The chaos continues this year after ceasefire talks between the U.S. and Iran have effectively stalled, raising fears of a renewed escalation in the Middle East. At the same time, the U.S. has imposed a naval blockade on Iran, disrupting global oil flows and intensifying geopolitical risk. In times like these, dividend stocks become particularly attractive to investors that offer steady income even when markets swing wildly. Here are three such compelling dividend stocks for income-focused investors looking for both stability and upside.

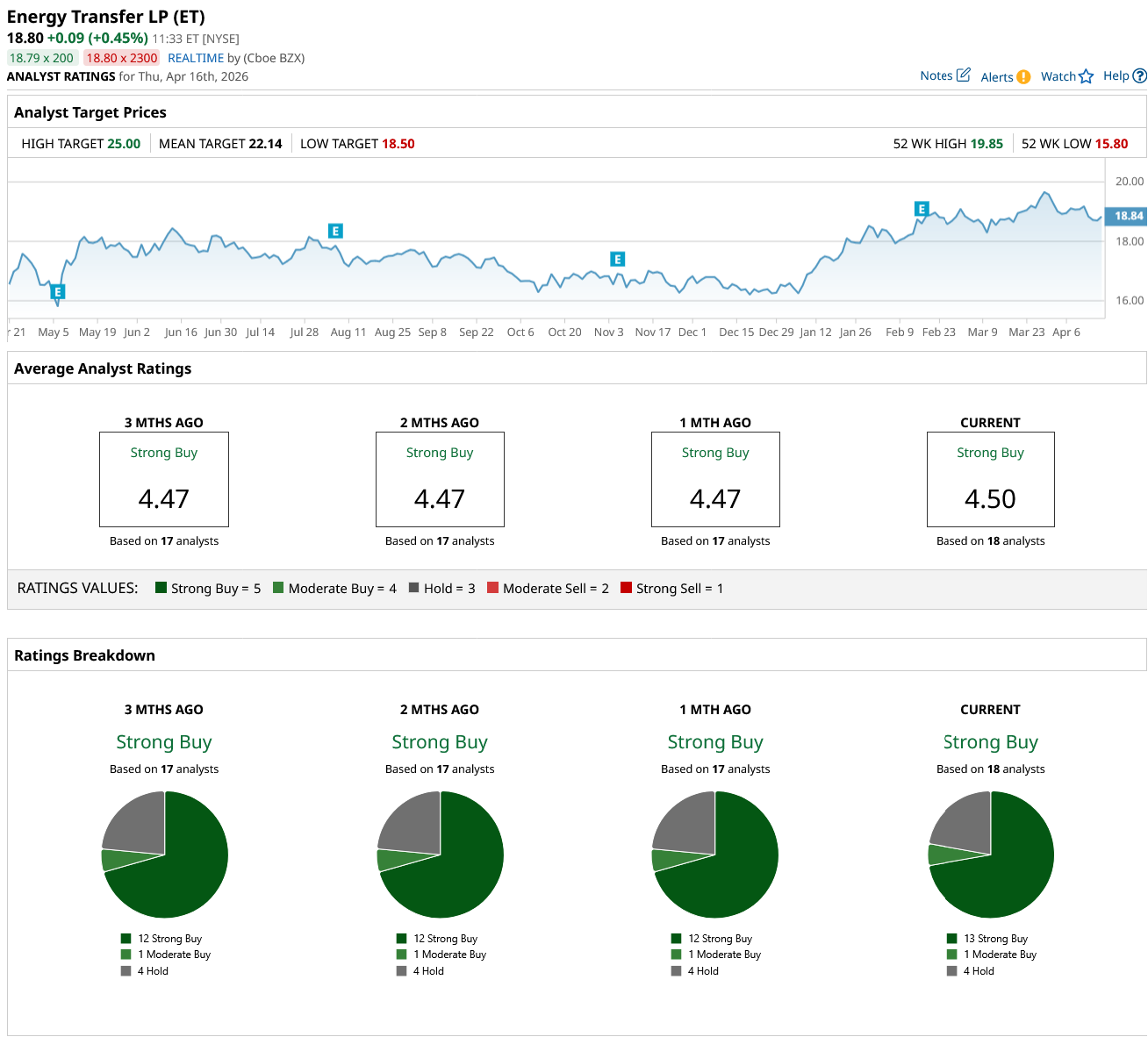

Dividend Stock #1: Energy Transfer (ET)

