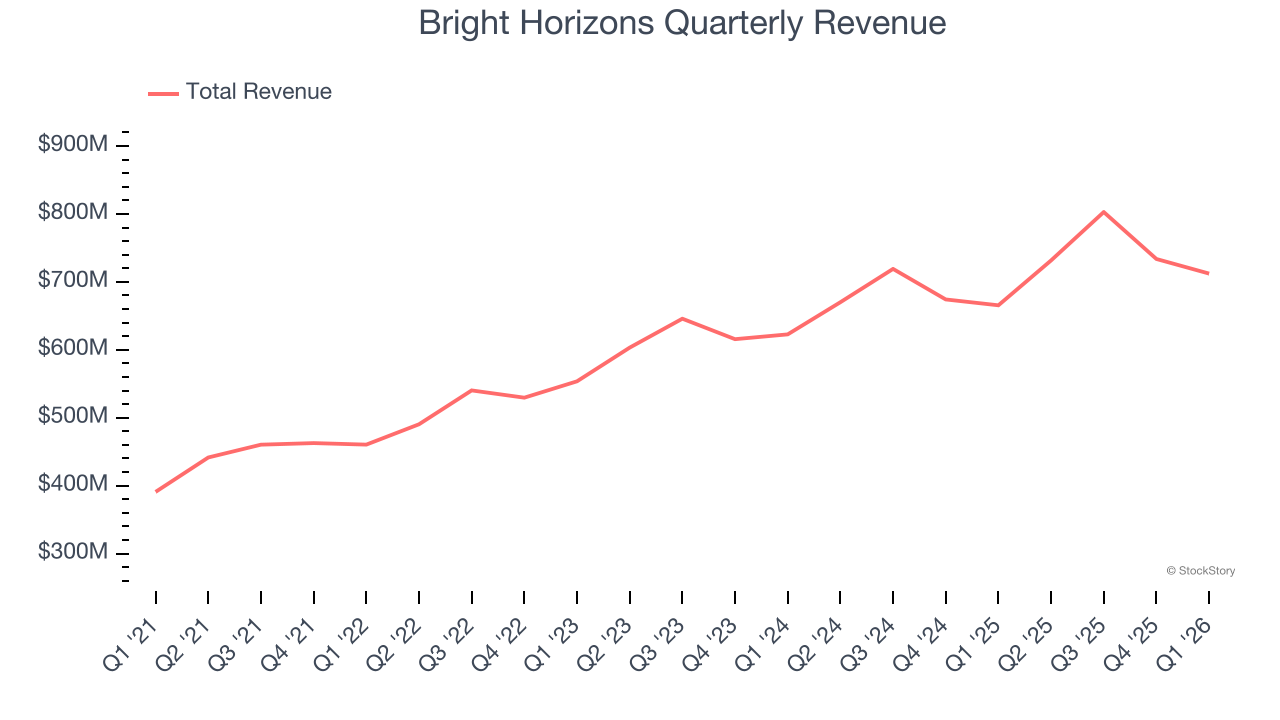

Child care and education company Bright Horizons (NYSE:BFAM) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 7% year on year to $712.2 million. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $3.1 billion at the midpoint. Its non-GAAP profit of $0.82 per share was 2.9% above analysts’ consensus estimates.

Is now the time to buy Bright Horizons? Find out by accessing our full research report, it’s free.

Bright Horizons (BFAM) Q1 CY2026 Highlights:

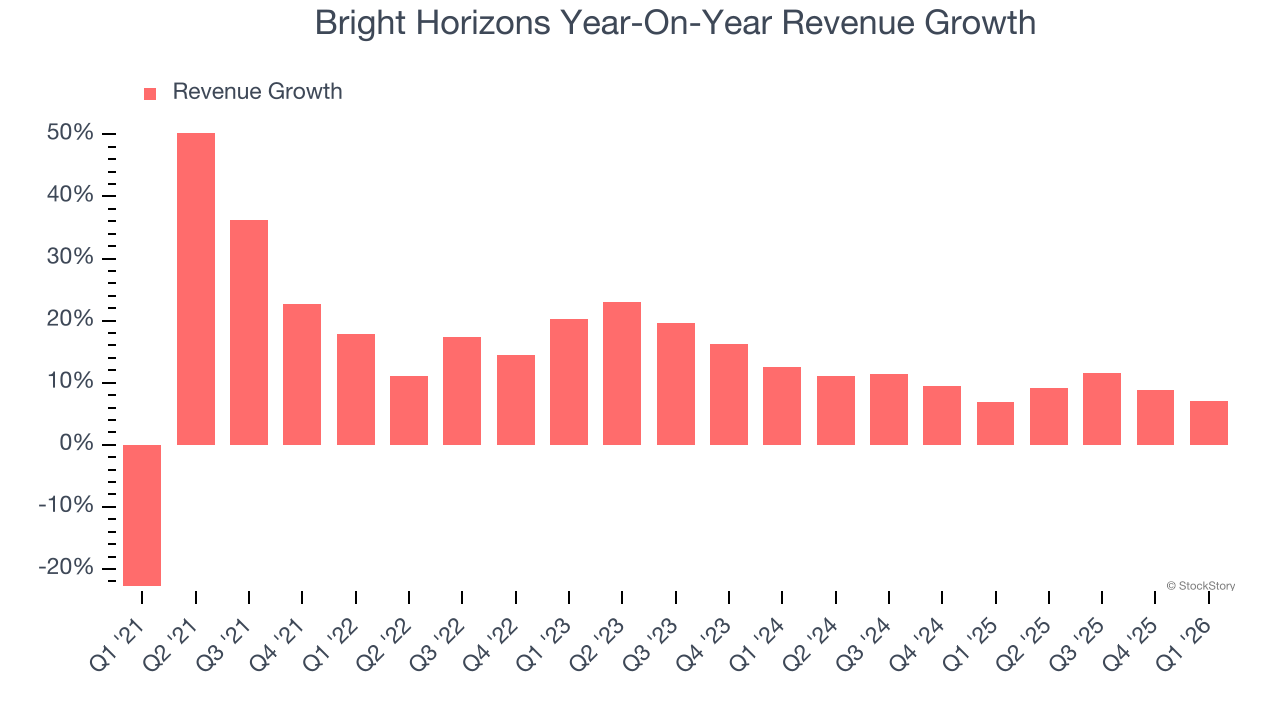

- Revenue: $712.2 million vs analyst estimates of $712.2 million (7% year-on-year growth, in line)

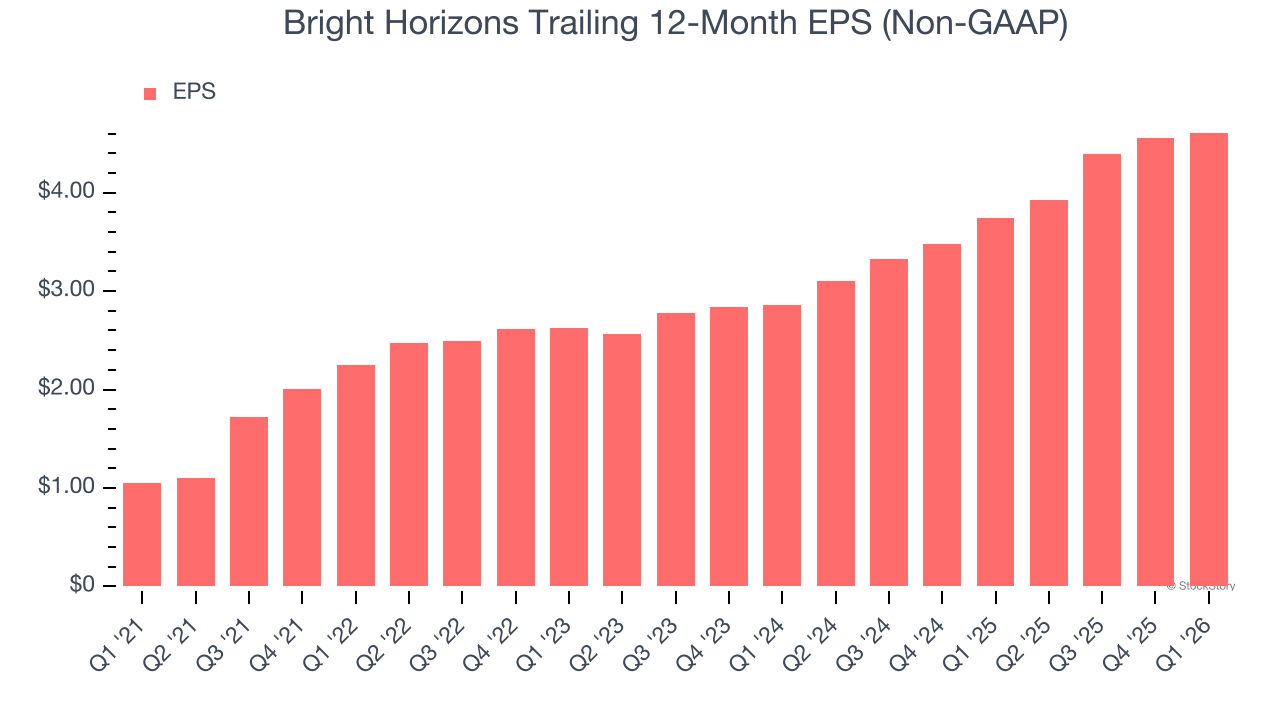

- Adjusted EPS: $0.82 vs analyst estimates of $0.80 (2.9% beat)

- Adjusted EBITDA: $95.61 million vs analyst estimates of $96.04 million (13.4% margin, in line)

