The enterprise communications market is changing fast. Artifical Intelligence is no longer just an extra feature. It is becoming one of the main components separating winners from the rest. International Data Corporation’s first Worldwide Communications Engagement Platforms 2026 Vendor Assessment brought CPaaS, UCaaS, and CCaaS together in one report, and several companies were named Leaders, including Sinch (SINCH.S.DX), Bandwidth (BAND), and RingCentral (RNG). The enterprise collaboration market alone is worth $73.41 billion in 2026 and is expected to grow to $135.96 billion by 2031, at a 13.12% CAGR.

One company stood out in that IDC report. Twilio (TWLO) was named a Leader in the 2026 IDC MarketScape. IDC research vice president Denise Lund said Twilio stands out for its broad customer engagement platform and ability to combine communications, data, and AI tools.

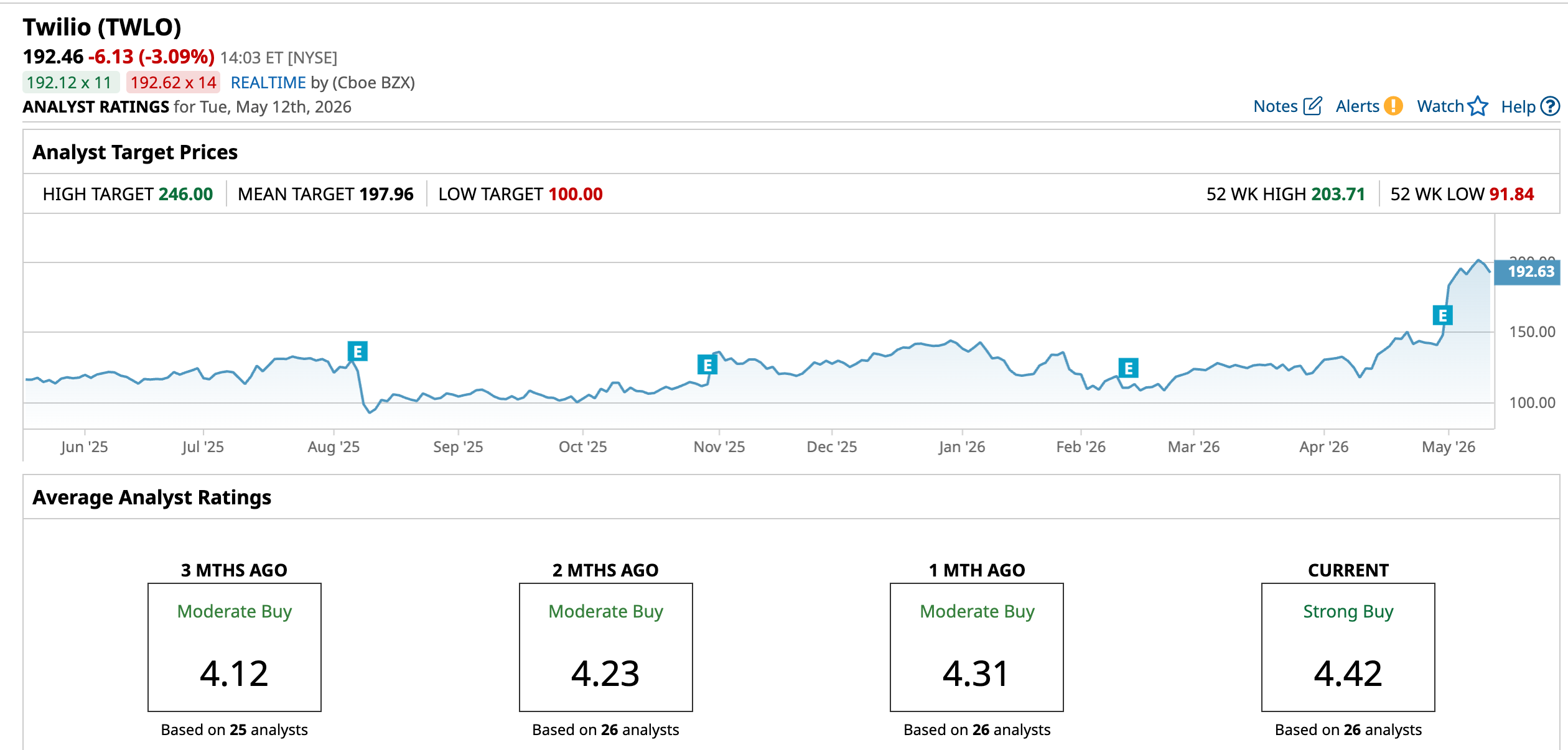

That recognition came just before Twilio posted strong first-quarter results. In Q1 2026, the company reported revenue of $1.41 billion, up 20% year-over-year (YOY), its fastest growth since 2022. Then on May 11, Needham raised its price target on TWLO from $200 to $250, the highest target on Wall Street, after attending Twilio’s customer conference. The firm kept its “Buy” rating and pointed to product innovation and AI leadership as the main reasons.

So, does Twilio’s business still have enough strength to support that bullish view, or has the stock already climbed too far? Let’s find out.

Twilio’s Latest Financial Snapshot

Twilio runs a cloud communications platform that helps businesses connect with customers through text, voice, email, and other digital channels. The stock has had a big run, rising 72.64% over the past year and 34.96% so far in 2026.

That rally has also made the stock look more expensive, with TWLO trading at 72.84 times forward price-to-earnings, compared with 33.06 times for the broader sector.

Its latest quarter helps explain some of that optimism. Revenue came in at $1.41 billion, up 20% from a year ago and ahead of the $1.34 billion analysts were expecting. Adjusted earnings were $1.50 a share, which was 18% above estimates, while adjusted operating income reached $278.9 million for a 19.8% margin.

Operating margin improved to 7.7% from 2% a year earlier, showing better cost control. Free cash flow margin did fall to 9.4% from the previous quarter, but net revenue retention rose to 114% from 108%, which suggests existing customers are spending more.

