/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)

Super Micro Computer's (SMCI) latest quarterly results finally delivered some relief to investors who have grown used to stock price volatility, margin headwinds, and concerns about execution. While another high-growth quarter came as no surprise, the earnings report clearly showed that infrastructure expansion and profitability are beginning to move up simultaneously in light of extremely high demand for AI infrastructure.

While market participants welcome Super Micro Computer's continued massive revenue growth and high guidance, they remain concerned about cash burn, leverage, and execution risk. Investors need to balance two very different stories with SMCI stock. For one, revenue growth is enormous and guidance indicates that the company is one of the fastest-growing infrastructure firms in the AI industry. At the same time, the company continues to face issues related to its balance sheet and execution.

About Super Micro Computer Stock

Super Micro Computer is an U.S. provider of AI servers, storage, liquid cooling infrastructure, and full-scale data-center solutions. In recent years, the company has been transitioning from a pure server manufacturer into a broad-based provider of AI infrastructure solutions for hyperscalers, enterprises, and cloud customers. With a market capitalization of roughly $20.1 billion, Super Micro continues to be one of the most closely watched AI infrastructure stocks.

Over the past year, SMCI stock has been very volatile. Right now, shares are trading at roughly $35 after rallying significantly. Even with the recent recovery in its share price, Super Micro remains well below its 52-week high of $62.36. However, from the 52-week low of $19.48, the stock has rallied 79%. In the last five days alone, SMCI stock has gained 28%, outperforming the broader market.

From a valuation perspective, SMCI stock looks remarkably cheap compared to AI infrastructure competitors. Currently, the stock trades at 18.2 times forward earnings and 0.94 times sales. The P/E-to-growth (PEG) ratio of 0.65 times shows that the market does not seem very confident in the company's sustainable growth rate. However, at the same time, many other AI-related infrastructure companies trade at considerably higher sales multiples despite much lower growth rates. Still, Super Micro faces concerns about its relatively low margins and ambitious expansion plans.

Super Micro Computer Beat on Earnings

In the third quarter of fiscal 2026, Super Micro posted revenue of $10.2 billion, up significantly from $4.6 billion in the prior-year quarter. Despite a sequential drop in revenue, which was $12.7 billion in Q2 2026, Super Micro showed significant improvement in profitability. That became one of the key highlights of the Q3 earnings report.

Diluted EPS reached $0.72 against $0.17 reported a year earlier, with non-GAAP EPS coming in at $0.84 compared to $0.31 last year. The company's gross margins stood at 9.9%, rising noticeably from the Q2 number of 6.3% and improving slightly compared to 9.6% in Q3 2025. Margins were especially critical in light of concerns about pricing competition in AI servers impacting the company's profitability.

Moreover, management guided for revenue between $11 billion and $12.5 billion in Q4 2026. This guidance suggests that demand for the company's products will remain very strong. For the entire fiscal year, the company projects revenue between $38.9 billion and $40.4 billion, reinforcing the narrative that Super Micro is heavily dependent on robust AI infrastructure buildouts.

It is also worth noting that management highlighted the expansion of the company's DCBBS business as well as construction of new production facilities in Silicon Valley. Management's focus on building out a full suite of data-center infrastructure solutions is becoming increasingly clear as more and more investors seek companies that can take part in the entire cycle of AI infrastructure spend.

However, not everything seemed to be going well. The company burned $6.6 billion in cash while operating in Q3. Additionally, Super Micro reported total debt and convertible notes at $8.8 billion. These numbers might add volatility to the price of SMCI stock due to growing balance-sheet concerns since the explosive AI rally.

