/Block%20Inc_%20Image%20by%20Koshiro%20K%20via%20Shutterstock.jpg)

Fintech firm Block (XYZ) announced sweeping layoffs in February, cutting down more than 4,000 employees of its 10,000-plus strength. The reason given was pretty clear for everyone: artificial intelligence (AI). Jack Dorsey, Block’s CEO (who also happens to be the co-founder of Twitter, now X), had the vision that a smaller team using the company’s AI-based tools would drive in greater efficiency.

Investors rejoiced at this news, leading to a resurgence in the stock from its 52-week lows. After Block reported its Q1 results on May 7, the stock jumped 6.7% the next day, as the company highlighted its reliance on AI to drive solid results, especially robust margin expansion. This gave investors confidence that Block is doing just fine after the layoffs.

About Block Stock

Headquartered in Oakland, California, Block builds technology to expand access to the global economy through its ecosystem of financial tools. Its operations center on Square, which equips sellers with payment processing, point-of-sale systems, and business management software for seamless commerce.

Complementing this, Cash App enables peer-to-peer payments, banking services, and bitcoin trading for individuals, while Afterpay offers buy-now-pay-later (BNPL) solutions. Additional segments, such as TIDAL for music streaming and Bitkey for self-custody bitcoin wallets, further empower creators and users worldwide. Block has a market capitalization of $44.84 billion.