Dividend Yield: 7.1%

Energy Transfer (ET) stands out as a classic high-yield energy infrastructure play, benefiting directly from rising global energy demand and geopolitical instability. Valued at $64.4 billion, Energy Transfer is one of the largest midstream energy companies in the U.S. The company is not involved in drilling operations. But it operates in the middle of the energy supply chain, which is moving, storing, and exporting energy, such as natural gas, crude oil, natural gas liquids, and refined products. It is less dependent on oil prices than drilling companies and earns a steady, fee-based income. This keeps its cash flows more stable and predictable, allowing it to pay consistent dividends.

Energy Transfer pays a forward yield of 7.1%, higher than the market average, making it very attractive for income-focused investors. Besides yield, the other key criterion when choosing a good dividend stock is the payout ratio, which tells you how much of a company’s earnings it distributes as dividends. This helps determine whether dividends are sustainable. Energy Transfer’s payout ratio of 103% may look alarming at first glance. However, as a midstream MLP, it relies on distributable cash flow (DCF) to support its dividend rather than accounting earnings. In the fourth quarter, its DCF increased by 3% year-over-year (YoY) to $2.04 billion. The company announced a 3% increase in its quarterly cash distribution (dividends).

Overall, Wall Street says ET stock is a “Strong Buy.” Of the 18 analysts covering the stock, 13 rate it a “Strong Buy,” one rates it as a “Moderate Buy,” and four say it is a “Hold.”

