Entertainment stocks have faced a challenging period in 2026 as investors weighed slowing consumer demand, rising production costs, and uncertainty around streaming profitability. Even some of the biggest media companies have struggled to regain momentum, with many stocks still trading well below their recent highs despite broader market gains.

One company that is now bringing the good news for the whole sector is Disney (DIS). Its stock just soared after the media and entertainment giant posted stronger-than-expected quarterly earnings, fueled by higher guest spending at its cruise lines and resorts alongside improving streaming profits. The company also delivered double-digit operating margins in its direct-to-consumer business for the first time, signaling progress in its long-running streaming turnaround strategy.

While DIS stock remains down roughly 4% year-to-date (YTD), despite a 7.5% surge on May 6, the latest earnings report may have shifted investor sentiment. Strong performance across Disney’s parks, experiences, and cruise operations, increasingly viewed as major profit drivers, has also put several ETFs with large Disney exposure back into focus.

For investors watching the entertainment sector closely, Disney’s latest quarter could mark an important turning point.

Is DIS Still Cheap?

Disney’s valuation story seems interesting now. Its price-to-sales ratio of roughly 1.8 is higher than the media sector median of about 1.3, suggesting the stock is not particularly cheap on a sales basis. However, Disney’s price-to-earnings ratio of around 16 remains below the sector average near 22, which could make the stock appear attractive relative to peers.

The company’s profitability also remains strong, with a net margin of about 12.8%, well above the broader media industry average of roughly 0.8%. In addition, Disney recently posted earnings-per-share growth of approximately 121% year-over-year (YoY).

Earnings and Cruise Boom

Disney’s Q2 beat expectations, and the stock popped on the news. EPS came in at $1.57, beating the $1.50 consensus, on $25.9 billion in revenue.

Investors cheered the cruise and park strength. New ships, Destiny and Adventure, drove a surge in cruise revenue. CFO Hugh Johnston noted that even with 40% more cruise capacity, bookings and occupancy stayed strong.

At parks, higher spending per guest lifted revenue, offsetting a 1% dip in U.S. attendance. Parks' operating income grew as food, drink, and merchandise sales beat forecasts.

Management reaffirmed its outlook: Disney still expects about 12% adjusted EPS growth in 2026 (excl. an extra week), with at least $5.3 billion in segment profit guided for Q3.

These results eased worries. D’Amaro highlighted that park demand is “healthy” even amid higher costs. The company plans to continue aggressive buybacks of about $8 billion for 2026 and investments in new attractions.

Analysts’ full-year EPS forecast is about $6.61, up 11% from FY2025, and Disney has a history of topping estimates.

Disney Expands Global Parks and Cruise Ambitions

Disney is pouring money into growth. It confirmed a new theme park in Abu Dhabi, partnering with Miral, and is building a new cruise ship in Japan. It opened a Frozen-themed land in Paris to stellar guest feedback.

Disney is also unifying its content pipelines: all creative teams now report to a single Disney Entertainment group. Management has talked about treating Disney+ as a “digital centerpiece,” tying movies, parks, cruises, and games together. Essentially, characters that succeed on screen fuel merchandise, park rides, and even cruise experiences.

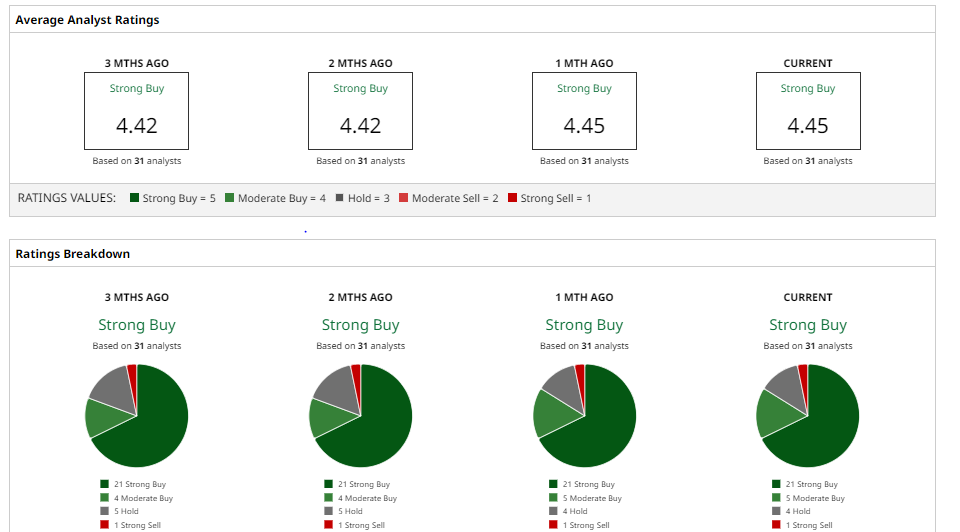

Wall Street Opinion on DIS Stock?

Wall Street’s view is bullish. Morgan Stanley just returned to coverage with an “Overweight” rating and a $135 price target. MS argues Disney’s streaming and parks trends are solid; in fact, the bank says these segments are “poised for a second-half acceleration.”

Goldman Sachs maintains a “Buy” with a $151 target. Goldman expects Q2 will show “continued operating leverage in streaming” boosted by hits like Zootopia 2 and stable parks; it forecasts park revenues up 5%.

Wells Fargo also stays bullish, “Overweight,” and a $148 target. Wells’ Steven Cahall notes Disney needs a fresh narrative; he calls this a “pivotal quarter” as Disney’s new management seeks to reignite growth.

Other firms echo the optimism. Bank of America reaffirmed a “Buy” with a $125 target, citing healthy revenue growth. Guggenheim lowered its target to $115 but still rates it a “Buy,” saying valuation is now more the issue.

Overall, consensus is a "Strong Buy" the average Wall Street price target is about $131.46, implying 21% upside. Disney’s steady beat-and-raise record and improving cash flows suggest analysts believe the company’s new strategy may finally pay off.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)