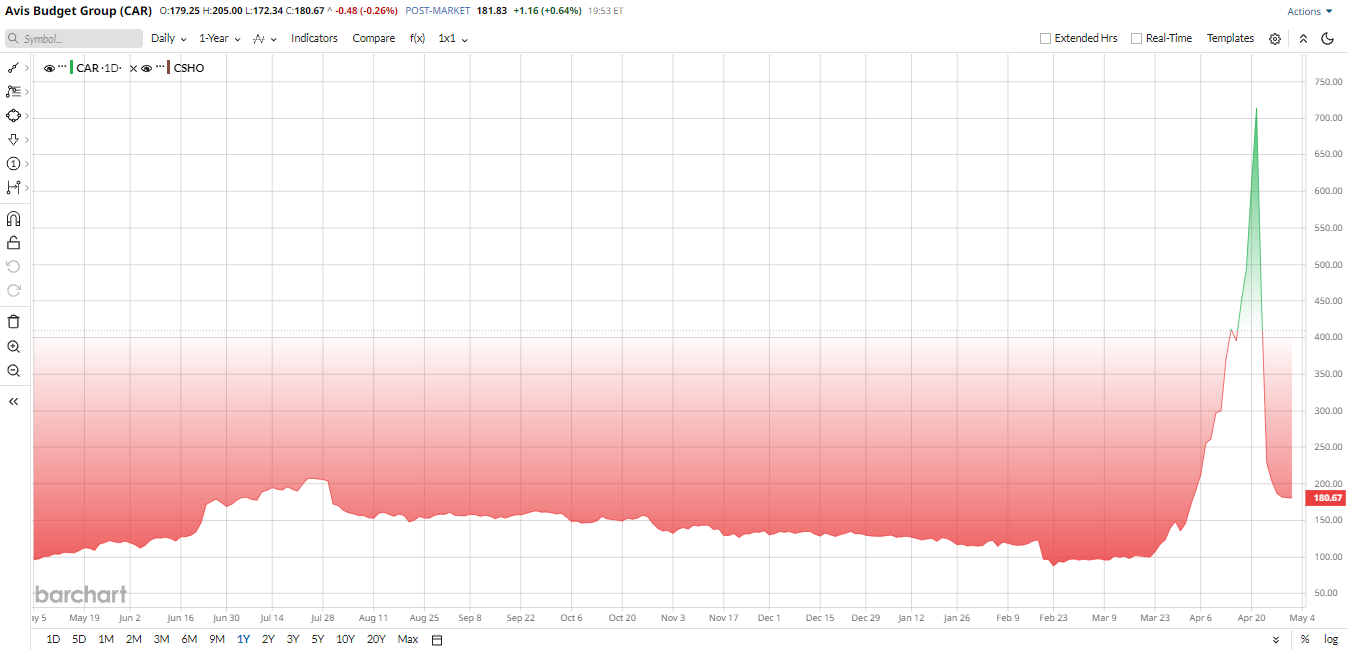

Avis Budget (CAR) is suddenly at the center of a market drama. Over the past few months, heavily shorted travel and mobility stocks have become prime targets for retail traders hunting for quick gains. CAR stock fit that playbook perfectly. It had high short interest, volatile fundamentals, and a long history of sharp moves.

In late April 2026, shares exploded higher in a classic short squeeze, catching bearish investors off guard. But the rally did not last. The stock reversed just as quickly after a large shareholder reduced its stake, and earnings raised fresh concerns.

Now, CEO Brian Choi has publicly pointed to Pentwater Capital as a key force behind the squeeze and the unwind. The company says it is reviewing the situation.

For investors, this turns a trading story into something more complicated.

A Quick Look at Avis Budget’s Business

Avis Budget runs a global car rental business. It operates under the Avis and Budget brands. The company makes money from renting vehicles to travelers and businesses. It also manages a massive fleet, which means costs, pricing, and asset values matter a lot.

The company is also making big moves this year. It is restructuring parts of its fleet strategy and pulling back on aggressive EV expansion after earlier missteps. It is also trying to improve pricing discipline and cut costs. These steps could help margins over time, but they take time to show results. Presently, execution risk is still high.

As said earlier, CAR stock has delivered big gains over the past year, but the path has been messy. Shares surged more than 95% over the last 12 months and jumped over 40% year-to-date (YTD). The short squeeze drove most of that upside. But the stock dropped sharply after earnings. Investors are worried about rising capital spending, especially fleet investments and EV-related costs. That pressure is hitting sentiment.