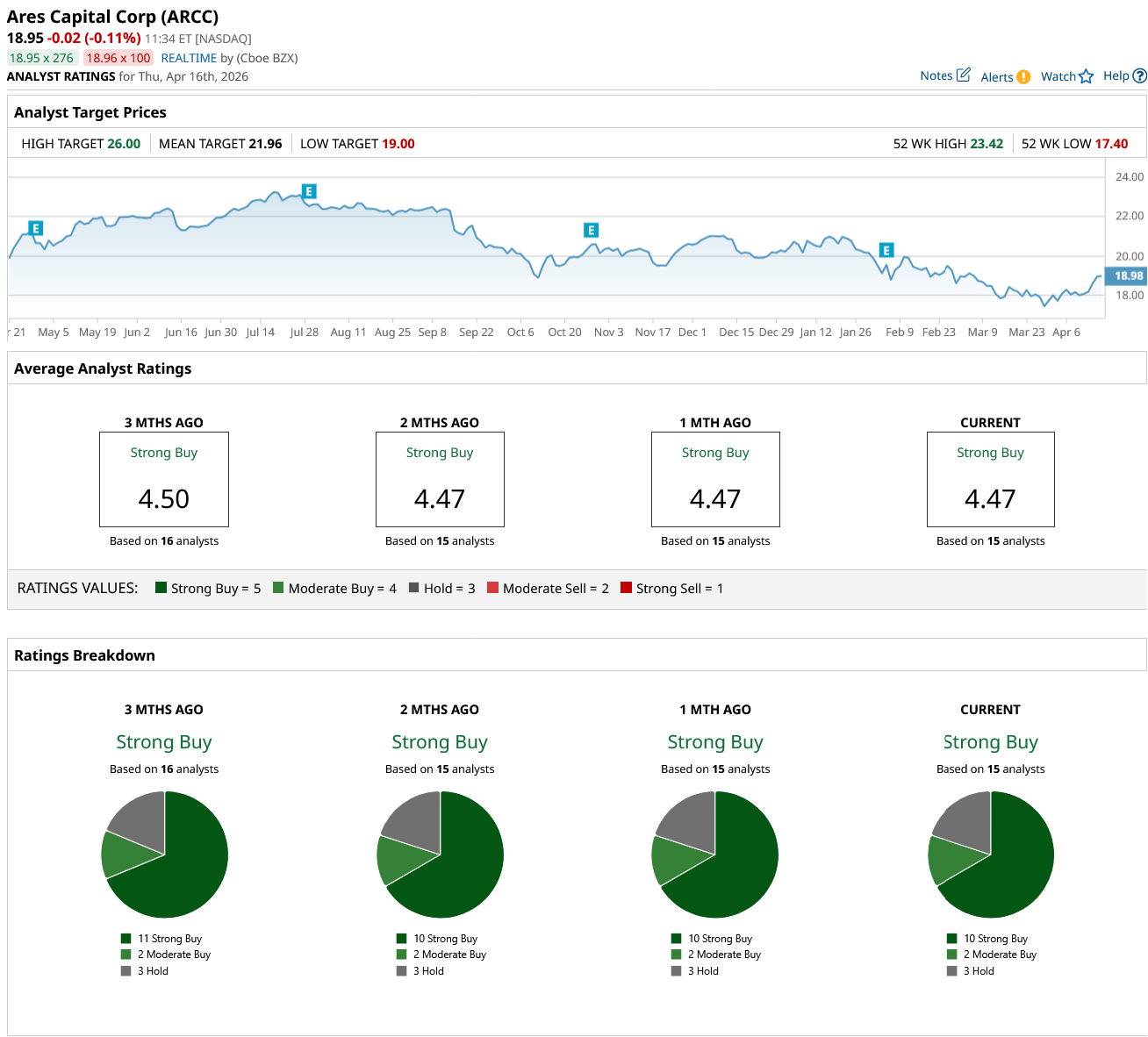

Dividend Stock #2: Ares Capital (ARCC)

Dividend Yield: 10.5%

Ares Capital (ARCC) offers one of the most attractive yields in the market today, with a dividend yield of about 10.5%. Valued at $13.6 billion, Ares Capital is a leading Business Development Company (BDC) that provides financing to middle-market businesses. In other words, it is a specialized lender and investor that earns money by issuing loans to companies, structuring private credit deals, and occasionally taking equity stakes in businesses. This business model earns steady interest income, which funds the dividends.

While its payout ratio also seems high at 97%, as a BDC, it must distribute at least 90% of its income to maintain tax advantages. That means Ares Capital is designed to operate with a high payout ratio. With rising interest rates and floating-rate loans, Ares continues to generate strong income, making its dividend relatively secure even in uncertain markets.

Overall, Wall Street says ARCC stock is a “Strong Buy.” Of the 15 analysts covering the stock, 10 rate it a “Strong Buy,” two rate it as a “Moderate Buy,” and three rate it a “Hold.”

