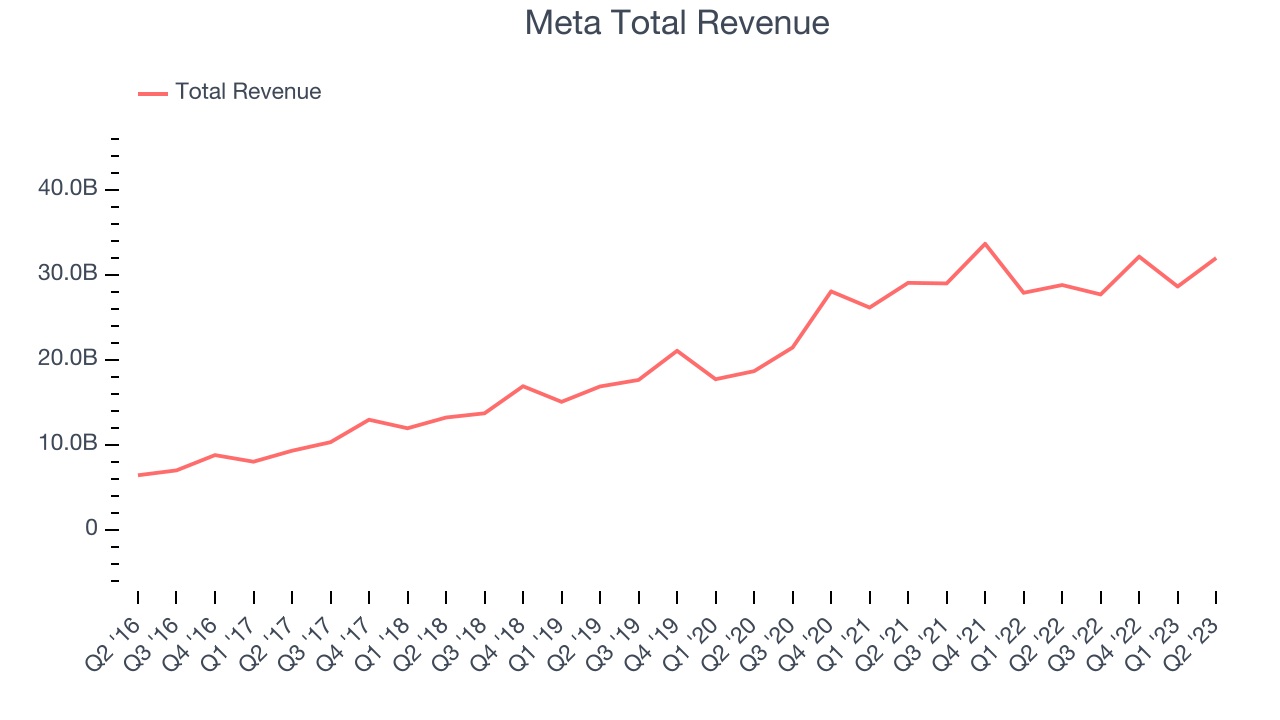

Social network operator Meta Platforms (NASDAQ: META) reported Q2 FY2023 results topping Consensus expectations, with revenue up 11% year on year to $32 billion. On top of that, next quarter's revenue guidance ($33.3 billion at the midpoint) was surprisingly good and 6.89% above what analysts were expecting. Meta made a GAAP profit of $7.79 billion, improving from its profit of $6.69 billion in the same quarter last year.

Is now the time to buy Meta? Find out by accessing our full research report free of charge.

Meta (META) Q2 FY2023 Highlights:

- Revenue: $32 billion vs analyst estimates of $31 billion (3.12% beat)

- EPS: $2.98 vs analyst estimates of $2.91 (2.51% beat)

- Revenue guidance for Q3 2023 is $33.3 billion at the midpoint, above analyst estimates of $31.1 billion

