/Quantum%20Computing/A%20concept%20image%20of%20a%20green%20and%20yellow%20motherboard_%20Image%20by%20Gorodenkoff%20via%20Shutterstock_.jpg)

IonQ (IONQ) is one of the most volatile technology stocks in the market right now. The company is trying to build a leadership position in quantum computing while investors debate whether the industry is still too early to justify massive valuations.

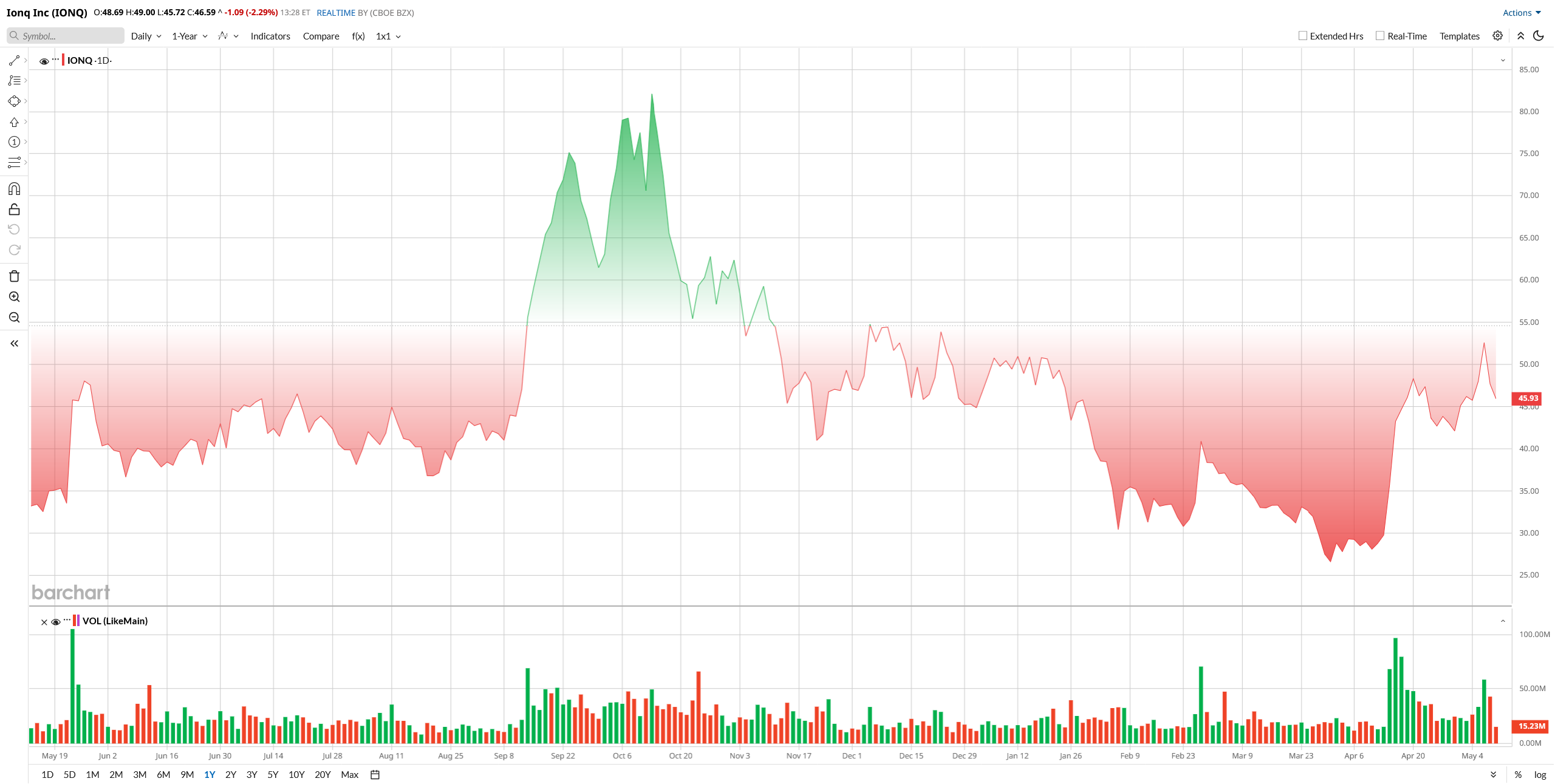

That uncertainty has created huge swings in the stock throughout 2026.

IonQ shares plunged during the first-quarter tech selloff before roaring back in April alongside renewed excitement around quantum computing and artificial intelligence infrastructure. But after reporting what initially looked like a blockbuster earnings quarter, the stock suddenly reversed again, falling more than 9%.

In my opinion, the selloff makes no sense. Revenue exploded higher, guidance increased sharply, and commercial demand appeared stronger than ever. But investors focused on the company’s losses, cash burn, and premium valuation instead.

The bigger picture, however, suggests the long-term growth story may still be intact.

Quantum Computing Remains a Massive Long-Term Opportunity

Quantum computing remains one of the hottest topics in technology, and it not only has great potential but is also highly speculative.

Unlike traditional computers' binary bits, which operate in only two states, quantum processes work with multiple states at once. That may one day lead to quantum computers having the ability to outperform conventional computers in solving very complex problems at much faster speeds.

The technology has the potential to be leveraged across many sectors, including artificial intelligence, cybersecurity, pharmaceuticals, logistics, and advanced manufacturing.

