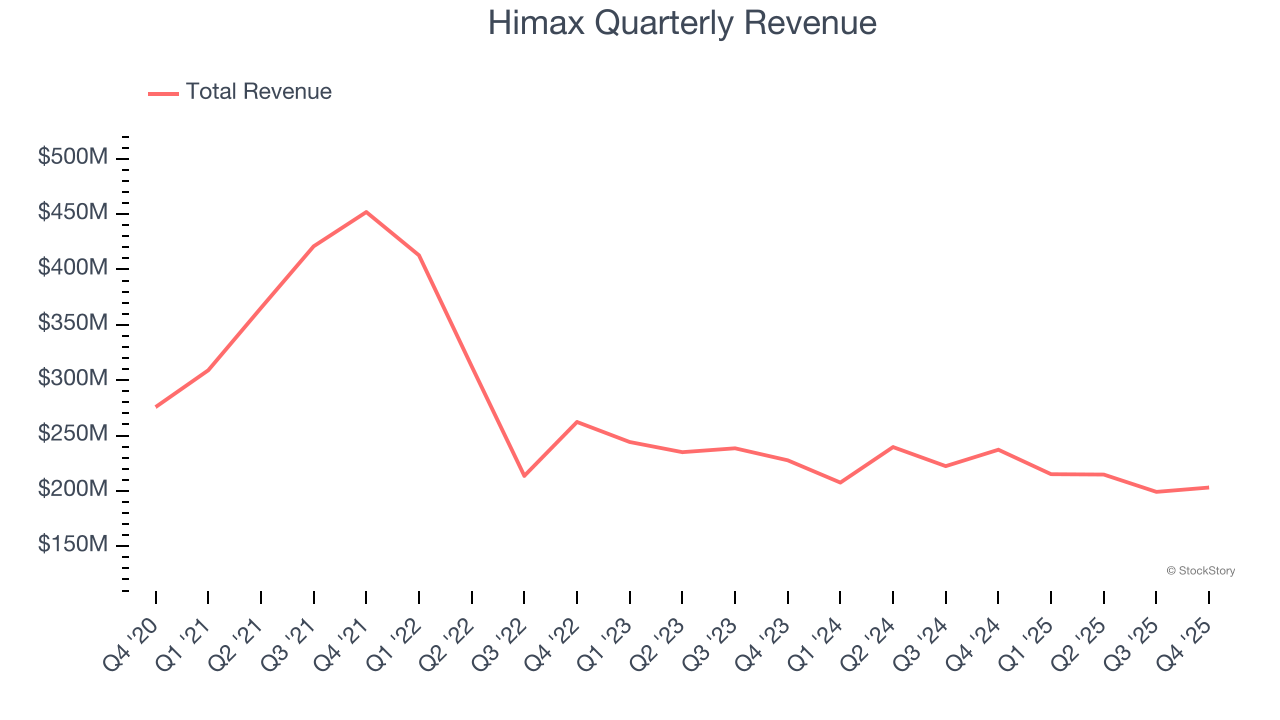

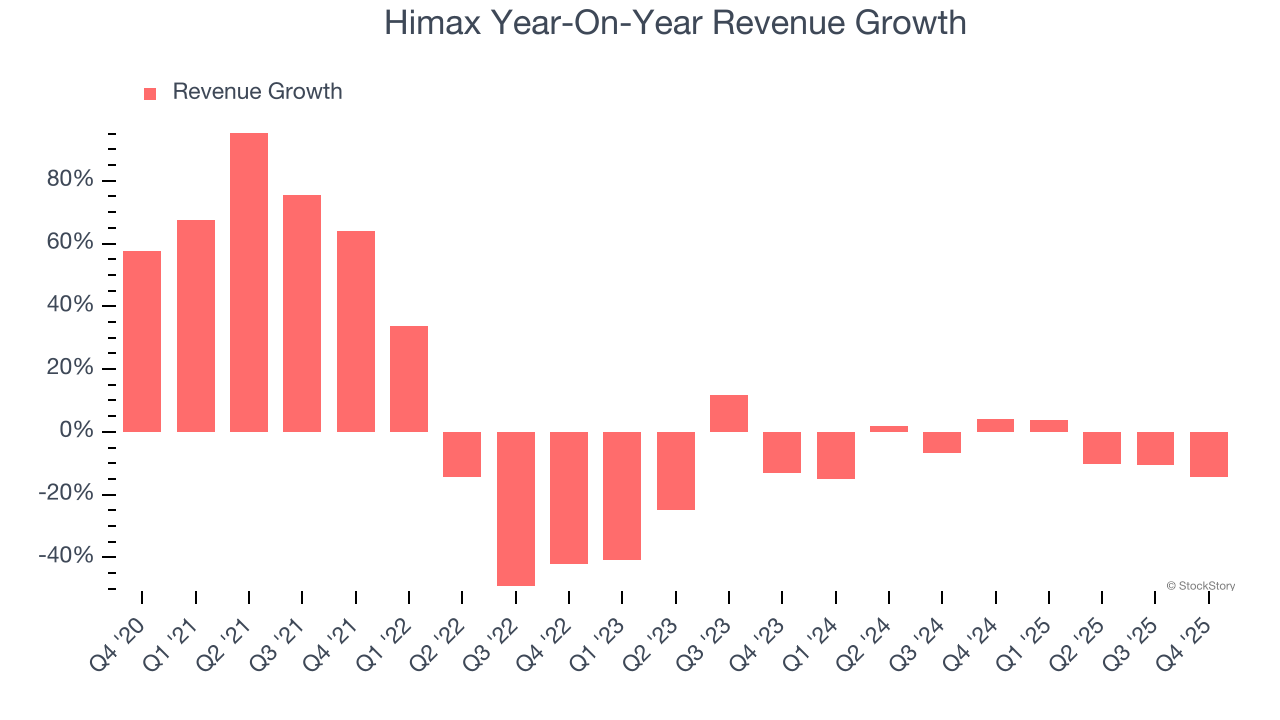

Semiconductor maker Himax Technologies (NASDAQ:HIMX) beat Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 14.4% year on year to $203.1 million. Its GAAP profit of $0.04 per share was in line with analysts’ consensus estimates.

Is now the time to buy Himax? Find out by accessing our full research report, it’s free.

Himax (HIMX) Q4 CY2025 Highlights:

- Revenue: $203.1 million vs analyst estimates of $199.2 million (14.4% year-on-year decline, 2% beat)

- EPS (GAAP): $0.04 vs analyst estimates of $0.04 (in line)

- Adjusted EBITDA: $13.69 million (6.7% margin, 1% year-on-year decline)

