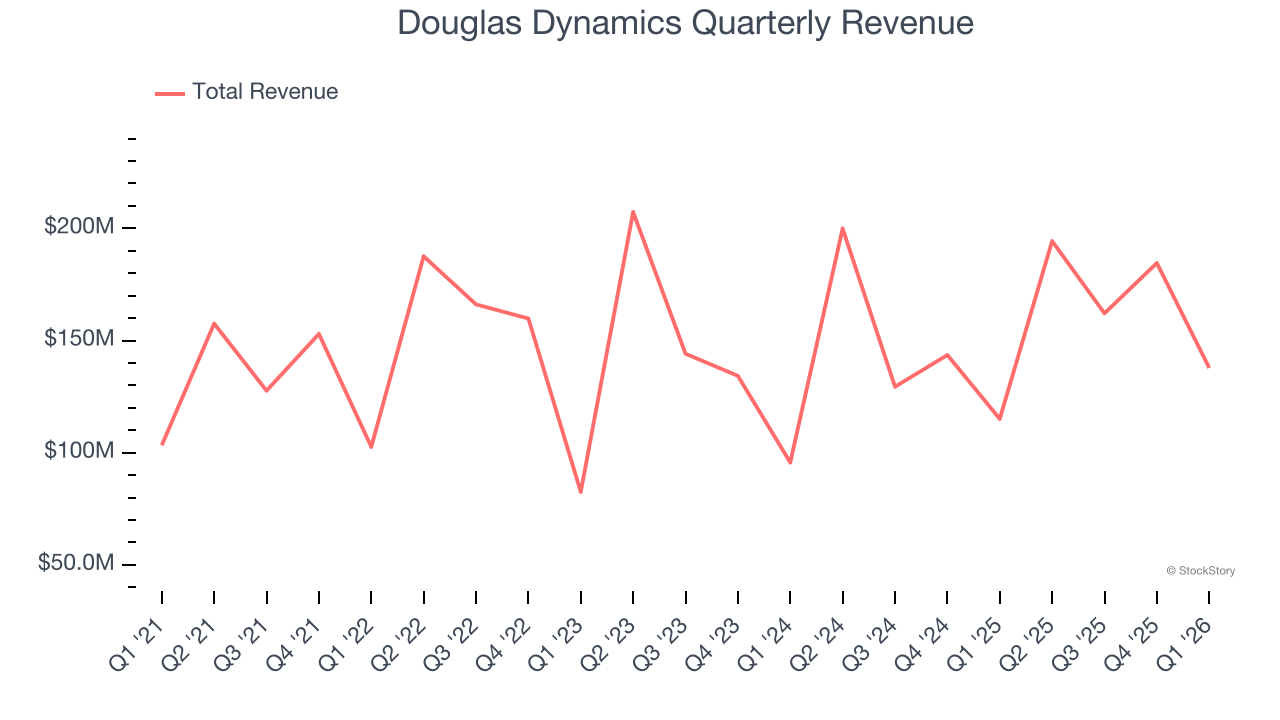

Snow and ice equipment company Douglas Dynamics (NYSE:PLOW) announced better-than-expected revenue in Q1 CY2026, with sales up 19.8% year on year to $137.8 million. The company’s full-year revenue guidance of $772.5 million at the midpoint came in 5.6% above analysts’ estimates. Its non-GAAP profit of $0.36 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Douglas Dynamics? Find out by accessing our full research report, it’s free.

