Many investors had already moved on from hydrogen, but Plug Power (PLUG) is back on the radar. The stock is up 96.34% so far in 2026 and has recently pushed to new highs of $3.94 today, helped by traders returning to a name that has stirred strong opinions in the past. The latest move is tied to results, not chatter. In Q1 2026, net revenue rose 22.3% from a year earlier to $163.5 million, beating Wall Street’s estimates by nearly 16%.

That performance matters even more because Plug still has major names behind it. Amazon (AMZN) and Walmart (WMT) remain key customers, using its hydrogen fuel cell systems in logistics and warehouse operations.

Still, the comeback is not without risk. Plug is facing an active securities fraud class action tied to earlier statements about a $1.66 billion Department of Energy loan package, after late‑2025 disclosures sparked fresh doubts about management's communications with investors.

With the stock breaking out, the business showing signs of improvement, and big customers still on board, the key question is whether Plug is finally getting back on track or heading for another sharp swing.

Plug Power’s Q1 Beat Behind the Breakout

Plug Power is based in Latham, New York, and makes green hydrogen systems for producing, storing, and using hydrogen in forklifts, trucks, and industrial settings.

As of May 12, the stock traded at $3.56 and is up 376.5% over the past 52 weeks.

The market now values Plug Power at $4.97 billion, with the stock trading at 6.05 times sales compared with a sector median of 1.96 times and 5.27 times book value versus a sector median of 3.20 times.

Their Q1 2026 report showed revenue of $163.5 million compared with analyst estimates of $141.1 million, which works out to 22.3% growth from a year earlier and a 15.9% beat on sales. This quarter still came with a GAAP loss of $0.18 per share, wider than the expected loss of $0.10, so earnings missed even though revenue was strong.

Their adjusted loss per share narrowed to $0.08 from $0.17 a year ago after backing out non‑cash items to better reflect the day‑to‑day business. This shows a company that is still losing money but is slowly closing the gap as it grows.

It also posted adjusted operating income of -$95.55 million versus a consensus estimate of -$106.3 million, equal to a -58.4% margin and a 10.1% beat that points to tighter cost control than feared.

The operating margin improved to -67% from -134% in the same quarter last year, a clear step in the right direction even though losses remain large. Plug’s free cash flow came in at -$152.4 million compared with -$146 million a year earlier.

Plug’s Strategic Story

Plug Power is trying to tighten up its finances and sharpen its business operations. In late February 2026, the company signed a $132.5 million definitive agreement with Stream Data Centers to sell its interest in the Project Gateway site in New York. The sale covers the land, supporting infrastructure, certain substation assets, and the transfer of specific agreements tied to the site.

Total proceeds could climb to as much as $142 million, depending on when the deal closes and how quickly Plug removes certain assets. The transaction, which is expected to close by this upcoming June 30, and includes a $6 million deposit, is the first leg of a larger $275 million infrastructure optimization plan. That broader effort is aimed at turning non-core assets into cash, freeing up restricted funds, and cutting ongoing maintenance costs.

Leadership is shifting to match that more disciplined approach. On March 2, Plug named Jose Luis Crespo as its new Chief Executive Officer (CEO). He has more than 12 years at the company and previously served as President and Chief Revenue Officer.

Andy Marsh moved into the role of Chairman of the Board. The change puts a long-time commercial leader in charge, with a clearer focus on execution, scaling revenue, and pushing the business closer to profitability.

International growth is also part of the story. In early April 2026, Plug won the front-end engineering design contract to supply a 275 MW GenEco PEM electrolyzer system for Hy2gen Canada’s “Courant” decarbonized ammonium nitrate project in Baie-Comeau, Québec. This is one of Plug’s largest electrolyzer deals so far and a key step in supporting heavy-industry decarbonization in North America.

Taken together, the company shows it can build a more global, contract-backed business that can better support its current valuation.

Plug’s Expectations Still Lag Price Action

Wall Street’s outlook helps explain why Plug Power’s surge is getting so much attention. For the current quarter ending in June 2026, analysts on average expect a loss of -$0.09 per share, better than the -$0.16 loss in the same quarter last year. That points to an expected earnings improvement of about +43.75% year-over-year (YOY), even though the company is still forecast to stay in the red.

