How many times have we seen it? A dividend stock that offers a high yield at first, but over time, weak earnings or large debts can force companies to reduce or even suspend their dividends.

With that in mind, it’s important to look beyond dividend yield and consider the company’s ability to consistently pay and even grow dividends. That’s where companies from the Dividend Kings list come in. Dividend Kings are stocks that have paid and increased their dividends for at least the last 50 consecutive years. The result? A more established record that can go a long way toward supporting a stable, passive income.

Today, I’ll be covering the top-yielding Dividend King and why Wall Street analysts are still positive on it.

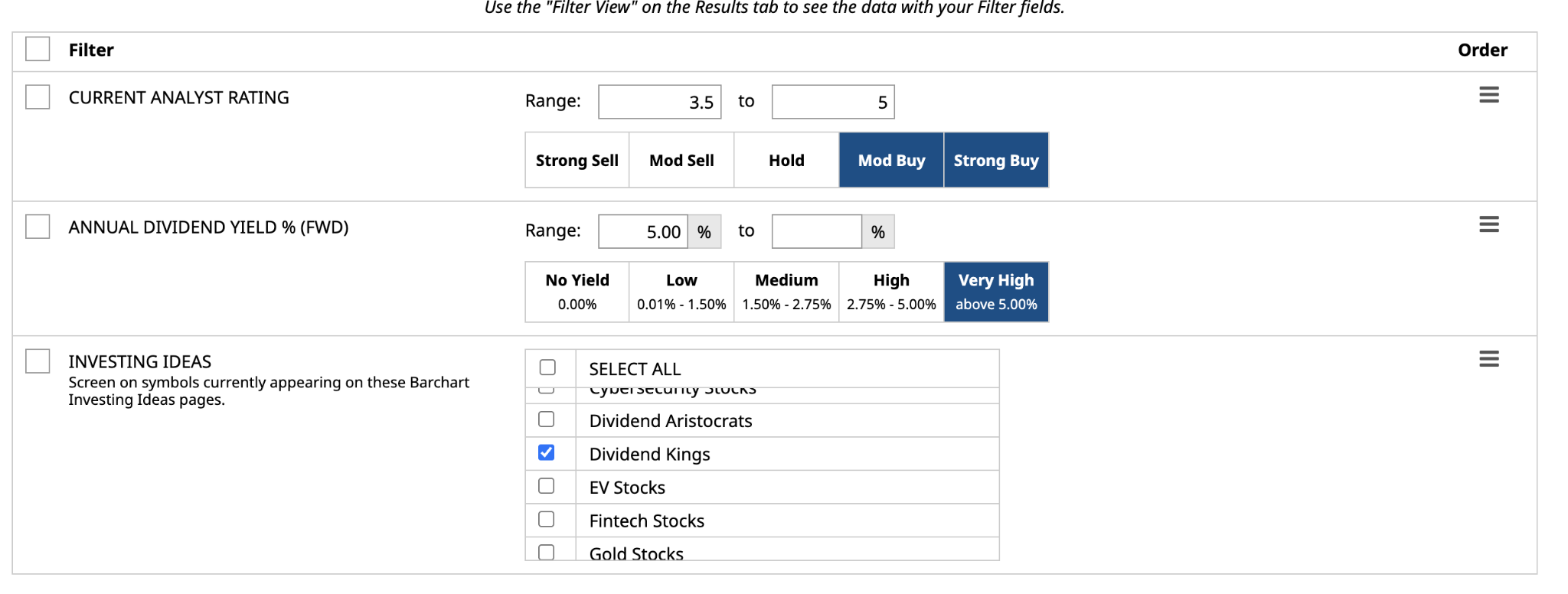

How I identified the highest-yielding Dividend King

I used Barchart’s Stock Screener and selected the criteria below to come up with a list of top-yielding Dividend Kings:

- Current Analyst Rating (Average Score): 3.5 to 5.

- Current Analyst Rating: Moderate to Strong Buy.

- Dividend Investing Ideas: Dividend Kings.

The screener came up with the following results, with the highest-yielding stock at the top:

Altria Group (MO)

Altria Group is a leading tobacco company that manufactures cigarettes, oral tobacco, and e-vapor products. It’s one of the largest and best-known tobacco companies in the U.S and owns Philip Morris USA, which generates the bulk of its revenues and is behind the popular Marlboro brand. The company is expanding beyond traditional cigarettes and into oral nicotine and smokeless tobacco.

