Headquartered in San Jose, California, BILL Holdings (BILL) is a leading provider of cloud-based software that automates financial operations for small and midsize businesses (SMBs). Founded in 2006, the company offers an end-to-end platform that streamlines accounts payable (AP), accounts receivable (AR), and spend management. By integrating with major accounting software and financial institutions, BILL enables businesses to eliminate paper-based processes, manage cash flow in real-time, and execute digital payments globally.

BILL Stock Rebounds

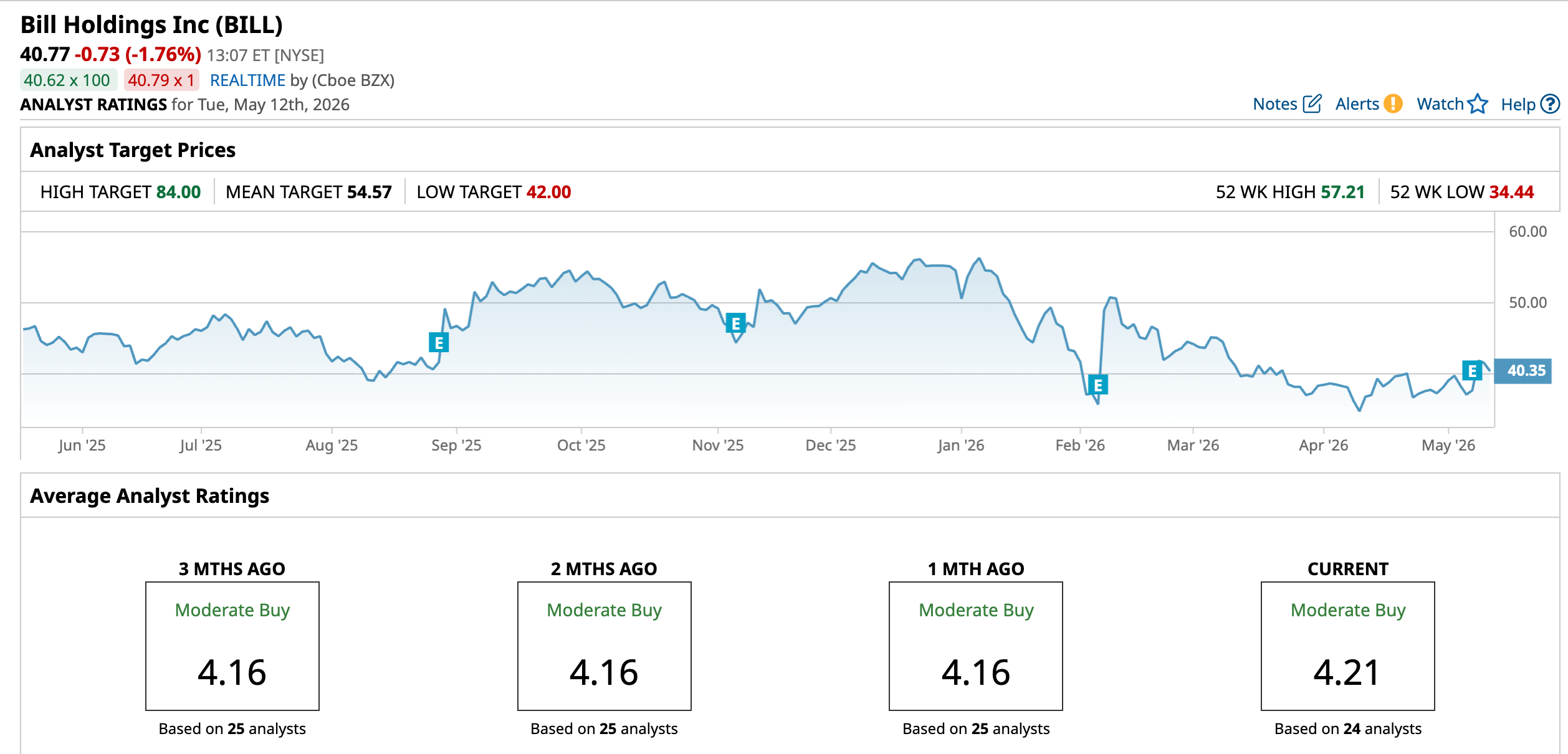

Bill Holdings' stock has faced significant headwinds throughout 2026, losing roughly a quarter of its value as investors rotated out of high-multiple fintech names. However, shares recently rebounded by 2.48% in aftermarket trading following a strong Q3 earnings report, recovering from a 52-week low of $34.44.

Compared with the Russell 1000 iShares ETF (IWB), BILL has significantly underperformed the broader market over the last 12 months. While the Russell 1000 gained 24.68% during the past year, driven by the AI mega-cap rally, BILL’s shares have struggled, falling by double digits in the same period.

BILL Posts Strong Earnings

BILL Holdings reported a landmark third quarter for fiscal 2026 on May 7, achieving GAAP profitability for the first time in its history with a net income of $12.8 million. Total revenue reached $406.6 million, a 13.5% increase year-over-year (YOY), beating analyst estimates.

This growth was fueled by Core Revenue, which climbed 16% to $371.1 million, driven by strong adoption of its integrated platform. Total payment volume (TPV) reached $89 billion, up 12% from the prior year, while transaction fees rose 18% to $296.6 million. The company also saw a 39% surge in joint customers using both its AP and Spend & Expense solutions, reflecting successful multiproduct adoption.

