The modular data center space is quickly becoming one of the fastest‑growing parts of digital infrastructure, with the market expected to climb from $29.93 billion in 2024 to $79.49 billion by 2030 at a 17.7% at a CAGR. That kind of jump shows how much demand is building for ready‑made, scalable facilities that can be set up quickly and tuned for heavy AI and cloud use.

Super Micro Computer (SMCI) is moving right into that space, expanding its Data Center Building Block Solutions (DCBBS) with new Arm‑based systems and OCP‑ready setups for modern data centers. At the same time, the company is dealing with some baggage, including an investor class action after big share losses and a sharp drop following the loss of a major Oracle AI server deal, which raised doubts about its supply planning and demand visibility.

All of this leaves the story at a key turning point, with the stock still trying to win back trust and prove whether it deserves a “Buy,” “Sell,” or “Hold.”

SMCI’s Financial Performance

San Jose, California‑based Super Micro Computer is a manufacturer of server, storage, and data center systems that focuses on high‑performance, energy‑efficient infrastructure for AI, cloud, and enterprise workloads.

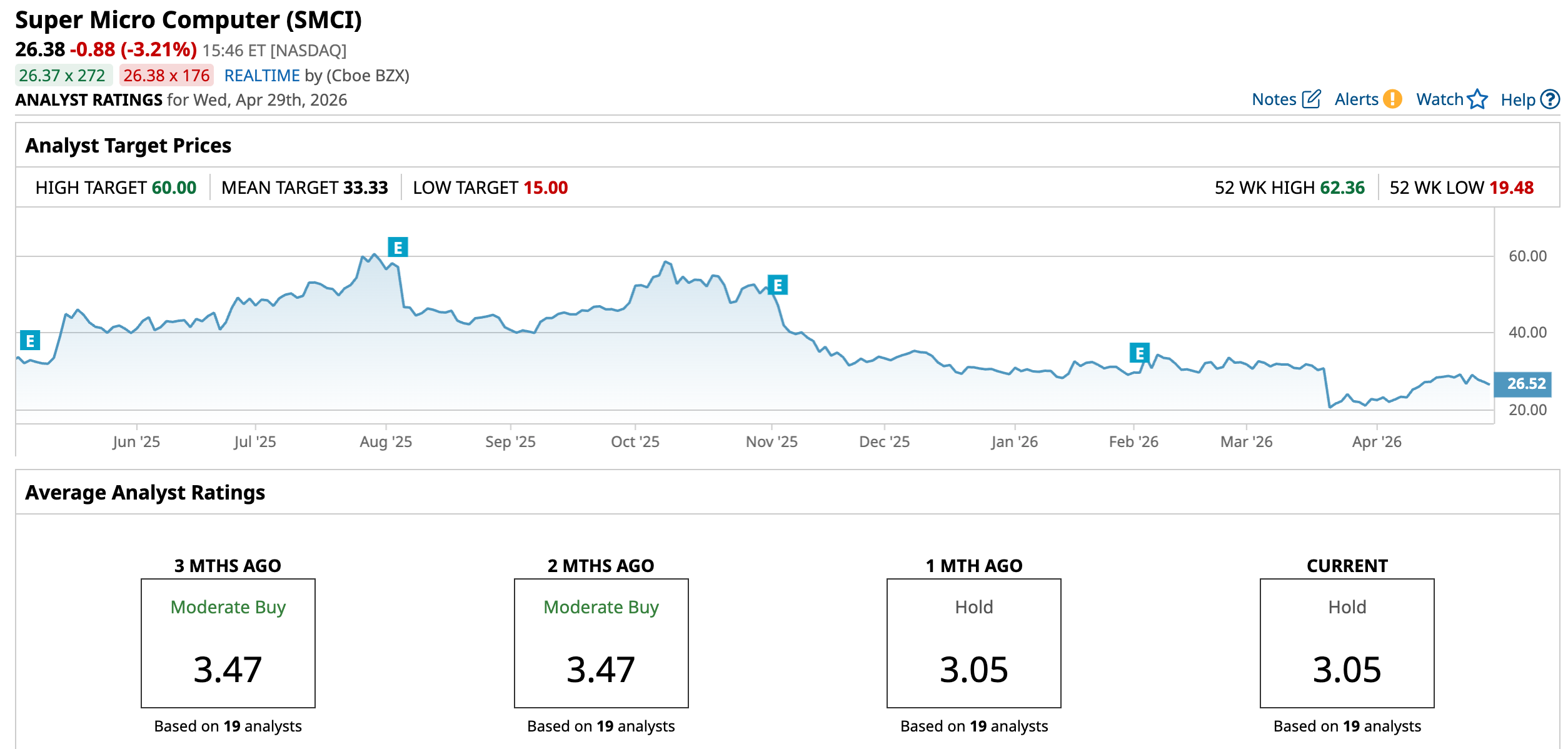

Its stock closed at $27.25 on April 28, down 10.47% year-to-date (YTD) and 27.21% over the past 52 weeks.

This business is now valued at $16.32 billion and trades at 21.10 times trailing earnings and 0.58 times sales, while the sector sits closer to 33.95 times earnings and 3.48 times sales, which points to a clear discount even with its growing role in data center build-outs.

Their latest reported quarter, for the period ending December 25, showed earnings of $0.56 per share compared with a consensus estimate of $0.41, a 36.59% beat that signals stronger profitability than the market expected. This report also showed $12.68 billion in sales for December 2025, up 152.75% from the prior quarter.

Its net income came in at $400.56 million, a 138.02% quarter-over-quarter (QOQ) increase that displays strong demand for the company’s data center platforms.

That performance on the income statement sits next to a tougher cash picture and makes the story more complicated. Their operating cash flow for December 2025 was -$941.42 million, a 2.60% drop from the prior quarter, which tells us growth is still being funded heavily through the balance sheet.

This negative trend also showed up in net cash flow of -$978.58 million, a 0.57% decline QOQ, and it suggests Super Micro Computer remains in a heavy investment phase rather than a period of steady cash generation.

