/Quantum%20Computing/A%20concept%20image%20of%20a%20green%20and%20yellow%20motherboard_%20Image%20by%20Gorodenkoff%20via%20Shutterstock_.jpg)

Quantum computing stocks have become the ultimate high-beta play in 2026, with massive rallies — fueled by AI and next-gen computing hype — punctuated by stomach-churning selloffs when reality checks hit. Following peers like IonQ (IONQ) and Rigetti Computing (RGTI) on the same quantum wave, Xanadu Quantum Technologies (XNDU) is now stepping into the spotlight with its very first earnings report as a public company. After a headline-grabbing initial public offering (IPO), a more than 280% April surge, and then a brutal 61% single-day crash triggered by a share-registration filing, investors are desperate for any signal.

That signal is expected to arise on May 14, when Xanadu reports first-quarter 2026 results after the closing bell. This isn’t just a financial update. It's the first real insight into whether Xanadu's photonic quantum promise is translating into commercial traction.

What Does Xanadu Actually Do?

Xanadu Quantum is not trying to do quantum computing the same way as everyone else. The company is building photonic quantum systems, and its own investor presentation says that photonic systems can operate at room temperature rather than relying on cryogenics or laser cooling. The firm also says that PennyLane is a key software layer in its broader platform, linking quantum circuits with classical and machine-learning workflows.

That difference matters because the market is not only valuing Xanadu as a hardware company. It is also valuing the possibility that photonics, software, and system sales can become a scalable platform over time.

The Numbers That Could Make or Break Xanadu Quantum

Xanadu doesn’t have a long public track record to lean on. In its last report before the IPO, the company posted a staggering loss of $14.29 per share for full-year 2025. Full-year revenue grew about 188% year-over-year (YOY) to $4.6 million.

For fiscal 2026, analysts currently expect the company to report a narrower loss of around $0.52 per share, with revenue estimates moving higher due to what some analysts describe as “strong machine sales momentum.” The real numbers to watch will be related to any updates on system deliveries, commercial partnerships, and cash runway.

Recent deals with Advanced Micro Devices (AMD) and EV Group signal that Xanadu is pushing hard to industrialize its chips, and the market will want to see whether these collaborations are already converting into orders, or whether they remain PowerPoint promises.

With XNDU stock still recovering from the recent share-registration shock, a weak top-line print or a cautious outlook on machine sales could easily reopen the wounds.

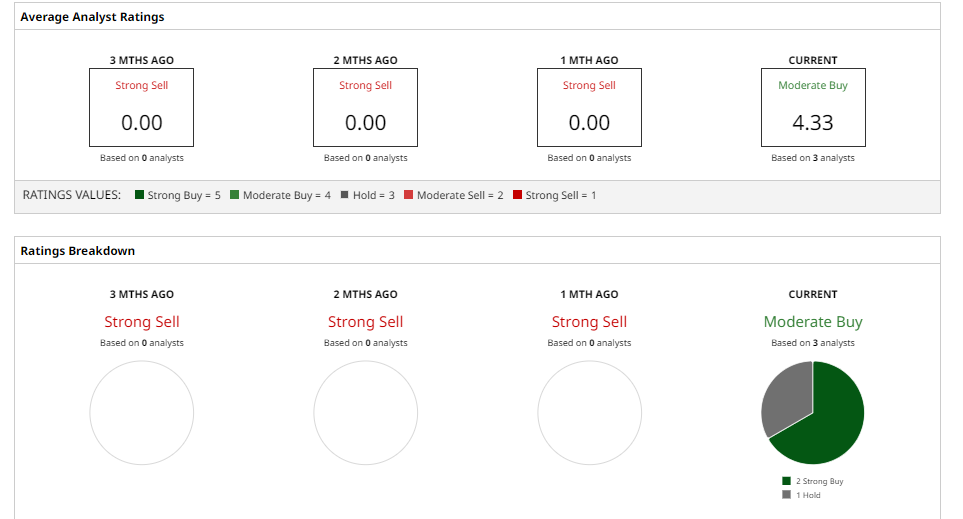

What Does Wall Street Think of XNDU Stock?

The Street is still unusually constructive for a stock that just suffered a brutal reset. Currently, analysts rate XNDU stock as a consensus “Moderate Buy." The mean price target of $44 implies potential upside of roughly 211% on paper.

However, the analyst base behind this rating and price target is still very small, which makes the consensus fragile. Price targets can be helpful as a sentiment gauge, but they are not the same thing as long-term proof that the business model is fully working.

For now, Wall Street appears to be betting that the selloff was an overreaction and that the current price is still far below the value of Xanadu's technology, if commercialization keeps improving.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Quantum%20Computing/A%20concept%20image%20with%20a%20brain%20on%20top%20of%20a%20blue%20circuit%20board_%20Image%20by%20Gorodenkoff%20via%20Shutterstock_.jpg)

/Microsoft%20logo%20on%20building%20by%20franz12%20via%20iStock.jpg)