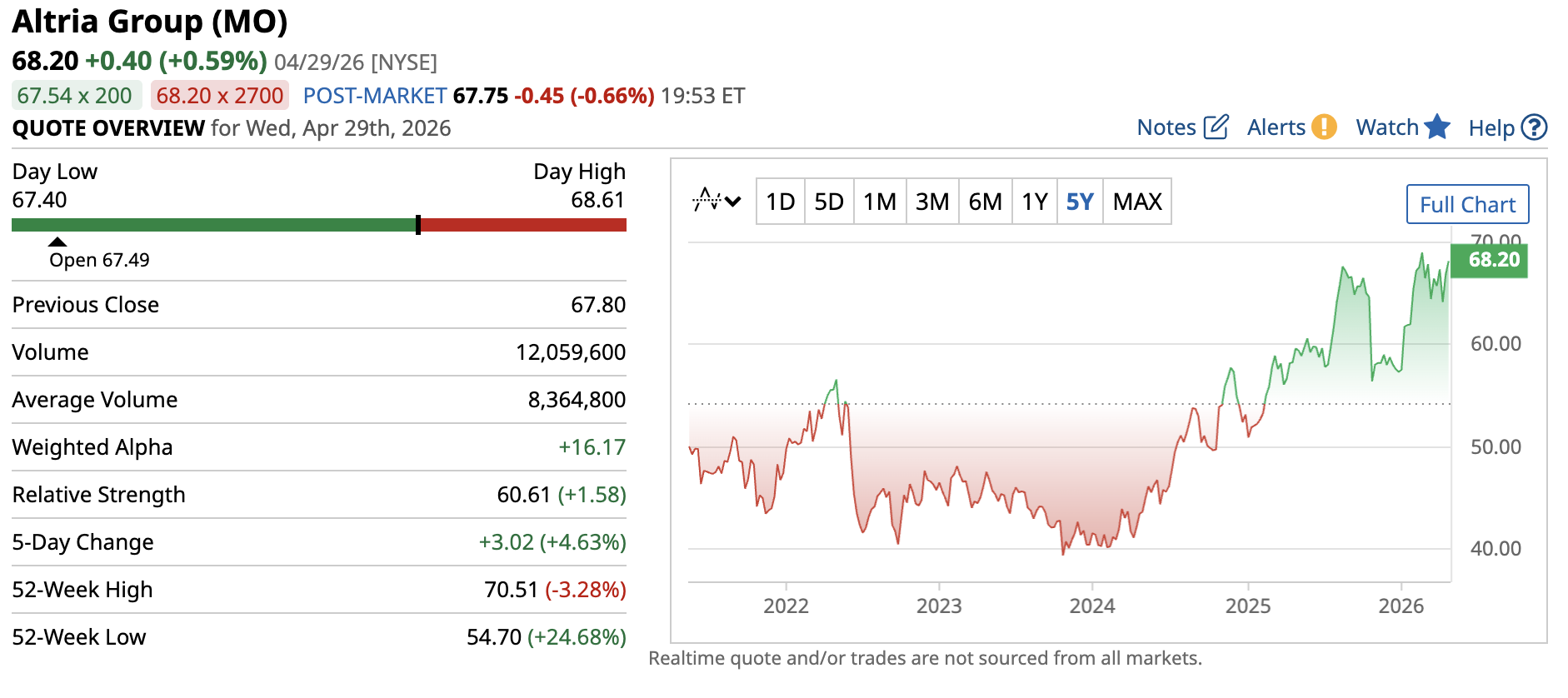

Altria’s stock performance

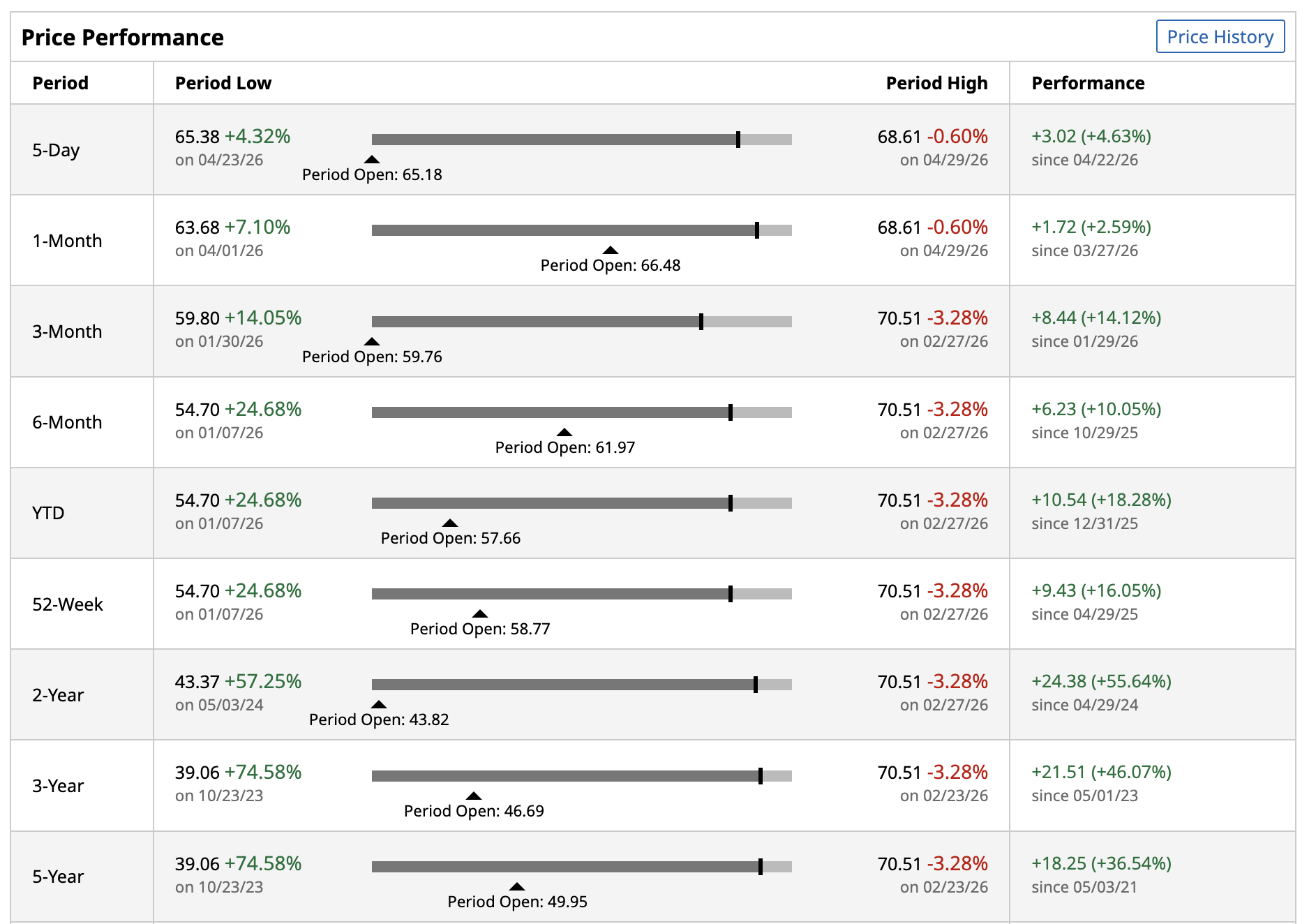

Altria currently trades at over $68 and is up 18.3% year to date, at least partly because of its attractive dividend yield, stable earnings outlook, and aggressive share buybacks. In the past five years, the stock has gone up over 36%- not including dividends.

So far, the stock is also outperforming the S&P 500 (SP500) year to date. I'm not entirely surprised, as the market has faced unprecedented uncertainty this year, leading many investors to rotate into defensive consumer staples like Altria. The company is also mature, generates stable cash flows, and has strong pricing power to help it offset lower shipment volumes for cigarette products.

Still, Altria faces ongoing challenges, including declining cigarette sales, regulatory risks, and growing competition from cigarette alternatives. That said, Altria could still benefit investors seeking for income.

Altria’s dividend profile

Altria is best known for its consistent cash flows and dividend payouts, making it a staple among dividend investors. The company has increased dividends 60 times over the past 56 years, and it currently pays a forward annual dividend of $4.24, yielding 6.4%.

Looking at its latest financials, Altria delivered adjusted diluted earnings per share of $1.30 in the fourth quarter of 2025, up 0.8% from the previous year. Meanwhile, full-year adjusted diluted EPS stood at $5.42, up 4.4% year over year- comfortably covering the dividend.

Although it missed expectations, EPS still grew, despite a slight decline in full-year revenues, as cigarette volumes dropped and competition from smoke-free alternatives increased.

Looking ahead to Altria’s first-quarter results, analysts are expecting EPS of $1.24, slightly higher than the $1.23 reported in the first quarter of 2025.

Altria’s dividend payout ratio is at 76.5%. This ratio measures the portion of the company’s earnings paid out as dividends. That said, the company’s dividends are well-covered by its earnings. Management is targeting mid-single-digit dividend-per-share growth annually through 2028.

First-quarter earnings in focus

Altria is reporting its first-quarter earnings today, and investors are eager to see how the company is dealing with ongoing challenges.