Super Micro Computer Strengthens Its AI Infrastructure

Super Micro Computer just announced its largest U.S. site so far. The new Silicon Valley campus covers about 32.8 acres and adds more than 714,000 square feet of space. This is now the company’s fourth Bay Area location and takes its regional footprint to almost four million square feet.

The facility will handle advanced design, manufacturing, testing, and global shipping for its Data Center Building Block Solutions. This expansion is meant to lift U.S. production capacity and help the company deliver new AI data center gear more quickly.

On the product side, Super Micro recently rolled out new Arm‑based server platforms built around the Arm AGI CPU in both 2U and 5U designs. These servers offer high core counts, support up to 6TB of DDR5 memory, and include flexible I/O options for demanding AI and high-performance workloads.

Further, the company introduced Open Compute Project ORv3-compliant racks, giving customers more flexibility when setting up next-generation AI infrastructure. Earlier this month, it added compact, energy-efficient systems based on AMD EPYC 4005 series chips for tight, power‑limited edge environments. These smaller systems are built to speed up AI inferencing and everyday computing tasks and come in box, short-depth 1U, and slim tower designs. They focus on better performance, stronger security, and lower overall ownership costs.

Taken together, these moves show Super Micro is pushing hard across the AI hardware stack, from big U.S. campuses to new server architectures and edge solutions, as it tries to open up more growth paths in the data center and beyond.

What the Street Is Really Saying About SMCI

Next up for Super Micro Computer is an earnings report due on May 5 after the close, and expectations are quite high. For the March 2026 quarter, the average earnings estimate sits at $0.55 per share, up from $0.19 a year earlier, which works out to an estimated year‑over‑year gain of about 189.47%. That kind of jump shows the degree of confidence in the company’s bigger push into data center and Arm‑based server sales.

There is still some hesitation in the background. Earlier in April, Vijay Rakesh and his team at Mizuho shifted to a “Neutral” rating on SMCI and cut their price target from $33 to $25, pointing to possible near‑term pressure even while acknowledging the company’s strong position in server technology.