- Operating Margin: 3.4%, down from 9.7% in the same quarter last year

- Free Cash Flow Margin: 6.3%, down from 13.6% in the same quarter last year

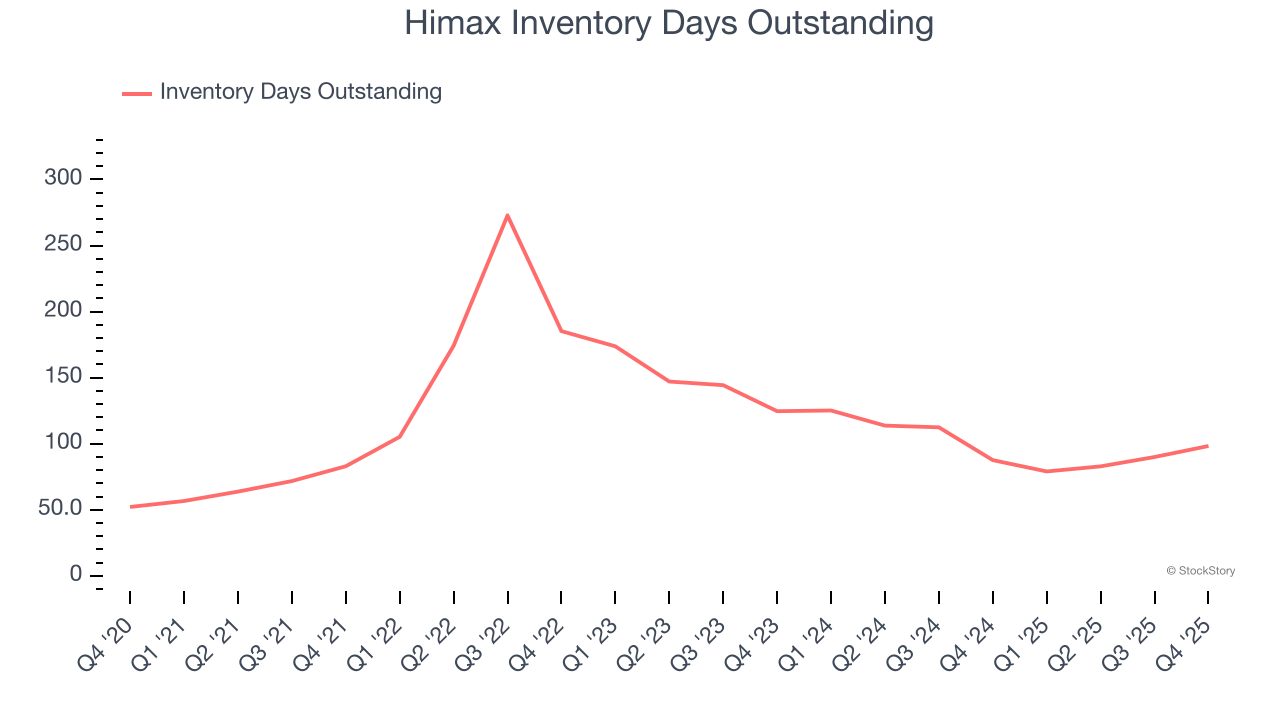

- Inventory Days Outstanding: 98, up from 90 in the previous quarter

- Market Capitalization: $1.44 billion

“Our visibility for the whole year outlook of automotive sector remains limited amid the backdrop of uncertain government policy and consumer sentiment. However, we expect the first quarter to be the trough of the year, with sales rebounding in the second quarter and business momentum continuing to improve into the second half, supported by lean customer inventory levels and new projects for automotive customers scheduled to enter mass production later in the year. Despite lingering economic uncertainty, beyond our mainstream business of display IC solutions, we continue to expand into areas such as ultralow power AI for endpoint devices, Front-lit LCoS microdisplay and waveguide for AR glasses, and WLO for co-packaged optics. All these technologies are seeing exciting upside potential in the next couple of years, driven by the recent breakout of AI,” said Mr. Jordan Wu, President and Chief Executive Officer of Himax.

Company Overview

Taiwan-based Himax Technologies (NASDAQ:HIMX) is a leading manufacturer of display driver chips and timing controllers used in TVs, laptops, and mobile phones.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Himax struggled to consistently generate demand over the last five years as its sales dropped at a 1.3% annual rate. This was below our standards and is a sign of poor business quality. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Himax’s recent performance shows its demand remained suppressed as its revenue has declined by 6.2% annually over the last two years.

This quarter, Himax’s revenue fell by 14.4% year on year to $203.1 million but beat Wall Street’s estimates by 2%. Despite the beat, the drop in sales could mean that the current downcycle is deepening.

Looking ahead, sell-side analysts expect revenue to grow 3.5% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Himax’s DIO came in at 98, which is 21 days below its five-year average. These numbers show that despite the recent increase, there’s no indication of an excessive inventory buildup.

Key Takeaways from Himax’s Q4 Results

It was encouraging to see Himax meet analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its inventory levels materially increased. Zooming out, we think this was a mixed quarter. The stock remained flat at $8.24 immediately following the results.

Big picture, is Himax a buy here and now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)