Financial services company Triumph Financial (NYSE:TFIN) fell short of the market’s revenue expectations in Q1 CY2026 as sales rose 5% year on year to $105.8 million. Its GAAP profit of $0.23 per share was 50% above analysts’ consensus estimates.

Is now the time to buy Triumph Financial? Find out by accessing our full research report, it’s free.

Triumph Financial (TFIN) Q1 CY2026 Highlights:

- Net Interest Income: $86.09 million vs analyst estimates of $87.29 million (15.8% year-on-year decline, 1.4% miss)

- Net Interest Margin: 6.1% vs analyst estimates of 6.3% (23 basis point miss)

- Revenue: $105.8 million vs analyst estimates of $107.5 million (5% year-on-year growth, 1.6% miss)

- EPS (GAAP): $0.23 vs analyst estimates of $0.15 (50% beat)

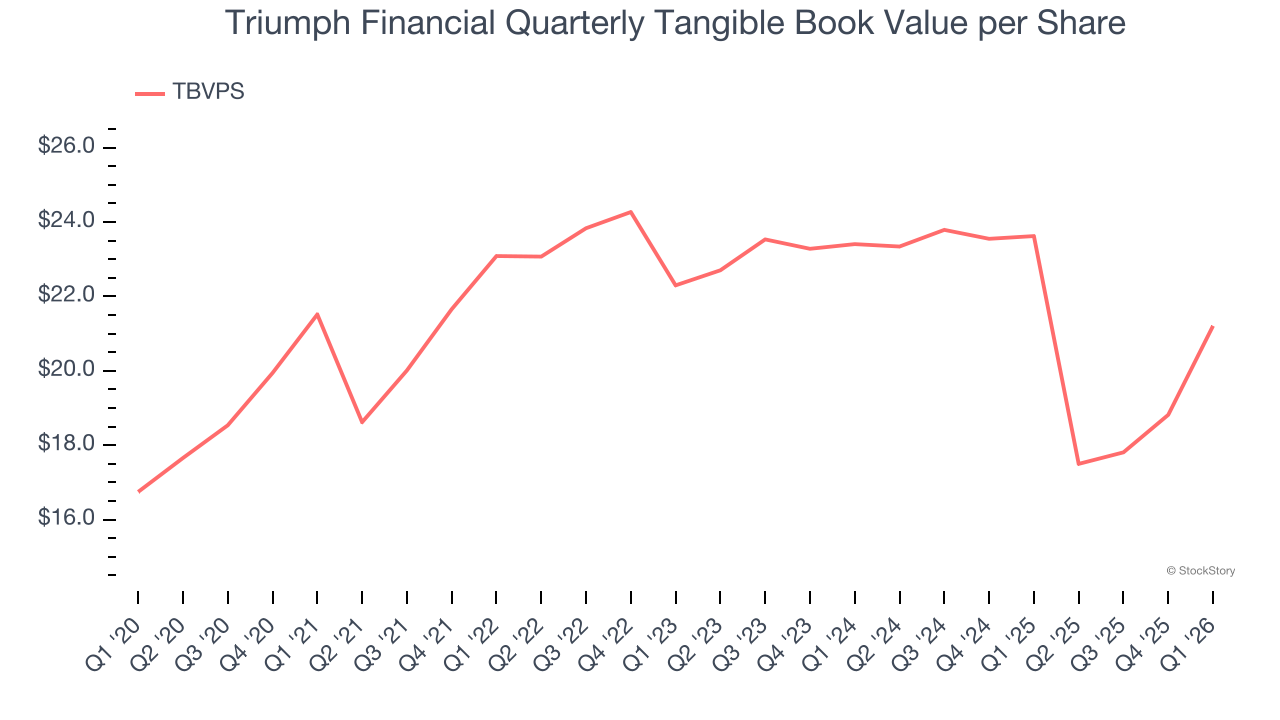

- Tangible Book Value per Share: $21.21 vs analyst estimates of $22.47 (10.2% year-on-year decline, 5.6% miss)

- Market Capitalization: $1.59 billion

Company Overview

Originally focused on traditional banking before pivoting to serve the transportation sector, Triumph Financial (NYSE:TFIN) provides specialized financial services to the trucking industry, including payments processing, factoring, banking, and data intelligence solutions.