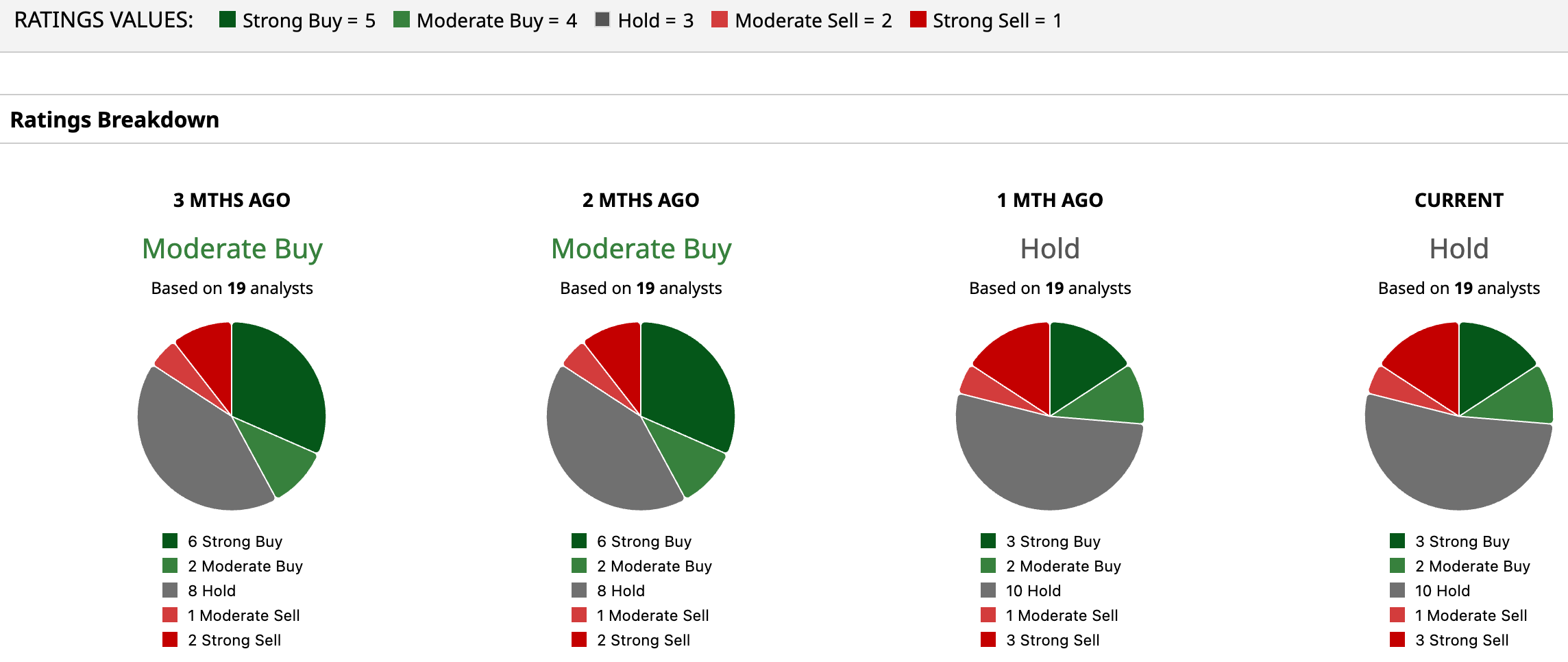

Even after that downgrade, the broader view is not strongly negative. Across 19 voices covering the stock, the consensus rating sits at “Hold.” The average 12‑month price target is $33.33, implying a 26.4% upside from recent levels, and with the Street-high target of $60, there is still room for gains of 127.5% from here.

Conclusion

SMCI looks more like a “Hold” right now, with some room for people who believe in its ARM and AI data center push. The shares trade cheaper than many peers on earnings and sales, but the heavy cash needs and cautious outlook keep risk on the higher side. Over the next few quarters, the move is more likely to be slow and choppy rather than a sharp breakout, and fresh earnings results will probably decide whether the story really improves or stalls.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)