Some firms see that progress as enough to stay bullish. H.C. Wainwright more than doubled its price target on Plug’s stock to $7 from $3 and kept a “Buy” rating in place.

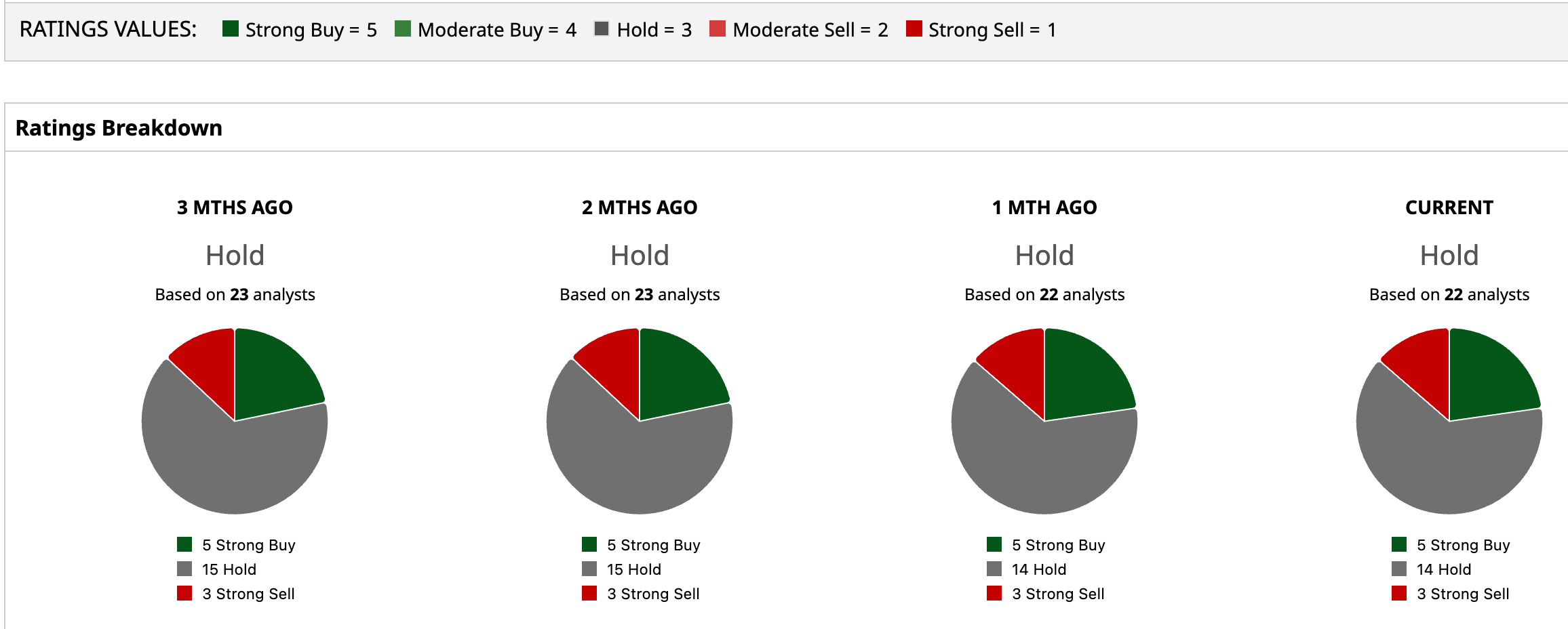

Most analysts are still cautious. The consensus rating sits at “Hold” based on 22 analysts who covered the stock. Their average price target is $2.96, which suggests about -25.6% downside from the recent price, not further upside.

Conclusion

Plug Power now looks less like a fading hydrogen story and more like a company slowly rebuilding its case. The Q1 beat, better margins, and support from Amazon and Walmart all point to a business moving in the right direction. Plug is still likely to be bumpy in the near term, but the tilt from here seems slightly upward as long as execution improves and new contracts keep landing.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.