Oil is off peak prices as tensions over the Iran war have subsided. As a result, oil stocks such as Chevron Corp. (CVX) have declined. But put option premiums remain high, making them attractive to short-sellers.

CVX closed at $185.21 on Friday, April 24, down 1.27%. It's now well off a peak price of $211.15 on March 27.

How Prior CVX Option Plays Worked Out

I discussed selling short covered calls and cash-secured puts on April 7, “Oil Futures Keep Rising, and Shorting Chevron Covered Calls and Cash-Secured Puts Works.”

That was when CVX was just below $200, at $198.86. Moreover, at the time, the $220.00 call option expiring May 15 was at $1.85. Today, it's down to just 24 cents, making this a profitable trade.

On the other hand, the cash-secured put trade did not work out well. The $185.00 put expiring May 15 was at $2.90, giving an investor a 1.57% yield (i.e., $2.90/$185.00) for the 39-day period.

However, today, the put option is close to the money as CVX is at $185.21. An investor who shorted this put could wait for the account to be assigned to buy shares from the cash collateral. Then, owning 100 shares of CVX, the investor could sell short covered calls.

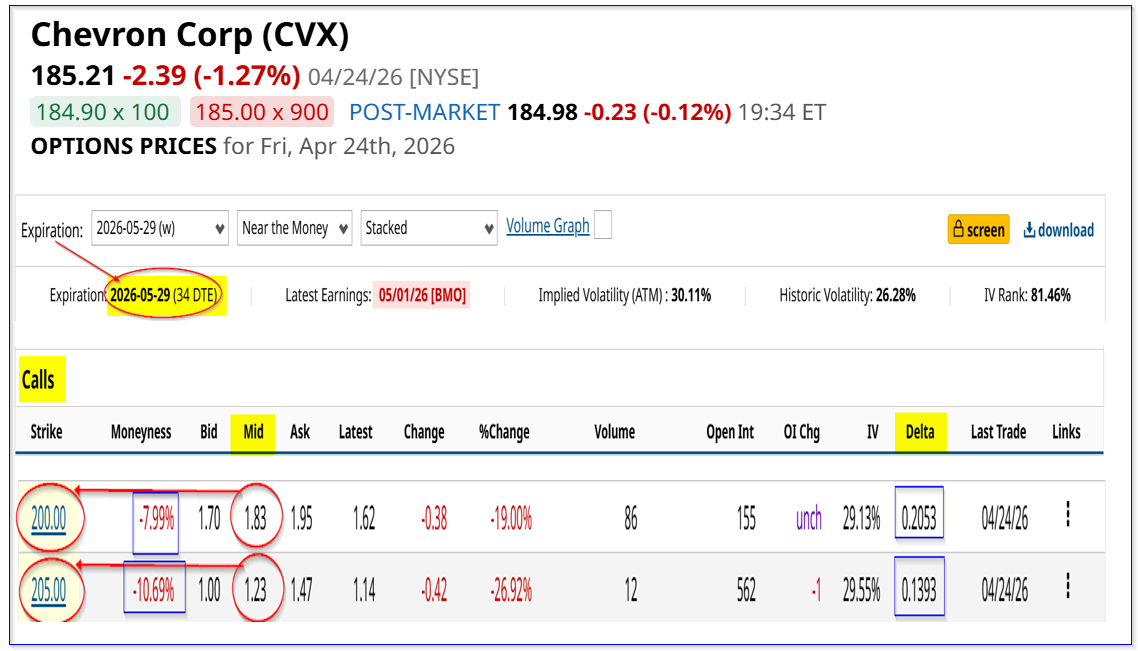

New CVX Covered Call Play

For example, the $205 call option expiring May 29, 34 days from now, shows that the midpoint premium is $1.23. That provides an investor a covered call yield of 0.665% for a strike price that is over 10% above Friday's close.

Moreover, less risk-averse investors could short the $200 call option expiring May 29. That is 8% higher, but the covered call yield is better: $1.86/$185.21 = 1.0%.

Note that the $200.00 call option has a very low delta ratio of just 0.2053. That implies there is less than a 21% chance that CVX will rise to $200 on or before May 29.

However, even if that happens, the investor can allow their shares to be assigned to be sold. In that case, the investor would make a capital gain of 8.0%.

As a result, the total potential return is 9.0% for the next month. That is an attractive return for most investors.

In addition, some investors may want to do a new cash-secured put option play to generate extra income.

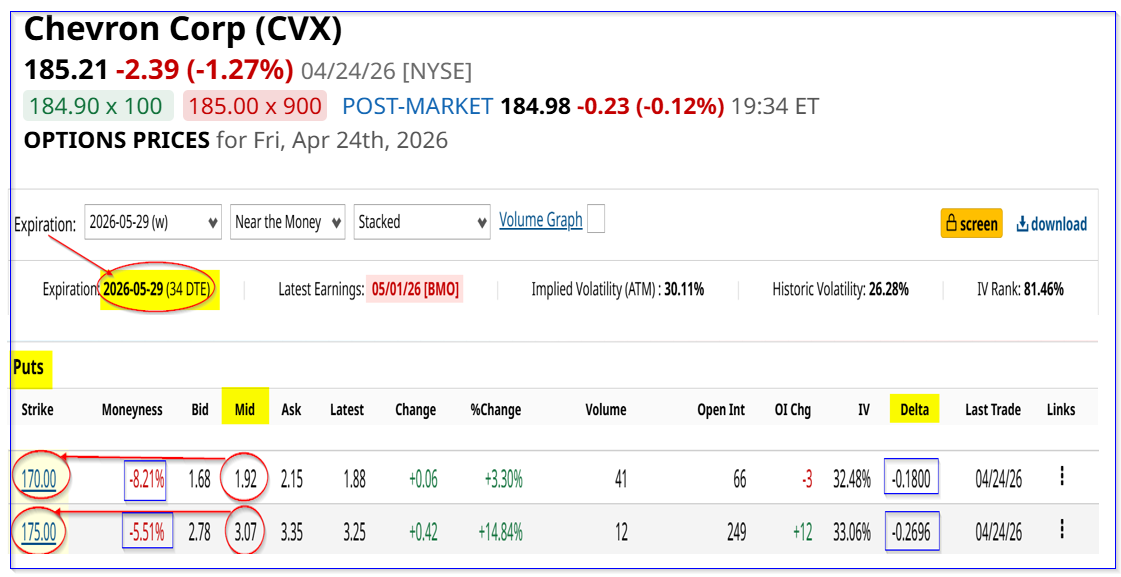

Shorting Cash-Secured CVX Puts

These premiums are higher and provide higher short-play yields. For example, the $175.00 put option contract expiring May 29 has a midpoint premium of $3.07. So, for this play, the investor secures $17,500 with their brokerage firm, and then enters a trade to “Sell to Open” 1 put at $175.00.

The account will then immediately receive $307. As a result, the cash-secured put yield is

$307/$17,500 = 0.0175 = 1.75%

Note this is for a strike price that is 5.51% below Friday's close. For more risk-averse investors, the $170 strike price put, which is 8.21% lower, has a 1.129% yield (i.e., $1.92/$170.00).

Compare that with the $200 call yield, for a 8% distance away from the spot price. It has a 1.0% yield, vs. 1.129% for a 8.21% away put yield.

Note also that the put option has a lower delta ratio of just 18%, implying it has a lower chance of being assigned (vs. the 20.53% delta ratio for the $200 call option).

The bottom line is that shorting out-of-the-money (OTM) puts may be a better play for Chevron stock investors.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)