IonQ is aiming to become a full-fledged quantum platform firm. As well as growing its business in trapped-ion quantum computers, the company is establishing new businesses in networking, sensing, and quantum-safe cybersecurity services.

At some point in the future, this broader platform concept could be significant because the quantum market could evolve to include more than just compute hardware.

How Did IONQ Stock Perform?

IonQ’s stock movement this year perfectly shows how emotional the quantum computing trade has become. The shares traded above $70 earlier this year before collapsing below $26 during the broader growth-stock correction. Rising macroeconomic fears, geopolitical tensions, and weakness across speculative technology stocks hit the sector hard.

Quantum computing stocks rallied sharply in April after Nvidia (NVDA) introduced new quantum-AI initiatives that reignited enthusiasm for the industry. IonQ surged more than 60% from its lows and climbed back above both its 50-day and 200-day moving averages, and it is presently up 3% year-to-date (YTD).

Like other quantum names, IONQ's valuation is significantly high, with its price/sales ratio at 99 compared to the sector median of 4, indicating the stock is very expensive relative to peers. However, its price/book ratio of 4.37 is closer to the sector median, suggesting a moderate valuation in this aspect.

For now, the market is valuing IonQ based on where the industry could be years from today rather than where it stands currently.

IonQ's Quarterly Results Actually Showed Strong Momentum

Despite the post-earnings decline, the company’s first-quarter numbers were impressive underneath the surface.

Revenue surged 755% year-over-year (YoY) to $64.7 million, easily beating management’s prior guidance. IonQ also raised its full-year revenue forecast to between $260 million and $270 million, significantly above previous expectations.

Commercial customers generated roughly 60% of total revenue, showing that enterprise demand continues expanding. International markets also contributed heavily to growth.

One of the most important figures in the report was the remaining performance obligations, or RPO.

RPO climbed 554% YoY to approximately $470 million. That metric represents contracted future revenue that has not yet been recognized. In simple terms, it provides visibility into future business demand.

That backlog growth may be one of the strongest indicators that commercial quantum adoption is accelerating faster than many investors expected.

The company is still deeply unprofitable, though.

IonQ posted another sizable adjusted loss while free cash flow remained heavily negative due to aggressive investment spending. Research and development costs surged as management continued prioritizing long-term growth over near-term profitability.

Still, IonQ ended the quarter with more than $2.5 billion in cash and investments, giving the company substantial financial flexibility to continue scaling operations.

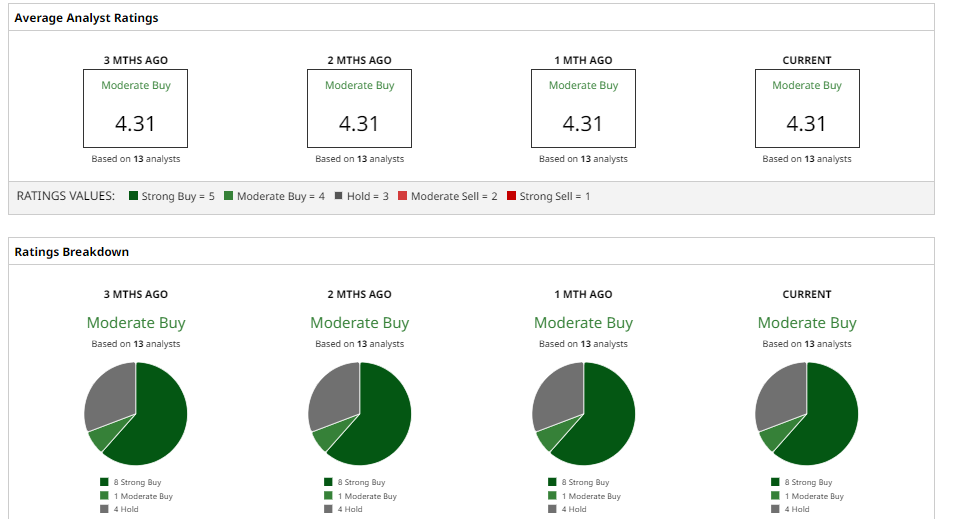

Analysts Still See Meaningful Upside Ahead for IONQ Stock

Wall Street remains divided on valuation, but many analysts continue to believe IonQ has substantial long-term upside potential.

Wedbush analyst Antoine Legault kept an “Outperform” rating on IonQ and raised his price target to $75 from $60. He said IonQ delivered a strong beat-and-raise quarter and pointed to the company’s growing remaining performance obligations (RPO) as a major sign that commercial revenue could keep accelerating in the coming years.

Similarly, Morgan Stanley raised its price target to $48.50 from $47 while maintaining an "Equal Weight" rating. Analyst Joseph Moore said IonQ continues to beat its own quarterly guidance and noted that the company’s overall business trend remains healthy. However, the firm is still cautious about the stock’s valuation.

Likewise, JPMorgan Chase increased its target price to $50 from $42 and kept a "Neutral" rating. Northland Securities started coverage on IonQ in April with an "Outperform" rating and a $55 price target. Needham maintained its "Buy" rating but lowered its target to $65 from $80.

According to Barchart data, the average analyst rating on IONQ stock is a “Moderate Buy.” The average 12-month price target is $66.67 per share, which suggests roughly 40% upside from the current stock price. The highest target on Wall Street is $100, while the lowest target sits at $37.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)