The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Clorox (NYSE:CLX) and the rest of the household products stocks fared in Q1.

Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options. These trends can be double-edged swords that benefit companies who innovate quickly to take advantage of them and hurt companies that don't invest enough to meet consumers where they want to be with regards to trends.

The 10 household products stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 2.7% while next quarter’s revenue guidance was in line.

While some household products stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 3.5% since the latest earnings results.

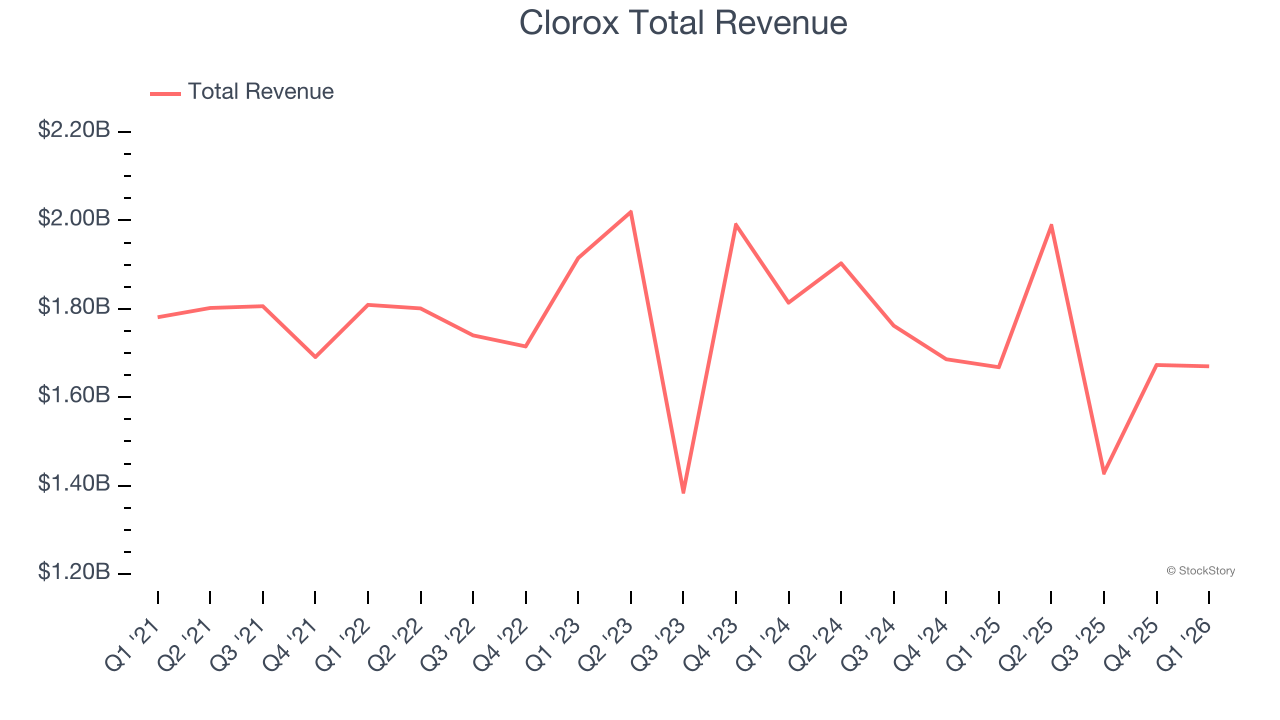

Clorox (NYSE:CLX)

Founded in 1913 with bleach as the sole product offering, Clorox (NYSE:CLX) today is a consumer products giant whose product portfolio spans everything from bleach to skincare to salad dressing to kitty litter.

Clorox reported revenues of $1.67 billion, flat year on year. This print was in line with analysts’ expectations, and overall, it was a satisfactory quarter for the company with an impressive beat of analysts’ EBITDA estimates but a miss of analysts’ gross margin estimates.

"Our third-quarter results were mixed, with continued momentum in some parts of our portfolio and slower-than-anticipated market share recovery in others," said Chair and CEO Linda Rendle.

The stock is down 4.7% since reporting and currently trades at $91.91.

Is now the time to buy Clorox? Access our full analysis of the earnings results here, it’s free.