Douglas Dynamics (PLOW) Q1 CY2026 Highlights:

- Revenue: $137.8 million vs analyst estimates of $133.3 million (19.8% year-on-year growth, 3.4% beat)

- Adjusted EPS: $0.36 vs analyst estimates of $0.13 (significant beat)

- Adjusted EBITDA: $16.81 million vs analyst estimates of $10.4 million (12.2% margin, 61.6% beat)

- The company lifted its revenue guidance for the full year to $772.5 million at the midpoint from $735 million, a 5.1% increase

- Management raised its full-year Adjusted EPS guidance to $2.80 at the midpoint, a 9.8% increase

- EBITDA guidance for the full year is $117.5 million at the midpoint, above analyst estimates of $108.3 million

- Operating Margin: 7.2%, up from 2.8% in the same quarter last year

- Free Cash Flow was -$4.16 million compared to -$3.50 million in the same quarter last year

- Market Capitalization: $1.03 billion

Mark Van Genderen, President & CEO, stated, “The strength of our first-quarter results reflects increased snowfall driven demand, disciplined execution, and continued progress against our strategic priorities. Our performance is particularly positive in light of year over year comparison to the robust first quarter of 2025. These results establish a strong foundation for the year, and we remain focused on pursuing our strategic objectives amid an evolving macroeconomic backdrop. I want to thank our teams for their ongoing dedication as we work to address the heightened demand across many areas of our business.”

Company Overview

Once manufacturing snowplows designed for the iconic jeep vehicle precursor, Douglas Dynamics (NYSE:PLOW) offers snow and ice equipment for the roads and sidewalks.

Revenue Growth

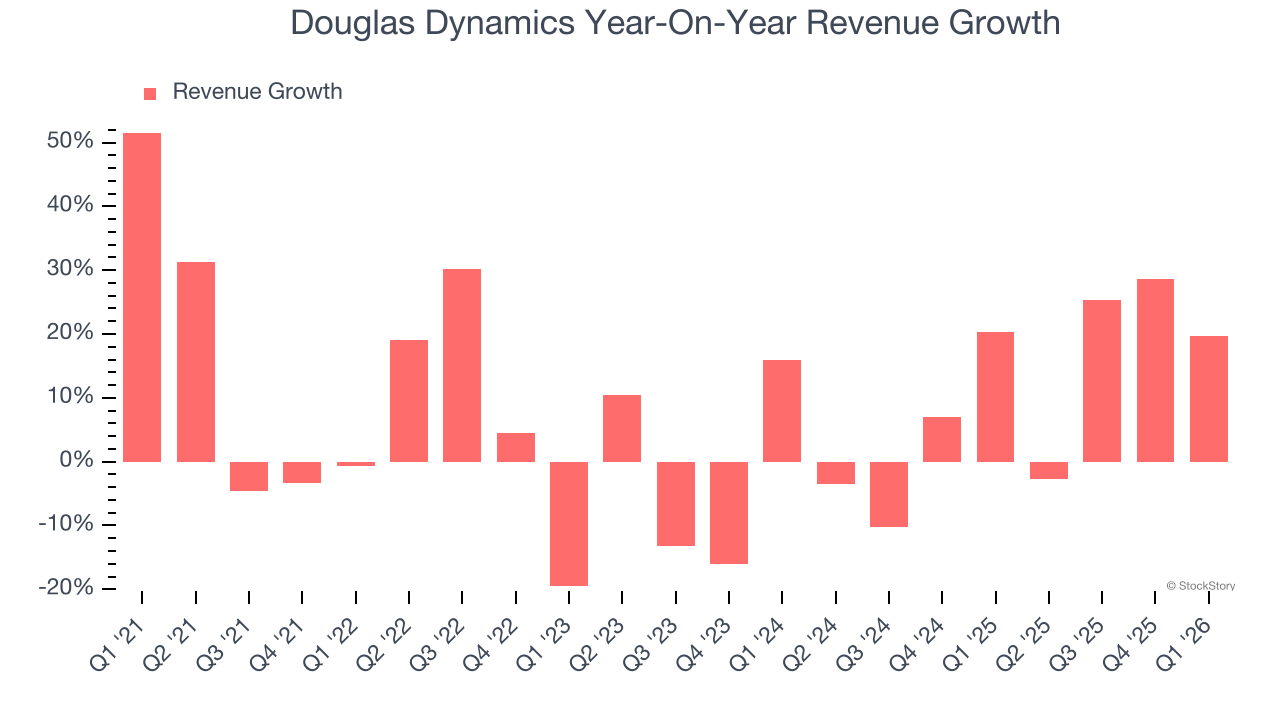

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Douglas Dynamics grew its sales at a tepid 5.7% compounded annual growth rate. This wasn’t a great result compared to the rest of the industrials sector, but there are still things to like about Douglas Dynamics.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Douglas Dynamics’s annualized revenue growth of 8.1% over the last two years is above its five-year trend, suggesting some bright spots.

