. But the partnership reduces legal uncertainty and positions Hims as a more mainstream health care provider instead of merely a low-cost workaround for drug shortages.

The company is also pushing hard internationally. Revenue outside the U.S. jumped to $78.2 million from just $7.3 million a year ago. That expansion won’t come cheaply either. Hims is investing in diagnostics, AI tools, and acquisitions, including its proposed $1.15 billion purchase of Eucalyptus, a digital health company. Management is prioritizing scale over near-term profitability.

The gamble is straightforward: sacrifice margins today to build a much larger health care ecosystem tomorrow.

What Analysts Think About HIMS Stock

Analysts appear divided between excitement about growth and concern about sustainability.

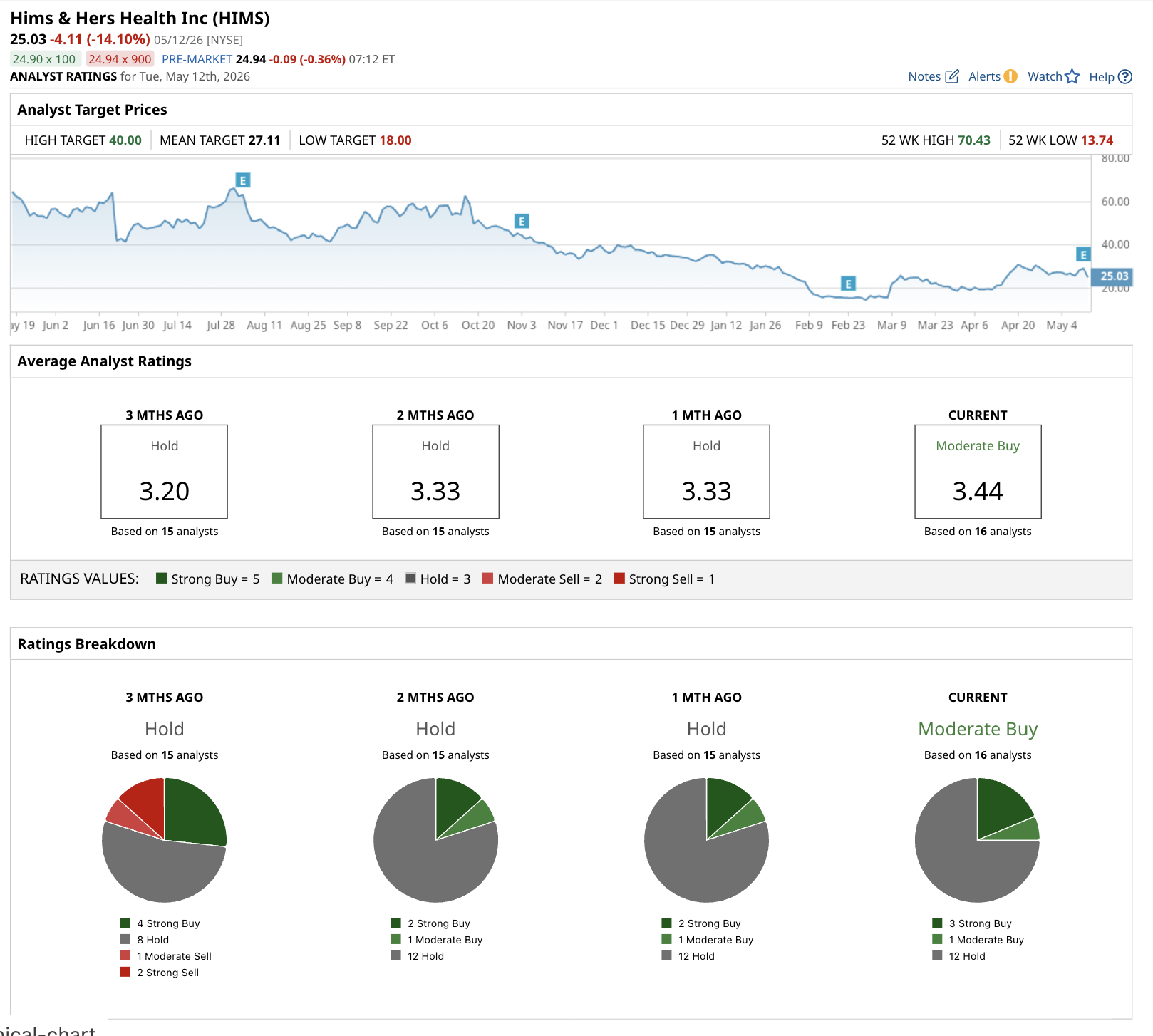

According to Barchart's analyst ratings', the stock currently carries a “Moderate Buy” consensus rating based on 16 analysts. The broader analyst community remains cautious, with three "Strong Buy" ratings, one "Moderate Buy," and 12 "Hold."

Bank of America analysts recently warned investors may be too optimistic about retention rates for branded GLP-1 subscribers and the long-term durability of Hims’ pricing strategy. They also noted recent Wegovy subscriber growth could partly reflect temporary promotional pricing and the shift away from compounded prescriptions.

Price targets also show just how wide the debate has become. Analyst targets currently range from roughly $18 on the low end to $40 on the high end, while the mean price target is $27.11, implying 8.3% upside potential — but there is nowhere near universal confidence.

Bottom Line

In short, Hims & Hers just learned the same lesson many fast-growing health care companies eventually face: Explosive demand does not automatically produce explosive profits.

The company is making expensive but rational decisions. Moving toward branded GLP-1 drugs lowers regulatory risk. Expanding internationally broadens the addressable market. Investing in technology and diagnostics could deepen customer loyalty over time.

But shareholders also need to accept that those investments will pressure margins for a while.

When all is said and done, this quarter looked less like a broken growth story and more like a company paying the entry fee for a larger future. The question now is whether investors have the patience to wait for it.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)