With declining cigarette volumes impacting the tobacco industry, investors want to see if the company can maintain its pricing power to offset these lower volumes. Analysts expect the downturn in smokeable products to continue, but if Altria can maintain better pricing, it could keep its revenues stable.

Meanwhile, Altria’s expansion into oral tobacco products could be its next big growth driver, especially its on! Nicotine Pouches. Investors want to see how well the company executes this expansion and whether this new product line could fuel long-term growth.

Altria missed certain estimates in its recent reports, so it's important for the company to show that it can stay profitable enough to keep growing its dividends. It also has to keep its margins healthy through cost controls or better pricing, while its investments in new products should support revenue growth, especially if traditional cigarette volumes continue to decline.

How does Wall Street rate Altria?

Now, let’s take a look at what Wall Street analysts are saying about Altria. A consensus among 14 analysts rates Altria stock a “Moderate Buy," and the average score is 3.5 out of 5. Meanwhile, the high target price suggests as much as 8.5% upside over the next year. Indeed, investors buy and hold MO stock for the dividend, not it's capital appreciation.

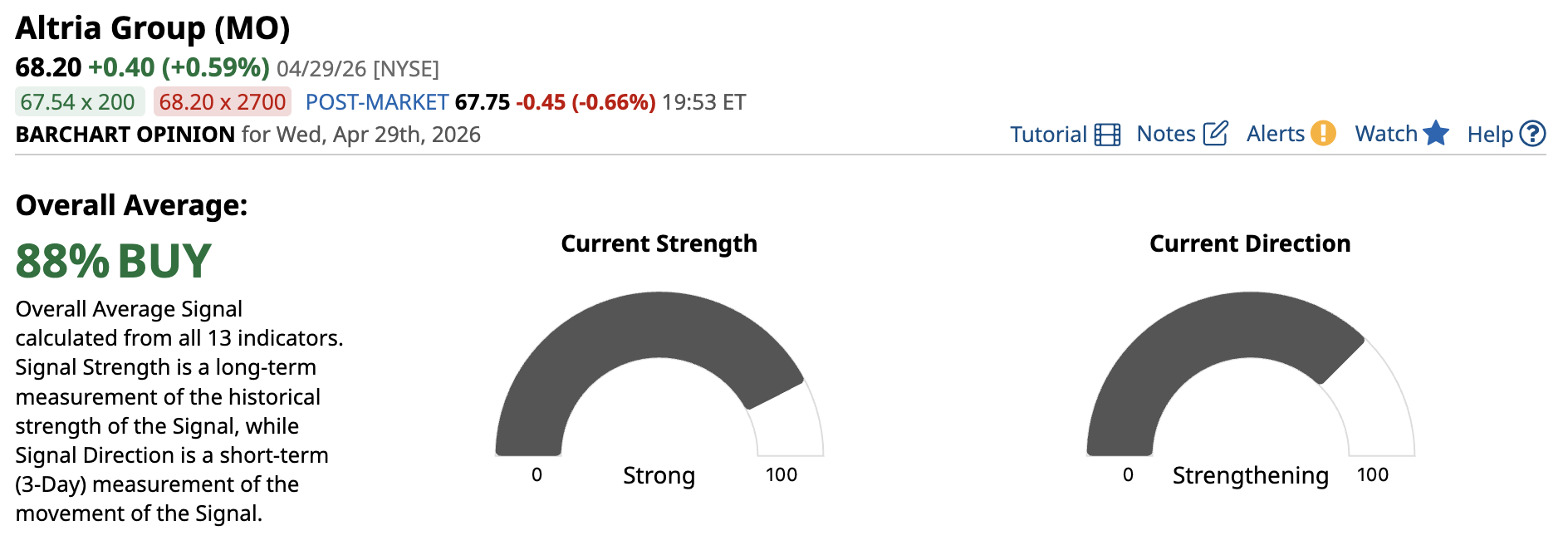

Now, turning to the technical dashboard, Barchart Opinion currently shows an 88% buy rating. Looking at the stock's current direction and strength, the rating suggests that Altria is has some upbeat price action coupled with strong momentum.

Is Altria a buy?

For investors seeking reliable, income-generating assets, Altria stock could be a solid idea. The company’s strong pricing power, stable cash flows, and expansion into smoke-free alternatives could make it a defensive yet high-yielding addition to dividend portfolios.

With its consistent dividend increases and positive outlook on dividend growth, it could offer investors stability and consistent income while macro conditions remain uncertain.

On the date of publication, Rick Orford did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)