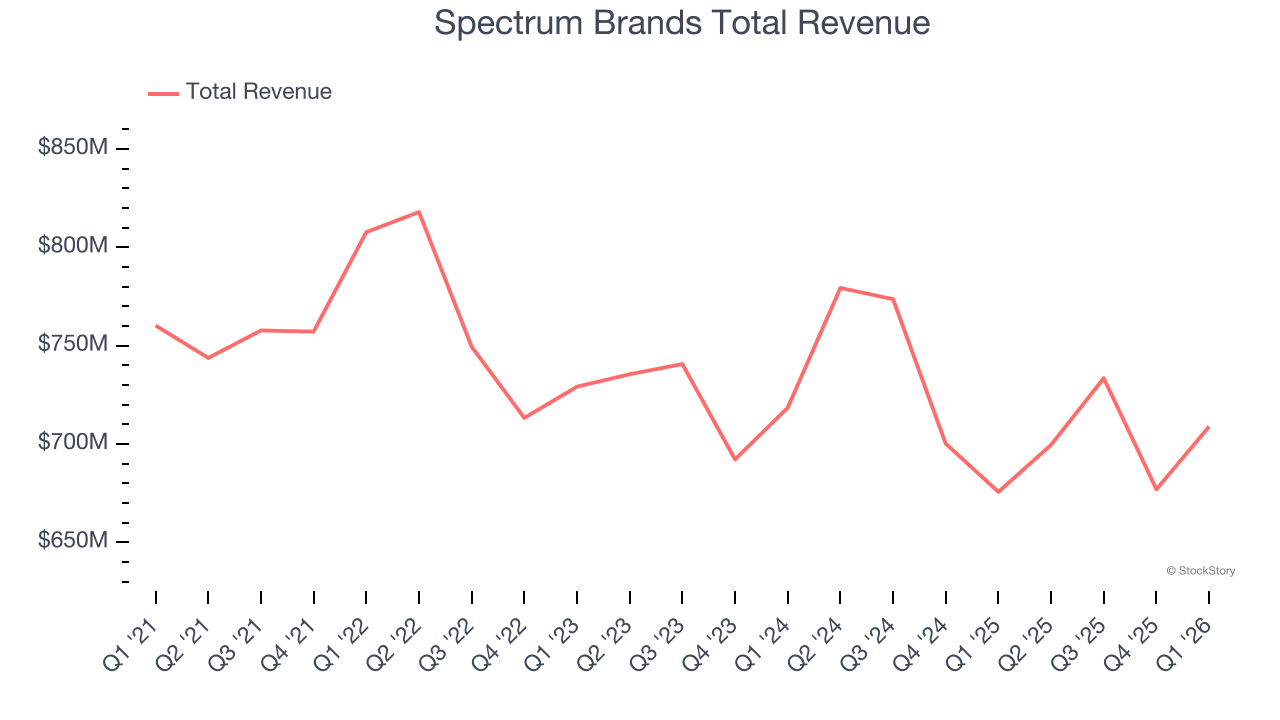

Best Q1: Spectrum Brands (NYSE:SPB)

A leader in multiple consumer product categories, Spectrum Brands (NYSE:SPB) is a diversified company with a portfolio of trusted brands spanning home appliances, garden care, personal care, and pet care.

Spectrum Brands reported revenues of $708.9 million, up 4.9% year on year, outperforming analysts’ expectations by 4.4%. The business had a stunning quarter with an impressive beat of analysts’ EBITDA estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 6.6% since reporting. It currently trades at $79.46.

Is now the time to buy Spectrum Brands? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Church & Dwight (NYSE:CHD)

Best known for its Arm & Hammer baking soda, Church & Dwight (NYSE:CHD) is a household and personal care products company with a vast portfolio that spans laundry detergent to toothbrushes to hair removal creams.

Church & Dwight reported revenues of $1.47 billion, flat year on year, exceeding analysts’ expectations by 0.7%. Still, it was a mixed quarter as it posted EPS guidance for next quarter missing analysts’ expectations.

As expected, the stock is down 1.9% since the results and currently trades at $95.19.

Read our full analysis of Church & Dwight’s results here.

Colgate-Palmolive (NYSE:CL)

Formed after the 1928 combination between toothpaste maker Colgate and soap maker Palmolive-Peet, Colgate-Palmolive (NYSE:CL) is a consumer products company that focuses on personal, household, and pet products.

Colgate-Palmolive reported revenues of $5.32 billion, up 8.4% year on year. This number beat analysts’ expectations by 1.8%. It was a satisfactory quarter as it also logged a decent beat of analysts’ revenue estimates.

The stock is up 2.6% since reporting and currently trades at $87.62.

Read our full, actionable report on Colgate-Palmolive here, it’s free.

Kimberly-Clark (NASDAQ:KMB)

Originally founded as a Wisconsin paper mill in 1872, Kimberly-Clark (NASDAQ:KMB) is now a household products powerhouse known for personal care and tissue products.

Kimberly-Clark reported revenues of $4.16 billion, up 2.7% year on year. This result topped analysts’ expectations by 1.6%. Overall, it was a strong quarter as it also put up a solid beat of analysts’ EBITDA estimates and a decent beat of analysts’ gross margin estimates.

The stock is down 1.1% since reporting and currently trades at $97.20.

Read our full, actionable report on Kimberly-Clark here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

/CPU%20Chip.jpg)

/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/AI%20software%20engineering%20by%20Tapati%20Rinchumrus%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Hands%20of%20robot%20and%20human%20touching%20on%20big%20data%20network%20connection%20by%20PopTika%20via%20Shutterstock.jpg)