- Free cash flow of $11 billion, up 58.5% from the previous quarter

- Gross Margin (GAAP): 81.4%, in line with the same quarter last year

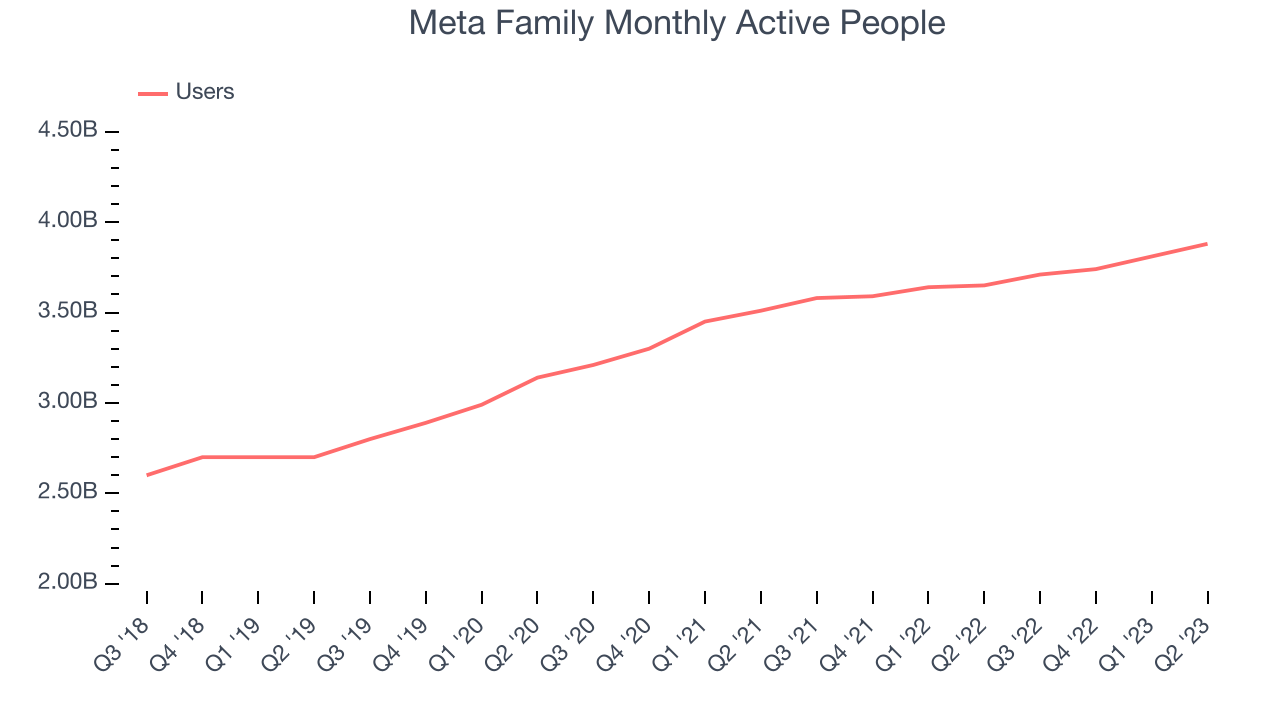

- Family Monthly Active People: 3.88 billion, up 230 million year on year

"We had a good quarter. We continue to see strong engagement across our apps and we have the most exciting roadmap I've seen in a while with Llama 2, Threads, Reels, new AI products in the pipeline, and the launch of Quest 3 this fall," said Mark Zuckerberg, Meta founder and CEO.

Famously founded by Mark Zuckerberg in his Harvard dorm, Meta Platforms (NASDAQ: META) operates a collection of the largest social networks in the world - Facebook, Instagram, WhatsApp, and Messenger, along with its metaverse focused Facebook Reality Labs.

Businesses must meet their customers where they are, which over the past decade has come to mean on social networks. In 2020, users spent over 2.5 hours a day on social networks, a figure that has increased every year since measurement began. As a result, businesses continue to shift their advertising and marketing dollars online.

Sales Growth

Meta's revenue growth over the last three years has been solid, averaging 18.6% annually. This quarter, Meta beat analysts' estimates but reported mediocre 11% year-on-year revenue growth.

Guidance for the next quarter indicates Meta is expecting revenue to grow 20% year on year to $33.3 billion, improving on the 4.47% year-on-year decline it recorded in the same quarter last year. Ahead of the earnings results, analysts covering the company were projecting sales to grow 10.8% over the next 12 months.

In volatile times like these, we look for robust businesses with strong pricing power. Overlooked by most investors, this company is one of the highest-quality software companies in the world, and its software products have been the gold standard in critical industries for decades. The result is an impressive business that's up an incredible 18,000%+ since its IPO. You can find it on our platform for free.

Usage Growth

As a social network, Meta generates revenue growth by increasing its user base and charging advertisers more for the ads each user is shown.

Over the last two years, Meta's monthly active users, a key performance metric for the company, grew 6.07% annually to 3.88 billion. This is average growth for a consumer internet company.

In Q2, Meta added 230 million monthly active users, translating into 6.3% year-on-year growth.

Key Takeaways from Meta's Q2 Results

With a market capitalization of $755 billion, a $53.4 billion cash balance, and positive free cash flow over the last 12 months, we're confident that Meta has the resources needed to pursue a high-growth business strategy.

We were impressed by Meta's revenue guidance for next quarter, which blew past Consensus expectations. It implies nearly 20% year-on-year growth. This is a big relief as just a few quarters ago, the company was barely growing revenue year-on-year. The company also beat free cash flow by a meaningful amount, and Meta also lowered its expected capex spend for the full year, which is an additional tailwind to forward free cash flow. We were also glad that revenue and EPS outperformed Wall Street's expectations. On the other hand, the company increased its full year guidance for expenses. This will likely be forgiven by the market, as investments in AI are being cheered and could lead to long-term advantages. Overall, we think this was still a really good quarter that should please shareholders. The stock is up 6.44% after reporting and currently trades at $318.01 per share.

So should you invest in Meta right now? When making that decision, it's important to consider its valuation, business qualities, and what's happened in the latest quarter. We cover this and more in our full company report, and it's free.

Looking for more investment opportunities? One way to find them is to watch for paradigm shifts, just like how every company in the world is slowly becoming a technology company and facing increasing cybersecurity risks. This company is leading the charge in cyber defense with its cloud-native cybersecurity solutions while generating best-in-class revenue growth and SaaS performance metrics. It should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)