Sales Growth

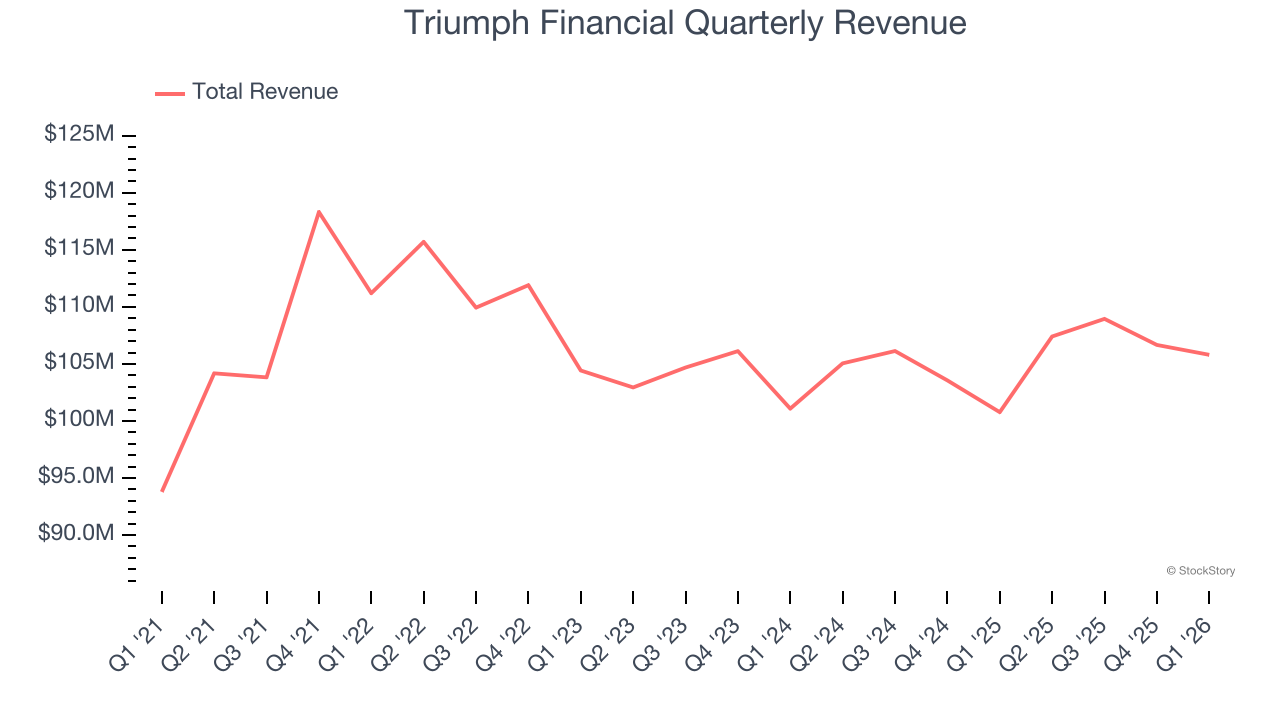

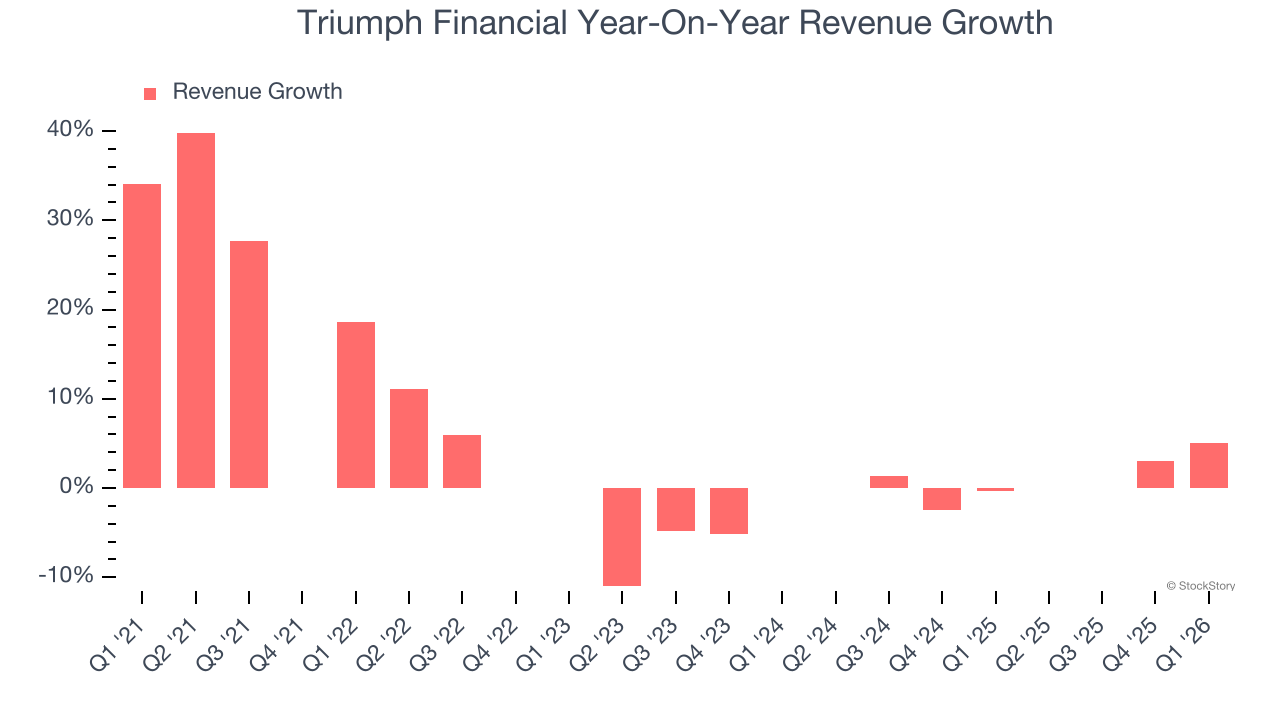

Net interest income and and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities. Over the last five years, Triumph Financial grew its revenue at a sluggish 4.6% compounded annual growth rate. This fell short of our benchmark for the banking sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Triumph Financial’s recent performance shows its demand has slowed as its annualized revenue growth of 1.7% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Triumph Financial’s revenue grew by 5% year on year to $105.8 million, falling short of Wall Street’s estimates.

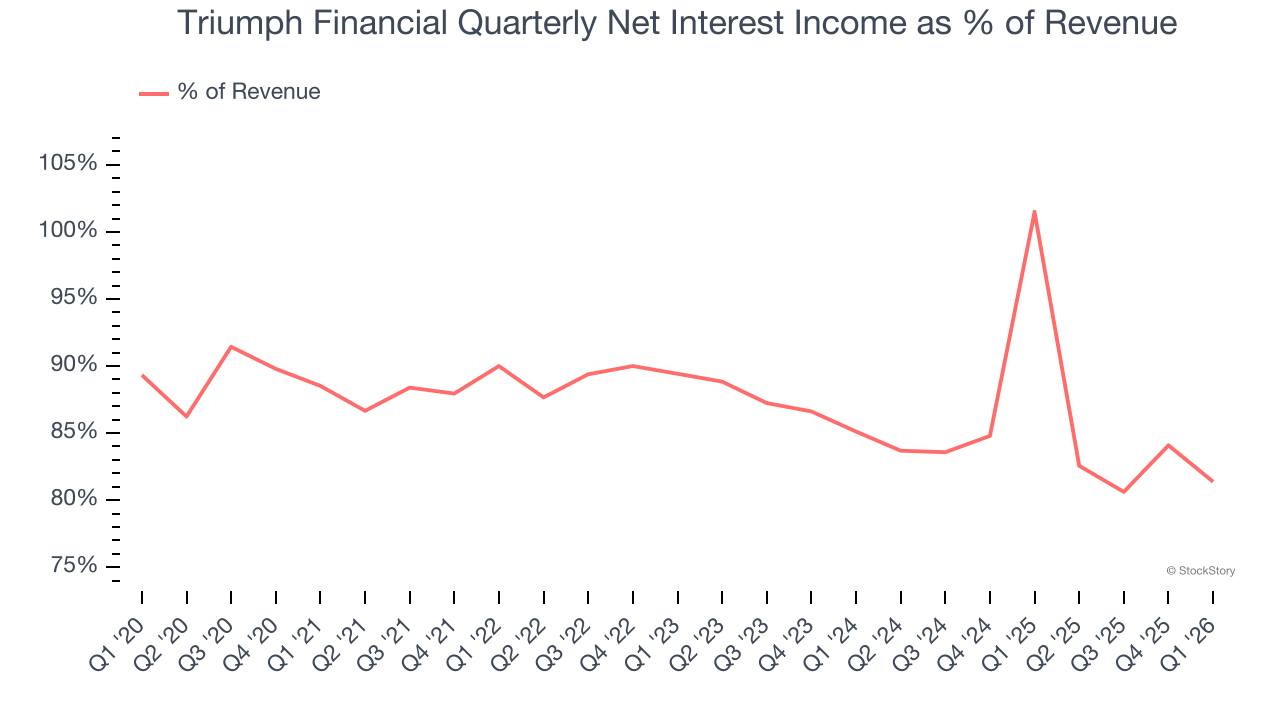

Net interest income made up 87% of the company’s total revenue during the last five years, meaning Triumph Financial barely relies on non-interest income to drive its overall growth.

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark. By excluding intangible assets with uncertain liquidation values, this metric captures real, liquid net worth per share. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

Triumph Financial’s TBVPS was flat over the last five years. A turnaround doesn’t seem to be in sight as its TBVPS also dropped by 4.8% annually over the last two years ($23.41 to $21.21 per share).

Over the next 12 months, Consensus estimates call for Triumph Financial’s TBVPS to grow by 19.5% to $25.35, top-notch growth rate.

Key Takeaways from Triumph Financial’s Q1 Results

It was good to see Triumph Financial beat analysts’ EPS expectations this quarter. On the other hand, its tangible book value per share missed and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 1.6% to $66 immediately following the results.

Triumph Financial underperformed this quarter, but does that create an opportunity to invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

/Apple%20Inc%20logo%20on%20Apple%20store-by%20PhillDanze%20via%20iStock.jpg)