Valuation seems mixed. CAR trades at about 0.5 times sales, which is below the sector average of 1.4. That looks cheap. But its enterprise value to EBITDA sits around 7 to 8 times, closer to peers. With weak earnings visibility and high debt, the market is not giving it a deep discount. It looks fairly valued for the risk.

Avis Budget Tops Q1 Estimates

Avis Budget reported its Q1 quarter with mixed signals. Revenue came in around $2.5 billion, down roughly 4% year-over-year (YoY). The Americas segment remained the largest contributor, while international operations showed softer trends due to uneven travel demand.

The company posted a net loss of about $283 million, a sharp decline from a profit a year ago. Adjusted EPS came in at a loss of $3.21, reflecting higher costs and weaker pricing in some regions. That is a big swing and not what investors wanted to see.

Free cash flow was negative for the quarter as fleet spending increased. Cash and equivalents stood near $600 million, giving the company some flexibility, but not a huge cushion considering its debt load.

CEO Brian Choi tried to stay optimistic. He said the company is focused on “disciplined fleet management and long term value creation.” That sounds good, but investors want to see results.

Looking ahead, management expects near-term pressure to continue. Revenue for the next quarter is expected to stay flat or slightly down. Full-year guidance suggests a modest recovery, but not a sharp rebound. Analysts expect full-year revenue to be around $11 billion and adjusted EPS to grow 136%.

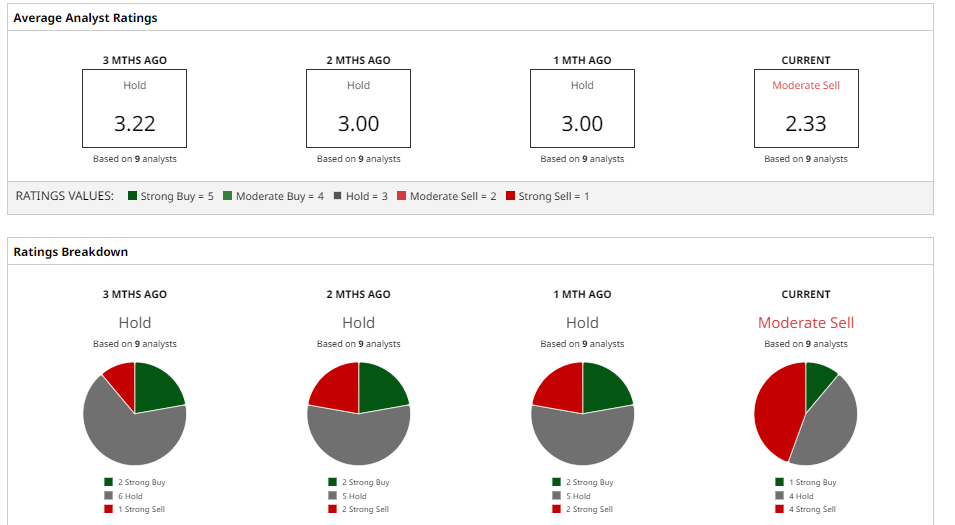

What Do Analysts Think About CAR Stock?

Wall Street is cautious. Morgan Stanley recently lowered its price target to $110 and kept an “Equal Weight” rating. The firm noted that “earnings visibility remains limited given fleet costs.” Goldman Sachs set a target near $105 with a “Neutral” stance, saying the stock reflects both upside and risk.

J.P. Morgan is slightly more optimistic. It has a target of around $120 and believes cost controls could stabilize margins. Still, it warned that volatility will remain high.

Overall, the consensus rating is “Moderate Sell.” The average price target sits near $120, implying a further 34% decline from current levels. Analysts agree on one thing. This is not a stable story yet.

So, Should You Keep Playing CAR Stock?

CAR is not a long term investment at this time. It is a trading vehicle. The short squeeze indicated how much volatility it can show if it can easily erase profits as well. But the company is on the nose, and excess spending is weighing down the forecast. So, if you like a gamble, CAR may be for you. But if you want it to grow, then maybe not. At present, risk outweighs reward.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Abbott%20Laboratories%20vials%20and%20Logo-by%20Melniov%20Dmitriy%20via%20Shutterstock.jpg)

/Intuit%20Inc%20logo-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)