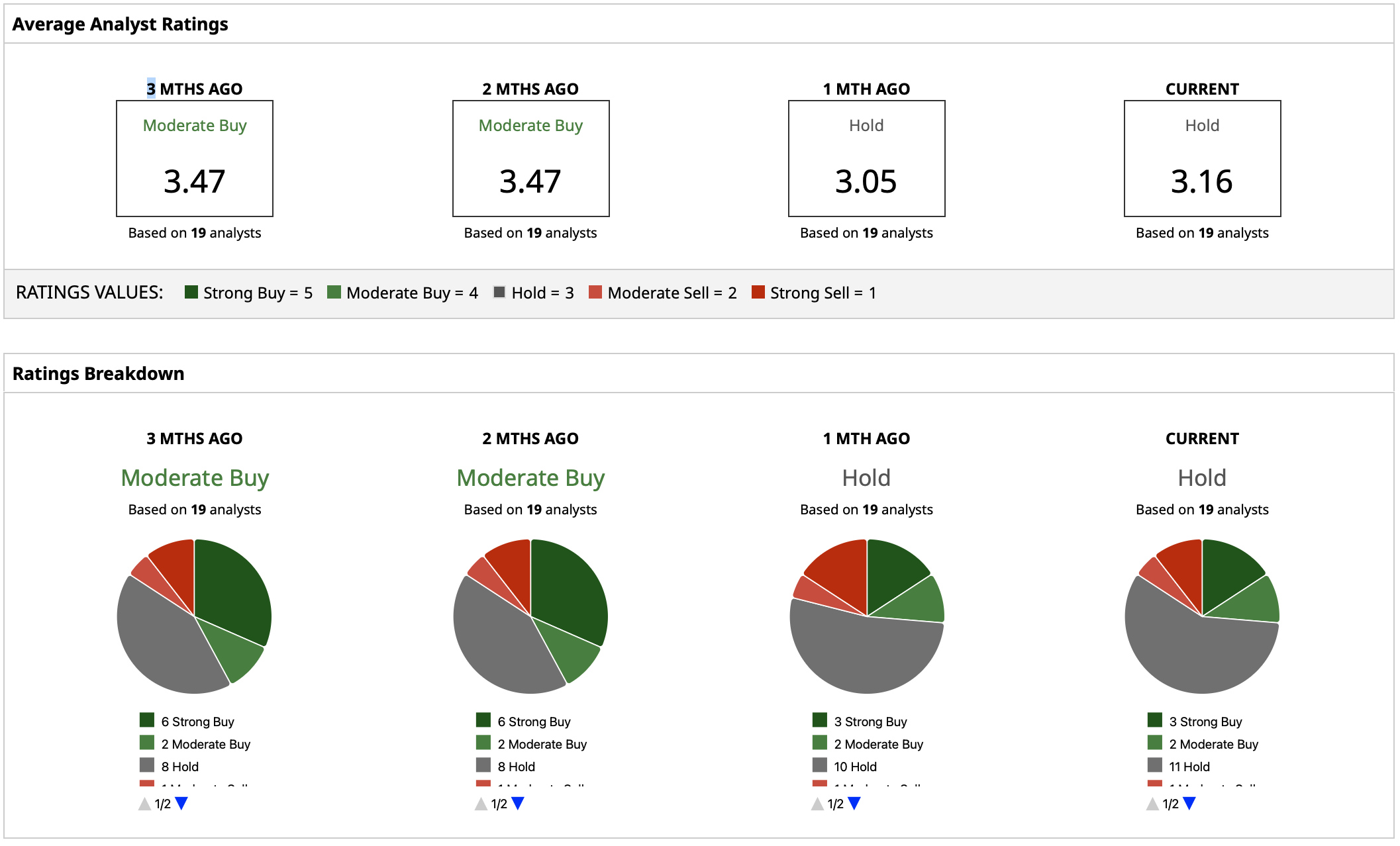

What Do Analysts Expect for SMCI Stock?

Wall Street analysts are divided on SMCI stock despite a positive earnings beat. As of this writing, the stock earns a consensus “Hold” rating. The mean price target of $36.07 is also relatively in line with current price levels, implying minimal potential upside from here. However, based on the high price target of $60, shares of Super Micro Computer could have as much as 71% potential upside from current levels.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)