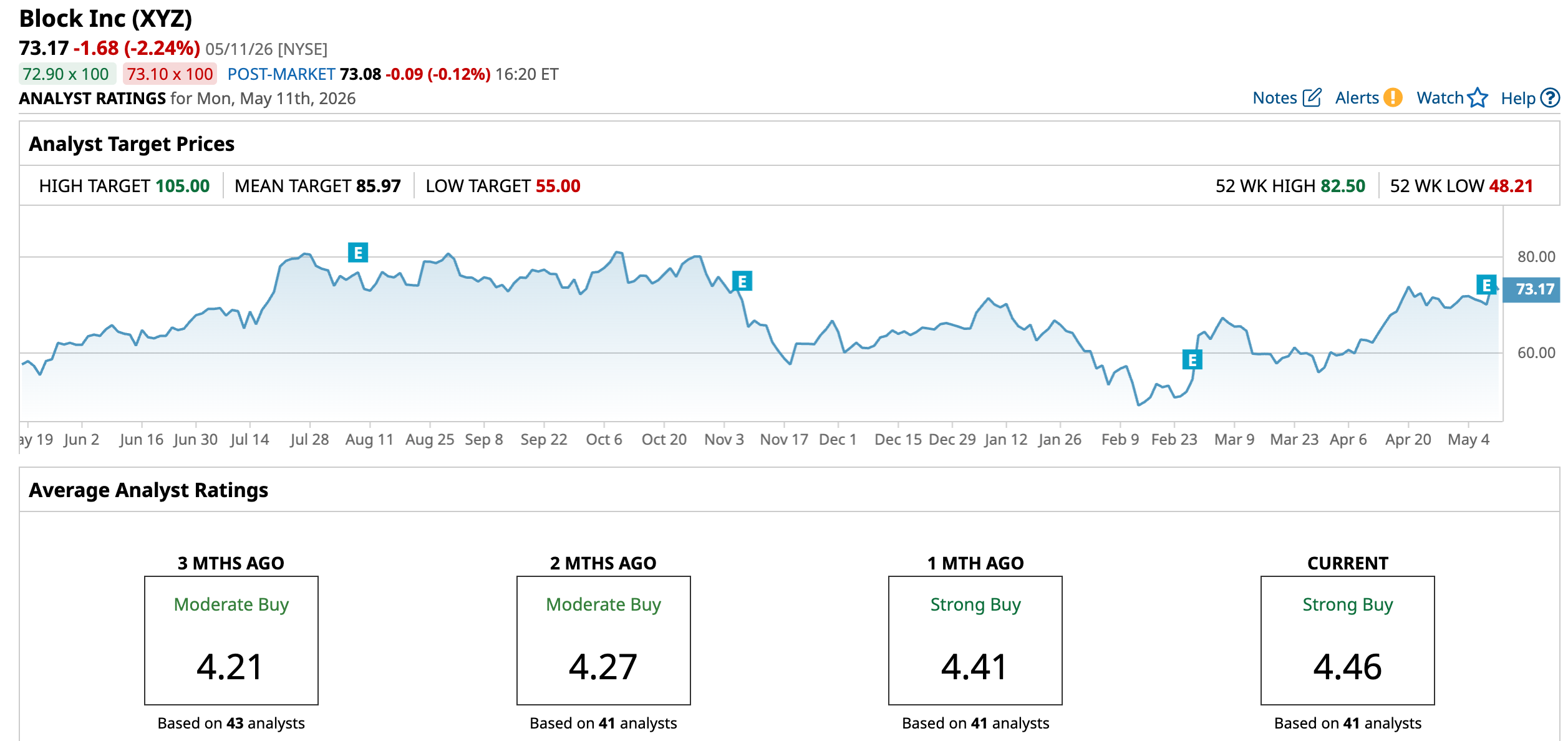

Over the past 52 weeks, Block’s stock has gained 45.29%, while it has been up 12.41% year-to-date (YTD). The job cut announcement, slashed costs, and boosted margins have led to a stock rally. There is also considerable bullish analyst sentiment surrounding the company’s prospects. The stock had reached a 52-week low of $48.21 on Feb. 12, but has rebounded 51.8% from that level.

On a forward-adjusted basis, Block has a price-to-earnings (non-GAAP) ratio of 19.46 times, which is moderately higher than the industry average of 10.61 times.

Block First-Quarter Earnings Highlight Strength

Block’s first-quarter results showcased the company’s increasing reliance on AI operations. With a leaner structure, 100% of its employees now use AI tools. Proactive intelligence tools such as Moneybot and Managerbot are built into the core interfaces of Cash App and Square.

Cash App’s Primary Banking Actives grew 18% year-over-year (YOY) to 9.70 million, with a commerce enablement volume of $55 billion, underscoring 18% YOY expansion. Square’s GPV increased 13% from the prior-year period to $61.21 billion, as its distribution increased across geographies and channels.

Block’s total revenue climbed 5% YOY to $6.06 billion, while its gross profit grew 27% from its year-ago value to $2.91 billion. The Financial Solutions segment posted the largest YOY segmental gross profit growth, at 55% YOY. Block’s adjusted EPS also climbed by a solid 52% annually to $0.85. While the top line missed the Street’s consensus estimate, the EPS figure surpassed expectations.

Moreover, Block raised its 2026 guidance, now expecting gross profit of $12.33 billion, indicating 19% YOY growth. Its adjusted EPS is expected to be $3.85 for the year, reflecting a 62% expansion.

Wall Street analysts have a mixed outlook about Block’s future earnings. Analysts expect Block’s profit to decline 5.5% YOY to $2.22 per diluted share for fiscal 2026, followed by 50% growth to $3.33 in fiscal 2027.

Here’s What Analysts Think About Block, Inc.’s Stock

Recently, after Block’s quarterly results, analyst Daniel Perlin from RBC Capital maintained a bullish “Buy” rating on the stock and kept a $93 price target, signaling unchanged positive sentiments surrounding the company’s prospects. Needham analysts also maintained a “Buy” rating and raised the price target to $95 from $90. Citi analysts also did the same, while raising the price target from $85 to $100.

On the other hand, Piper Sandler analysts kept their “Underweight” rating on Block’s stock, but raised the price target from $51 to $58. While Block has shown notable operating leverage through its restructuring efforts and focus on agentic product development, analysts at the firm remain skeptical of its growth targets and the sustainability of its recent margin growth.