- The company reconfirmed its revenue guidance for the full year of $3.1 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $5 at the midpoint

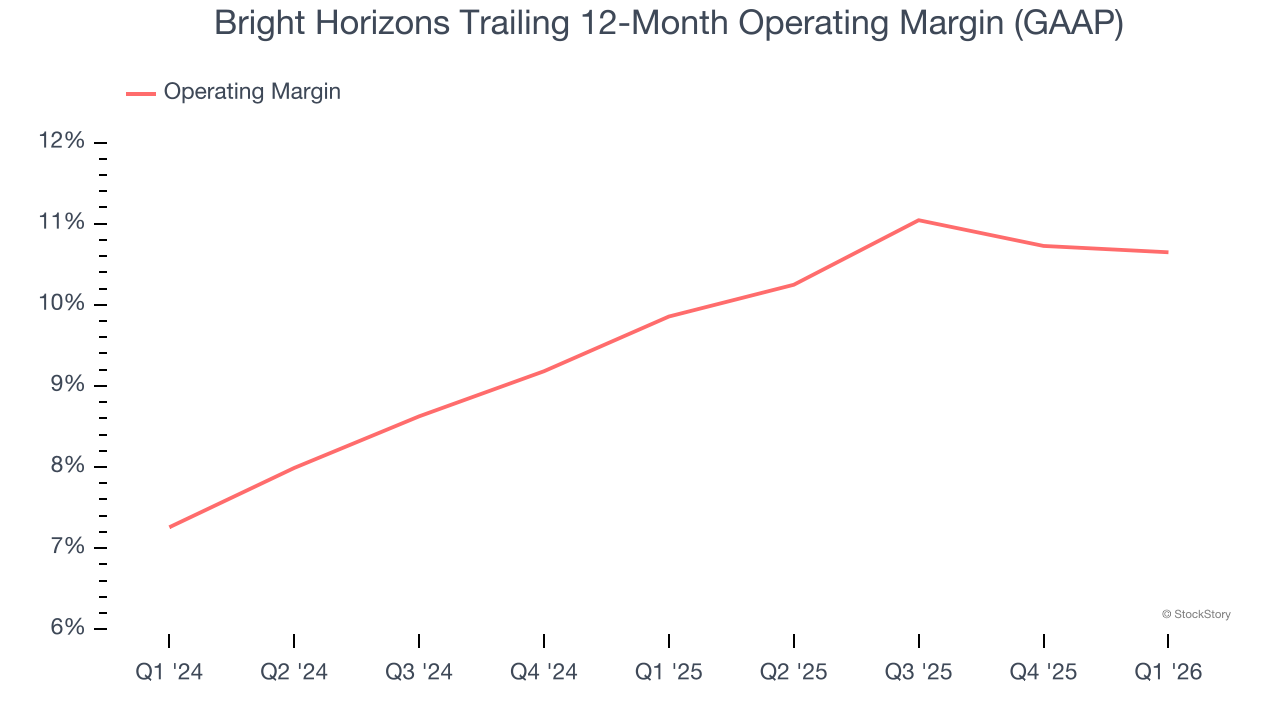

- Operating Margin: 9.1%, in line with the same quarter last year

- Free Cash Flow Margin: 12.3%, up from 10.7% in the same quarter last year

- Market Capitalization: $4.27 billion

Company Overview

Founded in 1986, Bright Horizons (NYSE:BFAM) is a global provider of child care, early education, and workforce support solutions.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Bright Horizons grew its sales at a 16.3% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Bright Horizons’s recent performance shows its demand has slowed as its annualized revenue growth of 9.5% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Bright Horizons grew its revenue by 7% year on year, and its $712.2 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5.6% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Bright Horizons’s operating margin has more or less stayed the same over the last 12 months , and we generally like to see margin increases due to economies of scale and cost efficiency over time.

This quarter, Bright Horizons generated an operating margin profit margin of 9.1%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Bright Horizons’s EPS grew at 34.4% compounded annual growth rate over the last five years, higher than its 16.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q1, Bright Horizons reported adjusted EPS of $0.82, up from $0.77 in the same quarter last year. This print beat analysts’ estimates by 2.9%. Over the next 12 months, Wall Street expects Bright Horizons’s full-year EPS of $4.61 to grow 12.3%.

Key Takeaways from Bright Horizons’s Q1 Results

Revenue was in line and EPS beat. The company's full-year revenue guidance was also in line. Zooming out, we think this was a quarter without many surprises, good or bad. The stock remained flat at $81.68 immediately after reporting.

Is Bright Horizons an attractive investment opportunity right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

/Western%20Digital%20Corp_%20logo%20on%20sign-by%20360b%20via%20Shutterstock.jpg)

/PayPal%20Holdings%20Inc%20sign%20on%20building-%20by%20Sundry%20Photography%20via%20Shutterstock.jpg)

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)