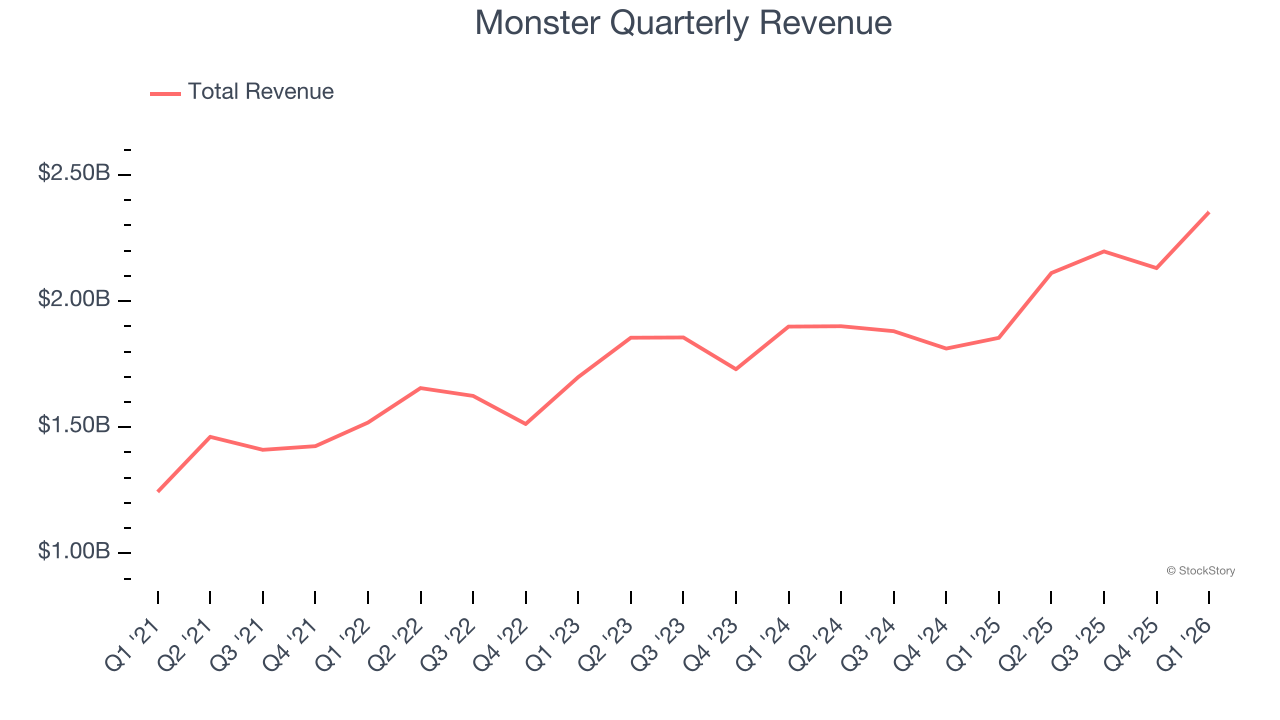

Energy drink company Monster Beverage (NASDAQ:MNST) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 26.9% year on year to $2.35 billion. Its GAAP profit of $0.58 per share was 10.2% above analysts’ consensus estimates.

Is now the time to buy Monster? Find out by accessing our full research report, it’s free.

Monster (MNST) Q1 CY2026 Highlights:

- Revenue: $2.35 billion vs analyst estimates of $2.15 billion (26.9% year-on-year growth, 9.3% beat)

- EPS (GAAP): $0.58 vs analyst estimates of $0.53 (10.2% beat)

- Adjusted Operating Income: $733.5 million vs analyst estimates of $652.1 million (31.2% margin, 12.5% beat)

- Operating Margin: 31%, in line with the same quarter last year

- Market Capitalization: $75.49 billion

Hilton H. Schlosberg, Chief Executive Officer, said, “The global energy drink category continues to demonstrate solid growth, driven by increased consumer demand. We delivered a strong start to the year, with net sales increasing 26.9 percent, operating income increasing 28.1 percent and net income per diluted share increasing 27.6 percent for the 2026 first quarter. Net sales crossed the $2.0 billion threshold for the first time in the Company’s history for a fiscal first quarter.

