/ServiceNow%20Inc%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

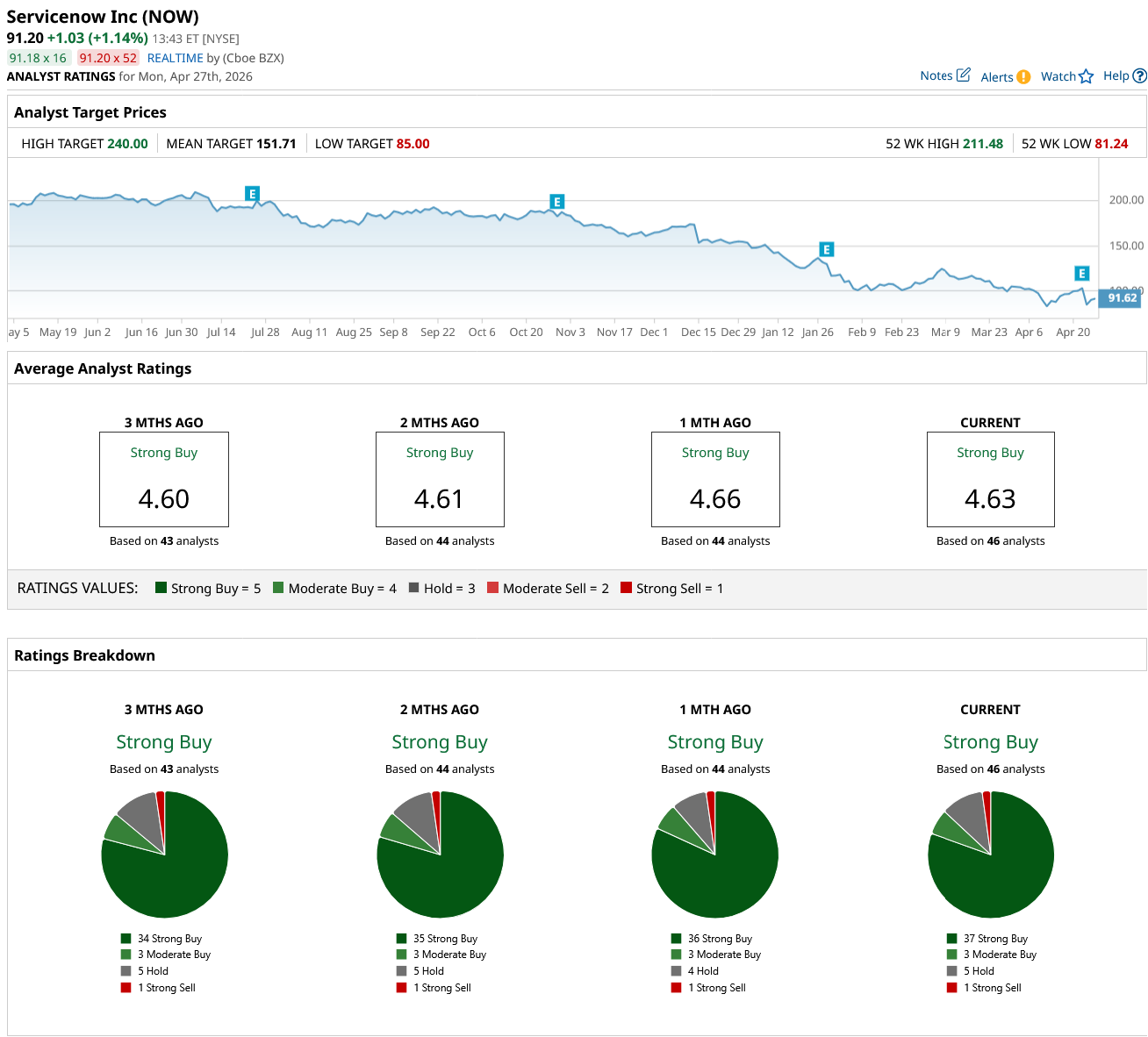

ServiceNow (NOW) has had a difficult stretch in the market, with its stock under significant selling pressure. NOW stock is down about 40% since the start of the year and has fallen roughly 52% over the past twelve months and is hovering close to its 52-week low.