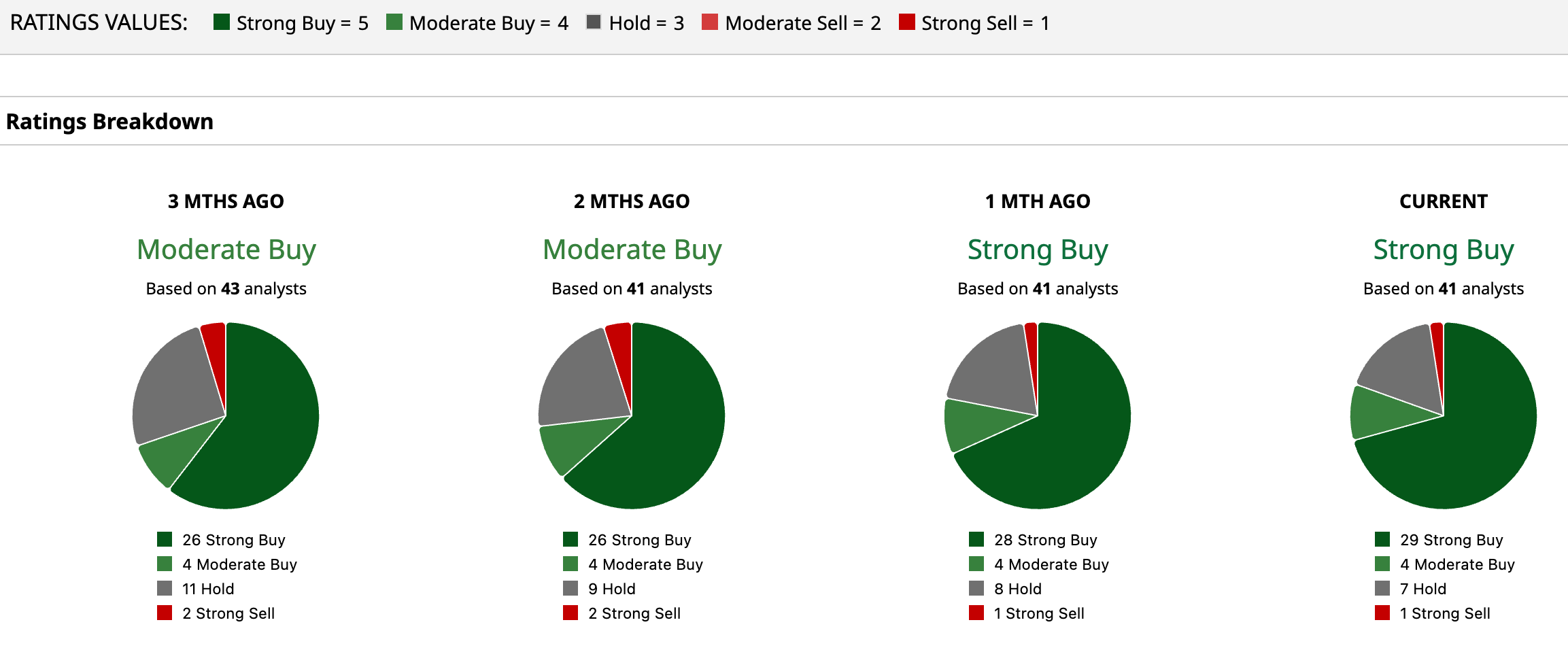

Wall Street analysts have a robustly favorable view of Block’s stock, awarding it with a “Strong Buy” rating overall. Of the 41 analysts rating the stock, a majority of 29 analysts have rated it a “Strong Buy,” four analysts rated it “Moderate Buy,” while seven gave a “Hold” rating, and one suggested “Strong Sell.” The consensus price target of $85.97 represents a 17.5% upside from current levels, while the Street-high price target of $105 indicates a 43.5% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)