Company Overview

Founded in 2002 as a natural soda and juice company, Monster Beverage (NASDAQ:MNST) is a pioneer of the energy drink category, and its Monster Energy brand targets a young, active demographic.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $8.79 billion in revenue over the past 12 months, Monster is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions.

As you can see below, Monster’s 10.6% annualized revenue growth over the last three years was decent. This shows its offerings generated slightly more demand than the average consumer staples company, a helpful starting point for our analysis.

This quarter, Monster reported robust year-on-year revenue growth of 26.9%, and its $2.35 billion of revenue topped Wall Street estimates by 9.3%.

Looking ahead, sell-side analysts expect revenue to grow 6.8% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is above the sector average and suggests the market sees some success for its newer products.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

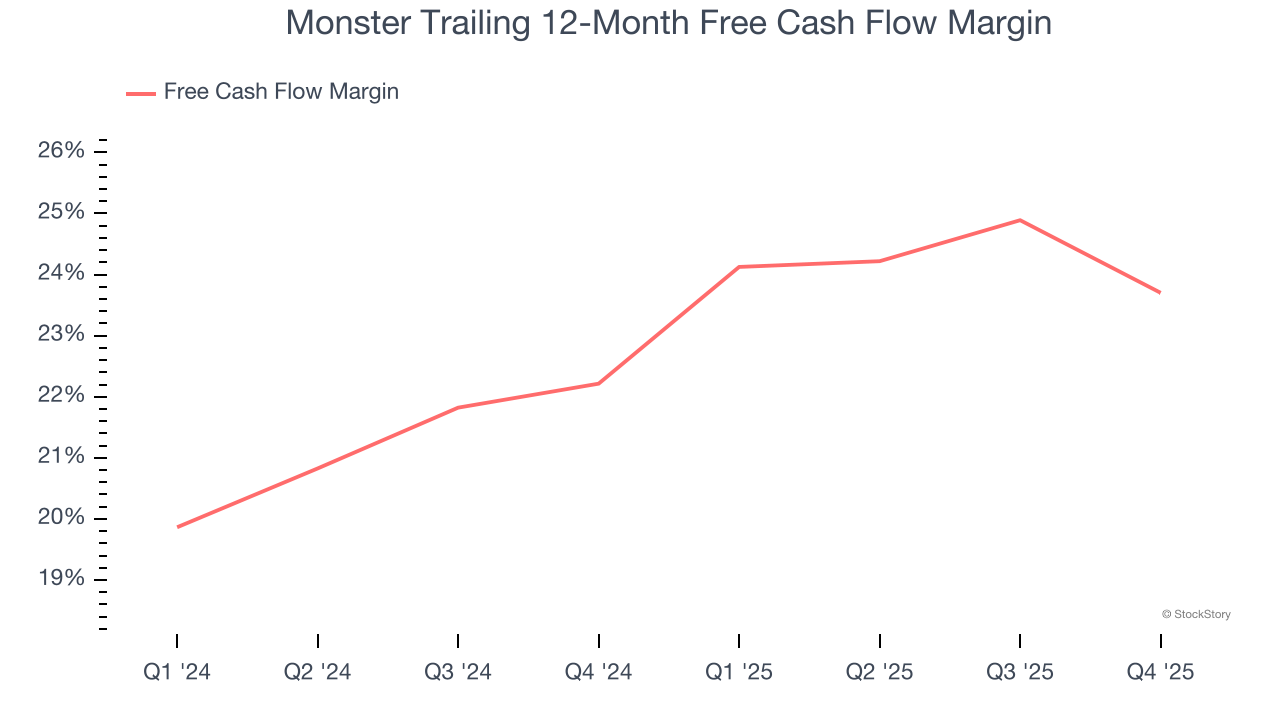

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Monster has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging 23.6% over the last two years.

Key Takeaways from Monster’s Q1 Results

We were impressed by how significantly Monster blew past analysts’ revenue expectations this quarter. We were also happy its adjusted operating income outperformed Wall Street’s estimates. On the other hand, its gross margin slightly missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 9.5% to $83.23 immediately after reporting.

Indeed, Monster had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

/Apple%20Inc%20logo%20on%20Apple%20store-by%20PhillDanze%20via%20iStock.jpg)

/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

/The%20Shopify%20logo%20on%20a%20smartphone%20screen%20by%20IB%20Photography%20%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)