This quarter, Douglas Dynamics reported year-on-year revenue growth of 19.8%, and its $137.8 million of revenue exceeded Wall Street’s estimates by 3.4%.

Looking ahead, sell-side analysts expect revenue to grow 9.1% over the next 12 months, similar to its two-year rate. This projection is admirable and implies its newer products and services will catalyze better top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

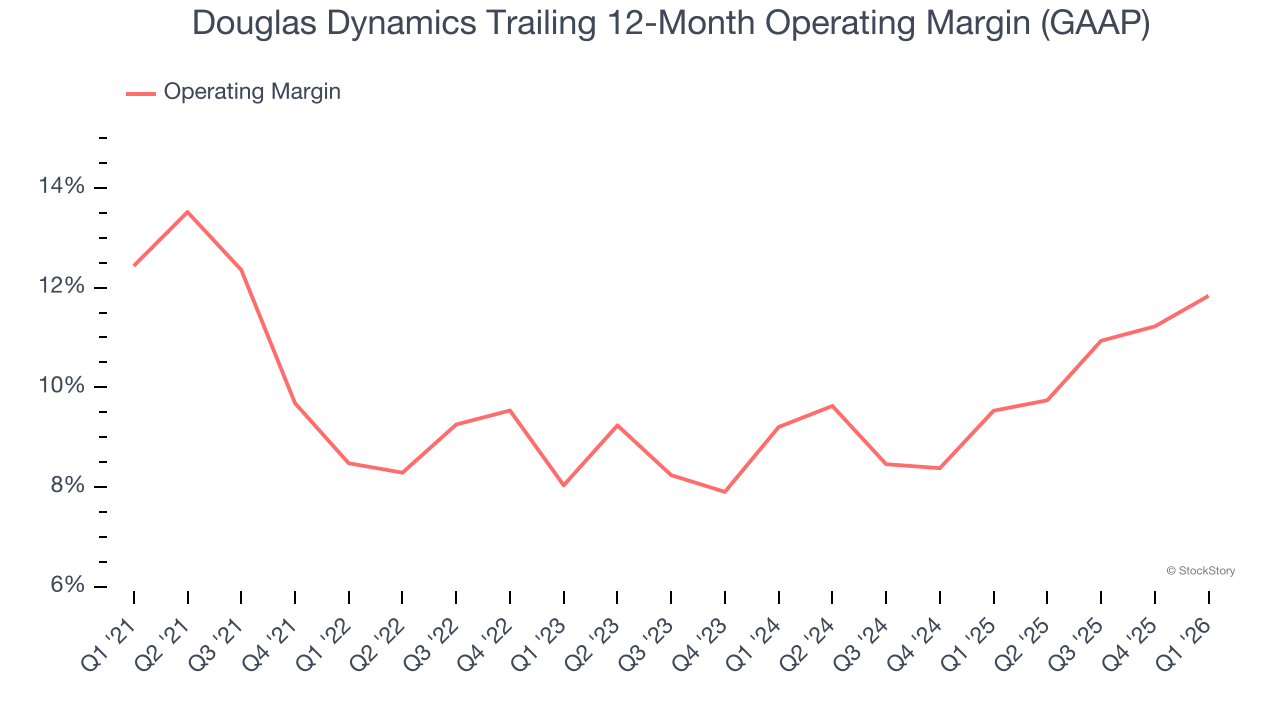

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Douglas Dynamics has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 9.5%, higher than the broader industrials sector.