The significant selloff reflects growing concern about the impact of artificial intelligence (AI) on the broader software industry. Investors are increasingly wary that advances in agentic AI could reduce the reliance on traditional enterprise workflow solutions. These fears have weighed heavily on valuation multiples across the sector, and ServiceNow has not been spared.

The selling pressure intensified following ServiceNow’s first-quarter earnings. Although ServiceNow delivered strong financials, the market reaction was negative, with the stock dropping 17.8% the following day.

Management indicated some weakness in subscription revenue due to delayed deals in the Middle East amid ongoing geopolitical tensions. Meanwhile, near-term margin pressure related to the Armis acquisition weighed on NOW stock.

Despite these headwinds, ServiceNow’s underlying fundamentals remain solid. It continues to generate solid growth in subscription revenue and remaining performance obligations (RPO), while customer deal metrics remain solid.

Importantly, ServiceNow is witnessing a meaningful acceleration in AI-driven revenue contributions, with the company now projecting $1.5 billion in AI-specific commitments by 2026. Adoption of its Now Assist, its generative AI-powered suite, has been particularly strong.

ServiceNow Sees Durable Growth

ServiceNow reported a strong first quarter, and its growth trajectory remains solid. The company’s subscription revenue reached $3.67 billion, rising 19% year-over-year (YoY) in constant currency. Growth came despite a modest headwind caused by delays in closing several large deals in the Middle East due to ongoing regional conflict. RPO stood at $27.7 billion, up 23.5%, offering solid demand visibility.

The company’s current RPO came in at $12.64 billion, growing 21%. Meanwhile, the renewal rate remained high at 97%, including contributions from Moveworks, which ServiceNow recently acquired. Moreover, ServiceNow’s customer base continues to scale meaningfully, with 630 clients now generating more than $5 million in annual contract value (ACV). Large deal activity remained healthy, with multiple high-value contracts signed during the quarter.

Customer spending trends are also improving. The number of clients spending over $1 million annually jumped 130% YoY. Moveworks, now integrated into ServiceNow’s employee experience segment, is already contributing meaningfully, closing several seven-figure deals, and witnessing rapid expansion.

A key highlight is the increasing adoption of multiple products on its platform. Most of the company’s largest deals now include a broad mix of offerings, signaling deeper platform integration. In addition, demand for AI-powered solutions is strong. The Now Assist suite is witnessing solid demand and is on track to deliver significant revenue. At the same time, other AI-related products, including AI Control Tower and Raptor DB Pro, are also gaining traction. This demand is translating into larger deal sizes and higher adoption rates.

ServiceNow’s profitability also improved during the quarter. Operating margins improved, supported by AI-related spending efficiencies, while free cash flow remained robust. The company also returned significant capital to shareholders through a large share repurchase program.

Looking ahead, ServiceNow has raised its full-year outlook, projecting continued strong revenue growth despite geopolitical uncertainty. Overall, ServiceNow is well-positioned to deliver strong growth, driven by high renewal rates, a growing customer base, and strong demand for its AI capabilities.

Is NOW Stock a Buy?

ServiceNow faces near-term risks, including delays in geopolitical deals and integration-related margin pressure. Moreover, fear of sector-wide disruption from AI poses challenges. However, its strong retention rate, expanding enterprise footprint, and accelerating AI monetization point to a resilient and growing business.

Given the decline, NOW stock trades at a forward earnings multiple of 34 that appears reasonable relative to its growth profile. Analysts are projecting NOW’s EPS to increase by over 26% in 2026, followed by 27.5% in 2027.

For long-term investors, this pullback in NOW stock offers a solid entry point. Wall Street analysts are also bullish and maintain a “Strong Buy” rating on the stock.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)