The Growth Engines Powering Twilio’s Next Phase

Twilio is trying to build its next wave of growth around better customer service tools. One example is its new Flex SDK, which lets businesses add contact center features straight into their own apps instead of relying on a separate system.

Also, it comes with voice support for Agentforce Service, better insights, a more flexible pricing model, and support for sub-accounts. With many companies still reworking their customer service tech, Twilio is clearly trying to make Flex easier to use and more useful as those businesses upgrade.

It is improving the plumbing behind its platform. Twilio says it is now the only CPaaS provider with direct 10DLC and toll-free links across all major carriers in the U.S. and Canada. That includes major U.S. carriers like AT&T (T), T-Mobile (TMUS), and Verizon (VZ), and big Canadian names such as Bell (BCE), Rogers (RCI), and Telus (TU), along with broader RCS availability. For customers, that should mean better message delivery, faster setup, and fewer compliance headaches, which are all important for larger companies delivering high volumes of messages.

Outside North America, Twilio is pushing newer messaging tools. Its partnership with KPN in the Netherlands, powered by Alphabet's Google (GOOGL), brings RCS Business Messaging to major mobile operators there. That gives businesses more than basic SMS, with features like verified sender identity, images, buttons, and other interactive tools.

Wall Street Reassesses Twilio’s Upside Potential

Analysts expect Twilio to earn $0.59 per share in the June quarter and $0.64 in September, compared with $0.42 and $0.56 a year ago. That works out to growth of 40.5% and 14.3%, respectively. For the full year, the consensus is $2.77, down from $4.59 in 2025.

In April, Bank of America jumped from “Underperform” to “Buy” in one move and raised its price target from $110 to $190, saying Twilio could become a core part of how AI-powered voice and messaging services work. Mizuho also lifted its view around the same time.

Jefferies upgraded the stock to “Buy” with a $160 target earlier in April, pointing to Twilio's spot at the top of the CPaaS market, its Voice AI products, new tools rolling out, and better monetization from current customers.

