Unity Software (U), the company that powers the world's leading platform for creating and operating interactive, real-time 3D content, has had a rough ride through 2026, and the market has been anything but kind to it. Weak financial guidance and a bruising macroeconomic environment have ganged up on the stock, sending it down a steep 37.54% year-to-date (YTD).

And investors are losing sleep over the growing threat from artificial intelligence (AI) tools like Alphabet's (GOOG) (GOOGL) Google "Project Genie," which lets users conjure interactive 3D worlds straight from text or images, cutting traditional game engines like Unity completely out of the picture and putting a serious dent in the company's competitive edge.

All eyes now sit on Unity's Q1 fiscal year 2026 financial results, which the company is scheduled to drop before the market opens on Thursday, May 7. With just a couple of days to go before the release, analysts at Wedbush Securities have come out swinging and reaffirmed their “Outperform” rating on U stock.

Wedbush sees more meat on the bone even after Unity laid out preliminary Q1 guidance back on March 26, believing the company may have sandbagged the numbers and left some room to surprise on the upside. Wedbush carries a $30 price target on the stock. The question now is whether the rest of us should follow Wedbush's lead and take the plunge on this one.

About Unity Stock

Headquartered in San Francisco, California, Unity Software runs a real-time 3D development platform that gives creators everything they need to build, run, and monetize interactive content across devices.

The company commands a market cap of roughly $12.1 billion and stretches its toolset across design, AI-driven development, live operations, user acquisition, and advertising, serving everyone from gaming studios to enterprise players, government bodies, and media companies worldwide through scalable software and services.

The stock has put up a solid 28.5% gain over the past 52 weeks. However, growing investor anxiety over AI advancements stirred up real fears about disruption to Unity's grip on the game engine market, which yanked the stock lower YTD. But the stock found its footing again and clawed back 21.27% over just the last month.

On the valuation front, U stock currently trades at 27.04 times forward adjusted earnings and 5.71 times sales, numbers that admittedly raise an eyebrow when stacked against peers at first glance but actually come in below Unity's own five-year average multiples, which changes the story quite a bit.

The gap hands long term investors a reasonably comfortable entry point, one where they are not walking in at the very top of the mountain.

Unity Surpasses Q4 Earnings

On Feb. 11, Unity announced its Q4 fiscal year 2025 financial results which cleared the bar on both the top and bottom line. Revenue grew 10.1% year-over-year (YOY) to $503.1 million, topping analyst estimates of $492.1 million, and adjusted EPS climbed 20% from the year-ago value to $0.24, beating the analyst expectation of $0.21.

Create Solutions pulled in $165 million, up 8% YOY, with subscription growth doing the heavy lifting and proving that developers are sticking around. Grow Solutions had an even better quarter at $338 million, up 11% YOY, with Unity Vector growing at a mid-teen sequential quarterly clip and accounting for 56% of total Grow revenue all by itself.

Profitability kept pace too. Adjusted EBITDA came in at $124.9 million, 17.7% better than a year ago. Moreover, the company wrapped up the year with $2.1 billion in cash on Dec. 31, 2025, a solid upgrade from the $1.5 billion it was sitting on twelve months prior.

Then on March 26, Unity raised the bar further by reporting preliminary Q1 fiscal year 2026 revenue and adjusted EBITDA both above its own guidance. The company now expects Q1 revenue of $505 million to $508 million against prior guidance of $480 million to $490 million.

Plus, it anticipates adjusted EBITDA of $130 million to $135 million against prior guidance of $105 million to $110 million, which works out to YOY growth of 58%.

Also, Unity announced it will sunset the ironSource Ads Network effective April 30 and has brought in a financial advisor to work through the divestiture of its Supersonic game publishing business. Once both moves wrap up, Unity expects the combination to drive faster revenue growth, higher adjusted EBITDA, and wider adjusted EBITDA margins.