Looking ahead, management raised its fiscal 2026 guidance, projecting total revenue between $1.642 billion and $1.652 billion, reflecting 15-16% growth in core revenue. The company is leaning heavily into its "AI-first" priority, having already deployed AI agents to over 100,000 customers to automate complex human workflows and reduce transaction costs. For the fourth quarter, BILL expects non-GAAP EPS of $0.69 to $0.72, well above the consensus mark.

With $2.17 billion in cash and short-term investments, the company is leveraging its strong balance sheet to fund its massive $1 billion buyback program while continuing to scale its AI-native finance workflows for its expanding upmarket customer base.

Bill Lays Off 30% of Its Staff

In a major strategic shift to bolster profitability, BILL Holdings announced a significant 30% workforce reduction alongside its third-quarter earnings. The San Jose-based fintech expects to incur restructuring charges of $30 million to $60 million, primarily impacting its fourth-quarter fiscal 2026 results. This aggressive cost-cutting move, which sent shares climbing over 8% in extended trading, comes amid intensifying pressure from activist investors Starboard Value and Elliott Investment Management.

The restructuring follows a challenging period where the stock lost nearly 31% of its value in early 2026. By prioritizing lean operations, BILL achieved GAAP profitability this quarter.

While the firm remains a potential acquisition target for private equity giants like Hellman & Friedman, these internal changes aim to stabilize the business independently by the first quarter of fiscal 2027.

Should You Buy BILL?

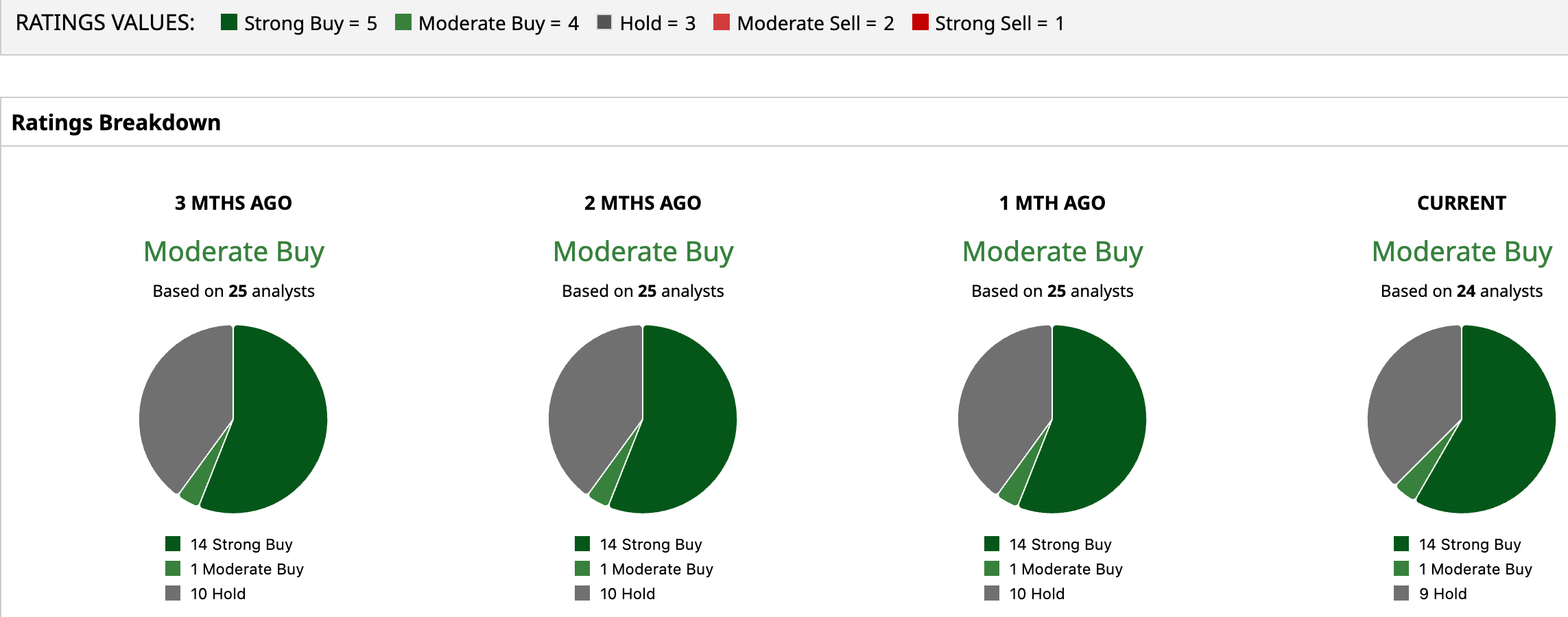

The recent 30% workforce reduction signals a decisive shift toward permanent profitability, addressing activist pressure and stabilizing the bottom line. Currently, BILL holds a consensus "Moderate Buy" rating supported by 14 "Strong Buy" ratings, one “Moderate Buy,” and nine "Holds" out of 24 reports. With a mean price target of $54.57, the stock offers a projected 33.9% upside from current levels.

For investors, the combination of a $1 billion buyback program, newfound GAAP profitability, and potential acquisition interest makes BILL an intriguing value play in the consolidating fintech sector.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)