/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

The story of Flex (FLEX) is suddenly looking very intriguing amid current AI infrastructure hype. FLEX stock saw a rally of 5% on May 5 and a 40% gain on May 6 following its recent earnings results and impressive fiscal 2027 guidance, as well as plans to spin off its Cloud and Power Infrastructure division. Shares have gained approximately 56% over the last five trading sessions.

This move is far from being done in isolation. AI demand in data centers now calls for investors' focus to shift away from pure chips and GPUs to power, cooling solutions, manufacturing capabilities, and infrastructure deployments, an area in which Flex is emerging.

About Flex Stock

Flex is a leading provider of advanced manufacturing and supply-chain services helping customers design, manufacture, and scale complex products in a variety of industries, such as cloud, power, automotive, industrial, healthcare, and consumer end markets. In the era of artificial intelligence, Flex is gaining importance as data centers face serious issues in power delivery, cooling, and infrastructure deployment speed. Currently, the company’s market capitalization stands at $52.3 billion.

Shares of Flex have seen impressive gains lately. FLEX stock trades near $145, setting new 52-week highs recently. Over the past 12 months, the stock has rallied more than 270%, up significantly from its 52-week low at $38.82. Such a strong performance is well ahead of the market’s general trend.

FLEX stock is now no longer cheap, however. The company trades at a price-to-earnings (P/E) ratio of 44.6 times, 40.2 times forward earnings, and 1.7 times sales. That is a premium valuation for a manufacturer whose profit margin reaches just 3.25%.

Nevertheless, Wall Street clearly sees Flex in a new light, operating as not just a traditional electronics manufacturing company but rather an important AI infrastructure player for data centers.

Flex Beats on Earnings

Flex posted fourth-quarter net sales of $7.5 billion, which grew by 17% year-over-year (YOY). At the same time, annual revenue came in at $27.9 billion, up 8% YOY. In Q4, the firm reported a GAAP operating margin of 5% and adjusted operating margin of 6.7%, marking six-straight quarters with adjusted operating margins above 6%.

Earnings were also good, with GAAP EPS of $0.67 and adjusted EPS of $0.93 reported in Q4. For the full fiscal year, Flex registered $2.33 in GAAP EPS and $3.30 in adjusted EPS. Free cash flow stood at $212 million in Q4 and $1.06 billion for the full-year period.

Guidance proved even more important. For Q1 fiscal 2027, management forecast revenue at $7.35 billion to $7.65 billion, or 14% growth at the midpoint. Adjusted EPS is predicted to be between $0.86 and $0.92 for Q1, reflecting 24% YOY growth at the midpoint.

Fiscal 2027 guidance forecast revenue in the range of $32.3 billion to $33.8 billion, or a YOY gain of 18% at the midpoint. For full-year adjusted EPS, the range is between $4.21 and $4.51, implying 32% YOY growth. These estimates do not include the Cloud and Power Infrastructure spinoff, which may contribute to a higher valuation in the context of AI infrastructure.

What Do Analysts Expect for Flex Stock?

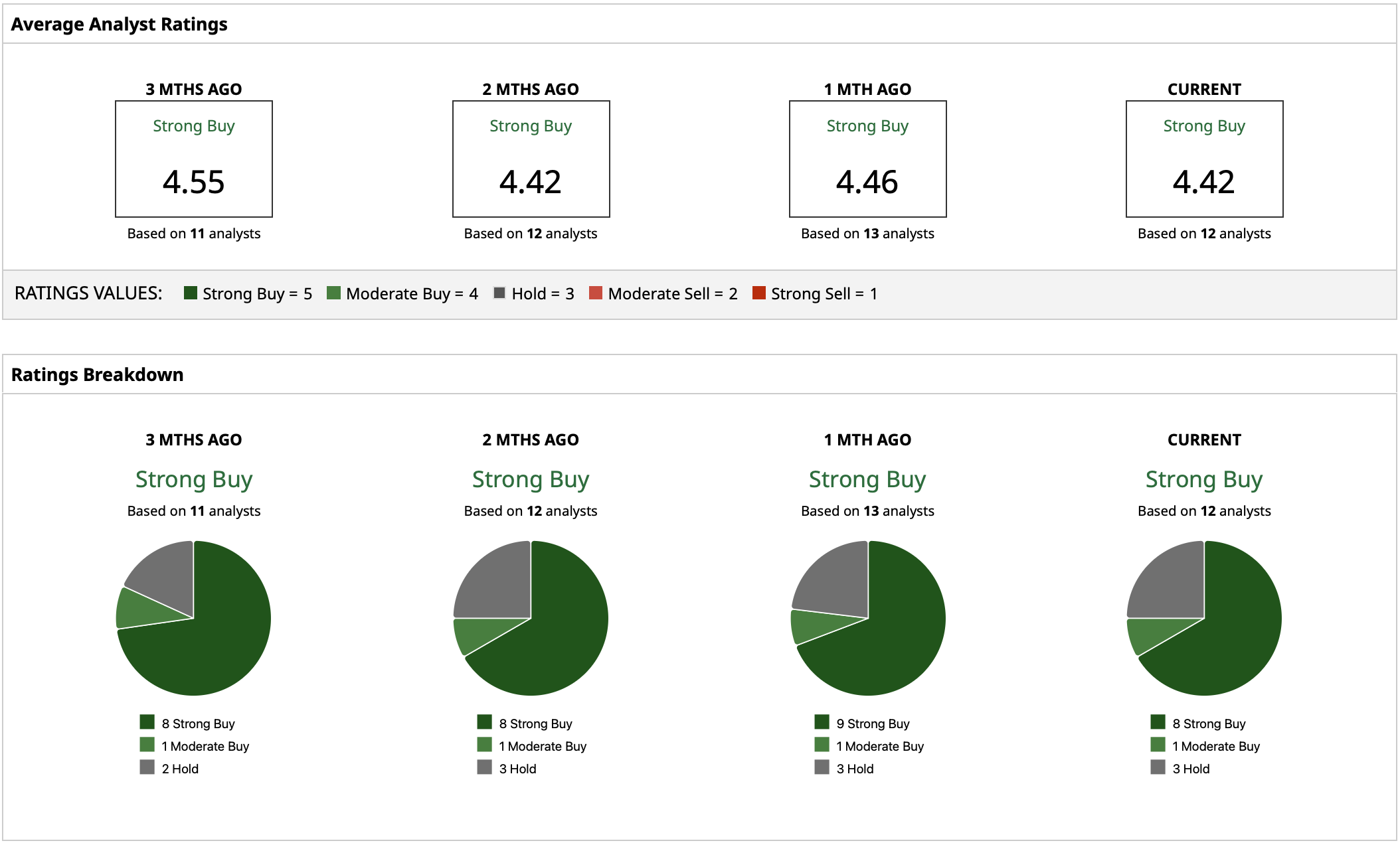

Wall Street analysts assign a consensus “Strong Buy” rating to FLEX stock. That breaks down to eight “Strong Buy” ratings, one “Moderate Buy,” three “Hold” ratings. The average target price stands at $150.11, with the highest and lowest targets at $180 and $85, respectively. Based on the mean price target, FLEX stock has potential upside of 4% from current levels.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)