On the earnings outlook front, analysts are penciling in Q1 EPS of $0.03, a 115.8% YOY improvement. They see full year fiscal year 2026 bottom line growing 160% to $0.13 and then stepping up another 123.1% to $0.29 in fiscal year 2027.

What Do Analysts Expect for Unity Stock?

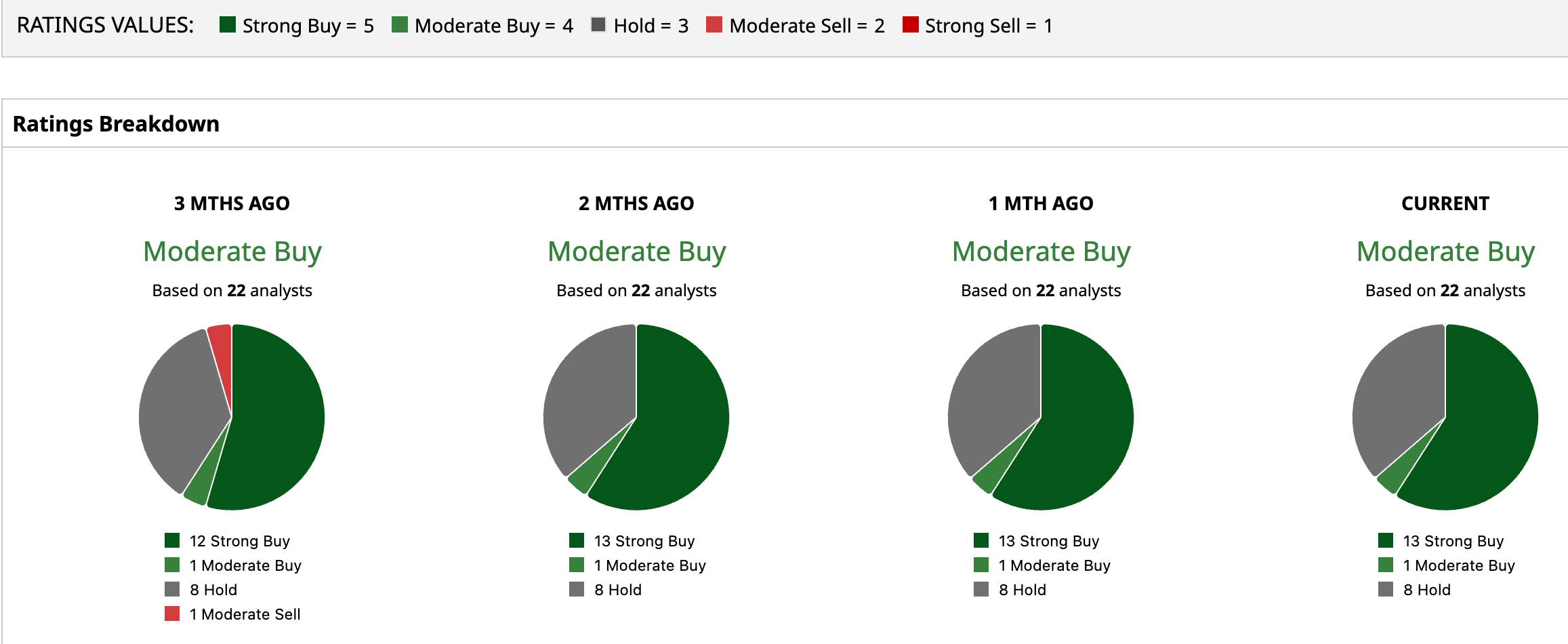

Despite the volatile backdrop, broader Wall Street has assigned the stock with an overall "Moderate Buy" rating. Among the 22 analysts covering U stock, 13 have gone all in with a "Strong Buy," one sits at "Moderate Buy," and eight are content to wait it out at "Hold."

The average price target of $32.67 points to potential upside of 18.6%. Meanwhile, the Street-High target of $48 suggests the stock could run as much as 74.2% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)