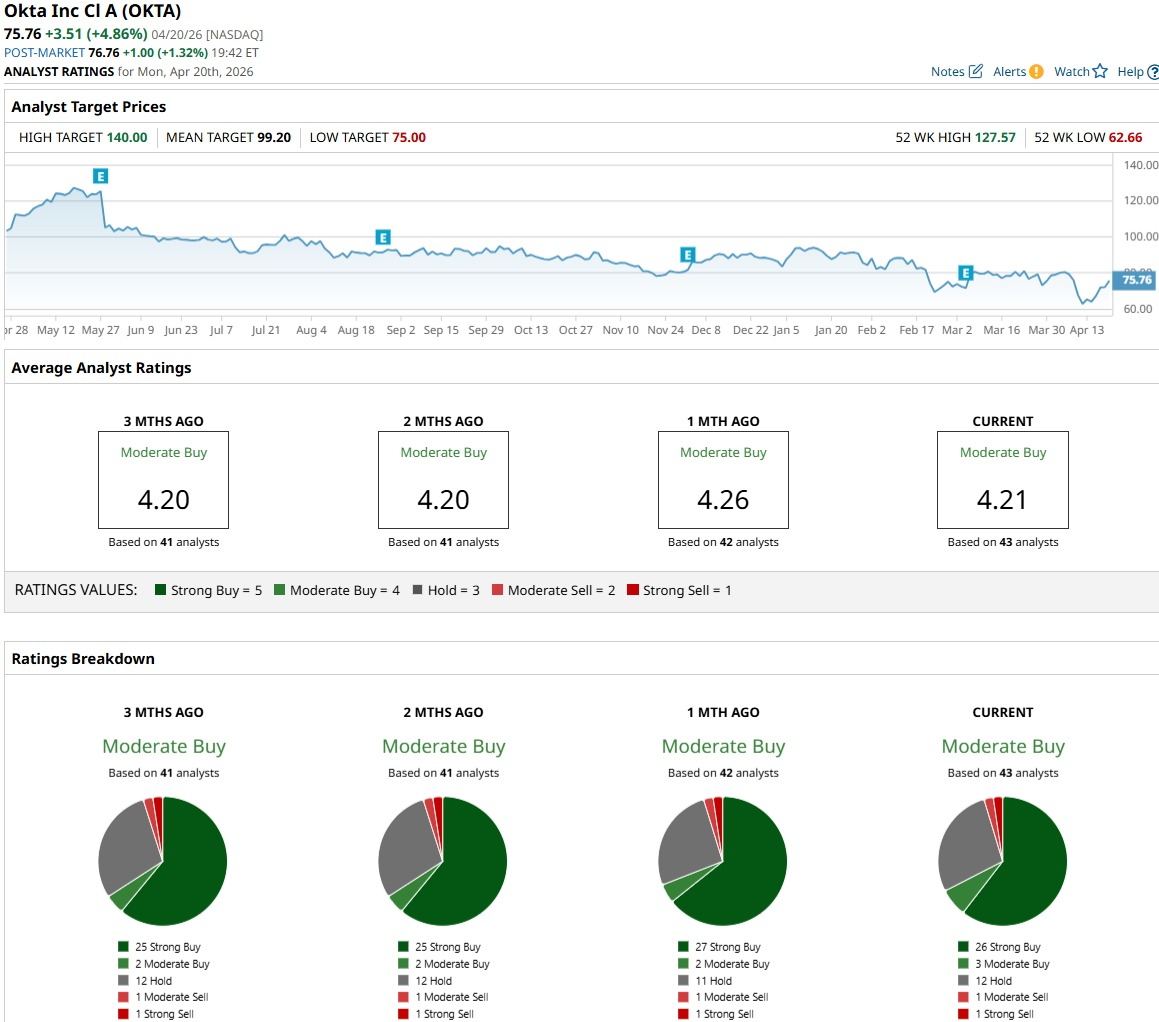

Raymond James just turned more positive on Okta (OKTA), upgrading the stock to “Outperform” on April 16 and setting an $85 price target. Barclays followed closely behind on April 20, upgrading OKTA stock to “Overweight” with a $90 price target. The move comes as the broader software group bounces back from last year’s “SaaS‑pocalypse,” with the U.S. Software & Computer Services Index ($DSSV) up more than 36% over the past 52 weeks, even though many names are still well below their highs.