Looking at the trend in its profitability, Douglas Dynamics’s operating margin rose by 3.4 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Douglas Dynamics generated an operating margin profit margin of 7.2%, up 4.4 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

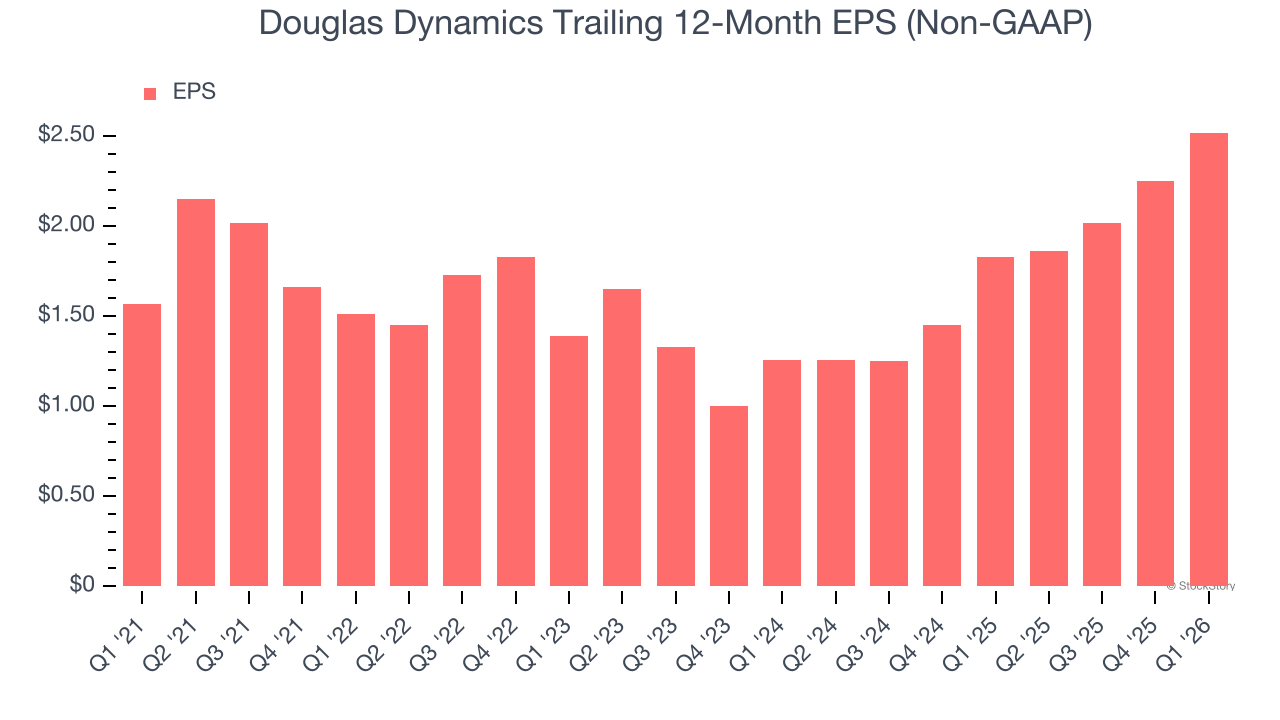

Douglas Dynamics’s EPS grew at 9.9% compounded annual growth rate over the last five years, higher than its 5.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Douglas Dynamics’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Douglas Dynamics’s operating margin expanded by 3.4 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Douglas Dynamics, its two-year annual EPS growth of 41.4% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, Douglas Dynamics reported adjusted EPS of $0.36, up from $0.09 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Douglas Dynamics’s full-year EPS of $2.52 to grow 2.8%.

Key Takeaways from Douglas Dynamics’s Q1 Results

It was good to see Douglas Dynamics beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 3.3% to $46.03 immediately following the results.

Indeed, Douglas Dynamics had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)