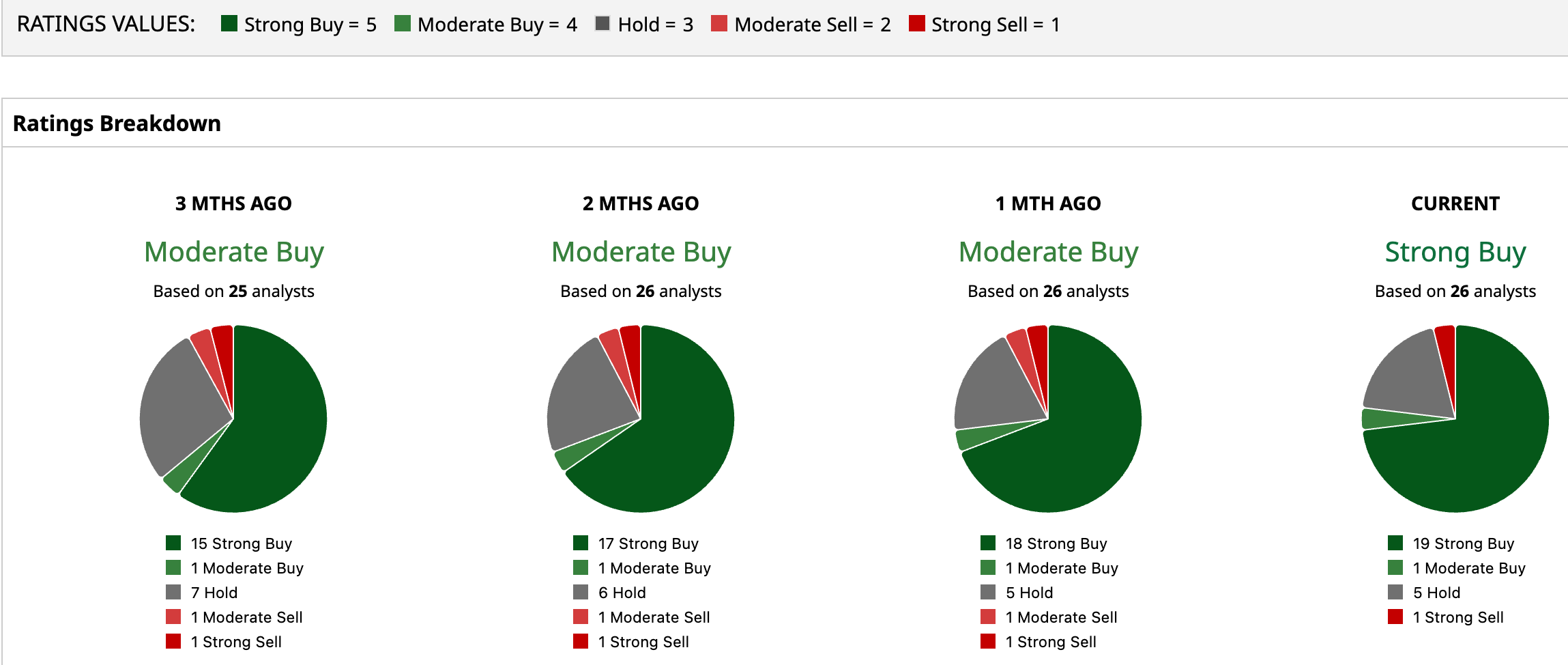

Right now, all 26 analysts covering the stock rate it a consensus “Strong Buy”, with an average target of $197.96, showing a possible 2.9% upside. And with a Street-high target price of $246, TWLO could climb 27.82% from here.

Conclusion

The bull case on Twilio looks credible, but the stock no longer looks cheap. The company is putting up stronger growth, improving margins, and showing enough product momentum in AI, voice, and customer engagement to justify a more constructive view, while Needham’s new $250 Street-high target reinforces that shift in sentiment. Still, a lot of optimism is clearly priced in. My view is that the stock is more likely to keep trending higher if execution stays this strong. But near-term, the move may be less explosive than the recent rally suggests because expectations have risen right along with the share price.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)