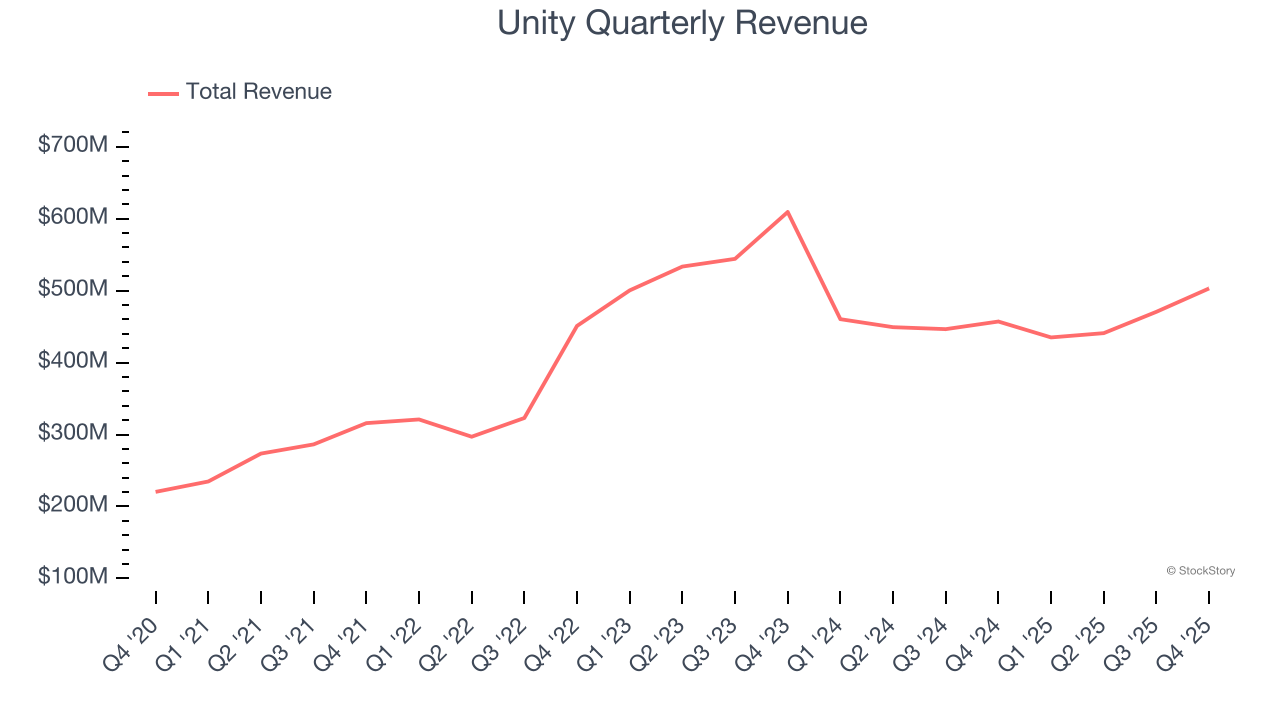

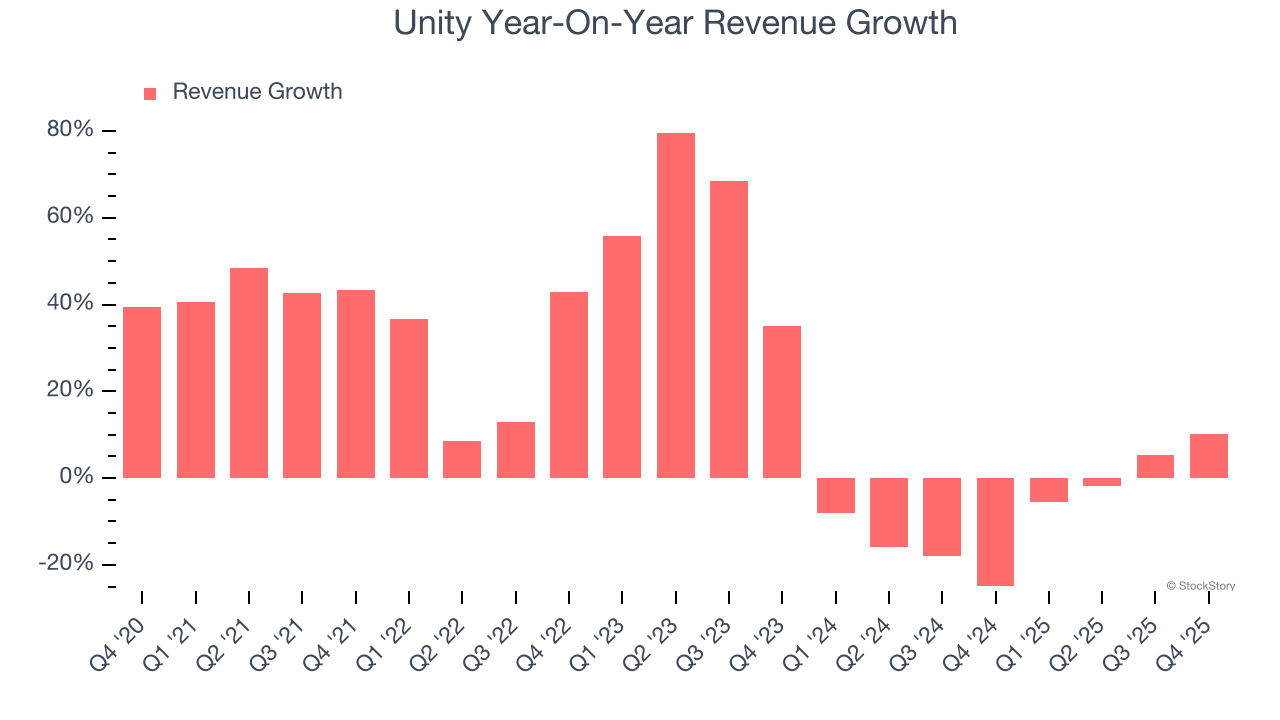

Interactive software platform Unity (NYSE:U) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 10.1% year on year to $503.1 million. On the other hand, next quarter’s revenue guidance of $485 million was less impressive, coming in 0.8% below analysts’ estimates. Its non-GAAP profit of $0.24 per share was 15.5% above analysts’ consensus estimates.

Is now the time to buy Unity? Find out by accessing our full research report, it’s free.

Unity (U) Q4 CY2025 Highlights:

- Revenue: $503.1 million vs analyst estimates of $492.1 million (10.1% year-on-year growth, 2.2% beat)

- Adjusted EPS: $0.24 vs analyst estimates of $0.21 (15.5% beat)

- Adjusted EBITDA: $124.9 million vs analyst estimates of $117.1 million (24.8% margin, 6.6% beat)

- Revenue Guidance for Q1 CY2026 is $485 million at the midpoint, below analyst estimates of $489.1 million

- EBITDA guidance for Q1 CY2026 is $107.5 million at the midpoint, below analyst estimates of $116.7 million

- Operating Margin: -21.2%, up from -27.1% in the same quarter last year

- Free Cash Flow Margin: 23.6%, down from 32.1% in the previous quarter

- Market Capitalization: $12.44 billion

Company Overview

Powering over half of the world's mobile games and expanding into industries from automotive to architecture, Unity (NYSE:U) provides software tools and services that allow developers to create, run, and monetize interactive 2D and 3D content across multiple platforms.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Unity’s sales grew at a decent 19.1% compounded annual growth rate over the last five years. Its growth was slightly above the average software company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Unity’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 8% over the last two years.

This quarter, Unity reported year-on-year revenue growth of 10.1%, and its $503.1 million of revenue exceeded Wall Street’s estimates by 2.2%. Company management is currently guiding for a 11.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below average for the sector.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Unity is quite efficient at acquiring new customers, and its CAC payback period checked in at 30.4 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

Key Takeaways from Unity’s Q4 Results

We enjoyed seeing Unity beat analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its revenue and EBITDA guidance for next quarter both missed, and this is weighing heavily on shares. Overall, this was a weaker quarter. The stock traded down 24.1% to $22.15 immediately after reporting.

The latest quarter from Unity’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)