The “SaaS‑pocalypse” theme makes a straightforward point. Software has been treated like a broken business, but what is really happening is a harsh reset. This reset puts identity and security tools in the likely “survivor” bucket because they are built into how companies manage access and protect sensitive data as AI agents spread and push digital risk higher. Identity and access management company Okta now sits in the middle of that story, as traders sort out which software names deserve a fresh look and which still need more time.

With that in mind, and with analysts calling for upside, the key question is simple. Is Okta coming out of the selloff? Or is it just another name that bounced too far, too fast? Let’s take a closer look.

Okta's Performance and Valuation Snapshot

Based in San Francisco, California, Okta is an identity and access management company that helps organizations secure and manage digital identities across apps, devices, and even AI agents as they move deeper into the cloud.

OKTA stock currently trades near $78, down 9% year-to-date (YTD) and down by 15% over the past 52 weeks. That said, shares have shown signs of life recently, surging roughly 22% in the five days following Raymond James’ upgrade

Okta is valued at about $13.4 billion by market capitalizationn and trades at a trailing price-to-earnings (P/E) ratio of 45.4 times versus a sector median of 34.1 times, with a P/E-to-growth (PEG) ratio of 2.8 times against the sector median of 1.46 times. So, the market is clearly paying up for earnings growth that is expected to strengthen.

The latest earnings report, released in early March for the quarter ending January 2026, showed sales of $761 million, up 11% year-over-year (YOY) and almost 3% sequentially. Net income climbed to $63 million, a 46% sequential jump showing the move toward stronger profitability.

This update also came with a big earnings surprise, as EPS landed at $0.43 versus a $0.30 consensus, a 43% beat that signaled the company can still deliver when execution matches plans. That confidence shows up in capital allocation, too, with a $1 billion share repurchase program now in place.

It was not just the income statement doing the talking, either. Operating cash flow reached $884 million, up 41% sequentially. Net cash flow also rose to $449 million, up 90% from the prior quarter, showing that profits are turning into real cash and not just accounting gains.

The full‑year fiscal 2026 numbers rounded out the story with profit of $235 million, or $1.31 per share, on revenue of $2.92 billion. That helps explain why an “Outperform” rating and a bullish call on future gains now look more grounded than hopeful.

Okta Expands Identity Security Footprint

Okta has been lining up clear growth drivers. The firm recently launched a new blueprint for the “secure agentic enterprise” built to help companies manage and protect both human users and AI‑driven agents on a single identity platform. The logic is simple. As more automated agents take on everyday work, each one becomes an identity that has to be checked, monitored, and, if needed, switched off fast.

The company is also pushing its reach through visible partnerships. Okta recently expanded its relationship with the PGA of America to secure the digital identities of golf professionals worldwide, giving Okta a global, consumer-facing use case beyond the usual corporate IT setup. That sort of deal brings more users onto the platform and shows Okta can support large, spread‑out groups where both security and easy access matter.

There is a regional push underway, too. Okta has added data residency and stronger disaster recovery options in India, an important market where multinational and local firms face tight data and uptime rules. These features let customers keep sensitive identity data inside the country while still counting on Okta for strong availability and quick recovery when something goes wrong.

What Does Wall Street Think of OKTA Stock?

Okta’s near‑term earnings picture is a bit mixed. The next report is due May 26 for the quarter ending April 2026, and Wall Street is looking for EPS of $0.32. That would be down from $0.42 a year earlier, which works out to a roughly 24% YOY drop in earnings.

That short-term dip has not stopped some analysts from getting more positive on shares. Both Raymond James and Barclays recently turned bullish on OKTA stock, with the former upgrading to “Outperform” with an $85 price target and the latter upgrading to an “Overweight” rating and $90 target. These moves lean on a steady outlook for identity security, helped by ongoing AI and cloud adoption that should keep demand growing over time.

Looking at the wider picture, the consensus rating across 43 analysts is a “Moderate Buy.” The average price target is $99.33, implying roughly 27% potential upside from here.

Conclusion

At today’s price, Okta looks like a reasonable buy for investors who can live with some bumps while the AI and identity story plays out. The setup points more toward upside over the next few years rather than a major reset lower. Over the next year, the most realistic base case is that OKTA stock works its way closer to the $90 to $100 area as opposed to recent lows, which makes buying on pullbacks look more appealing than staying on the sidelines.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Alibaba%20by%20Photo%20Agency%20via%20Shutterstock.jpg)