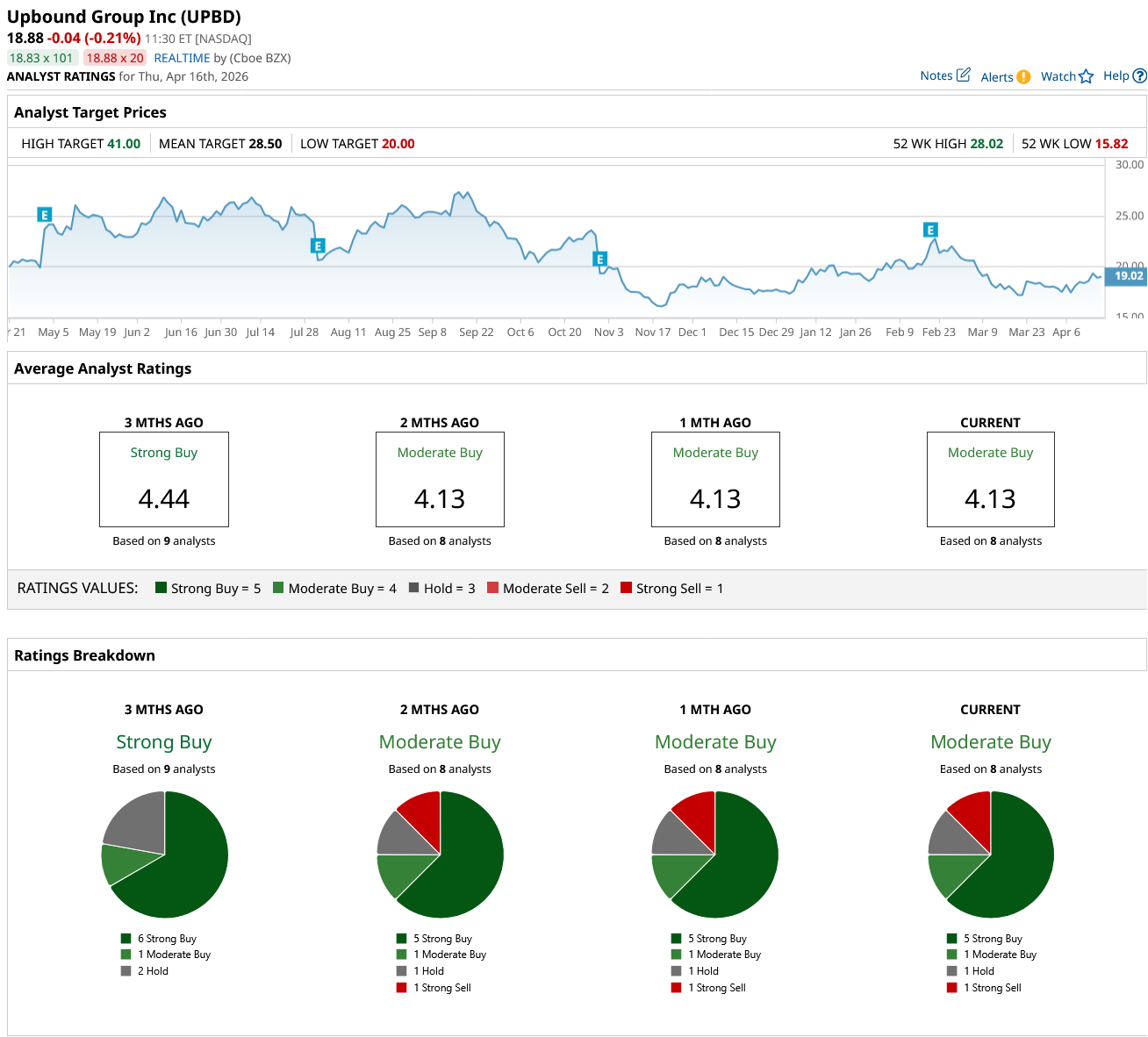

Dividend Stock #3: Upbound Group (UPBD)

Dividend Yield: 8.4%

Valued at $1.1 billion, Upbound Group (UPBD) is a consumer finance and retail company that helps those who do not qualify for traditional credit. It operates in the rent-to-own and consumer finance space, providing flexible payment solutions for customers. It generates revenue through payment plans, fees and service charges, and retail partnerships.

As traditional credit tightens and consumers face financial pressure, demand for alternative financing solutions often increases. Its business model generates recurring payments from customers, leading to strong cash flows, allowing it to maintain its dividend yield of 8.4%. But the business also carries some risks; when customers struggle to make payments, earnings can be impacted.

In 2025, Upbound’s adjusted earnings increased by 7.8% to $4.1 per share. Analysts expect the company’s earnings to increase by 1.6% in 2026, followed by 15.3% in 2027. Its payout ratio of 37% remains modest, meaning that dividends are sustainable while still allowing the company to reinvest profits.

Overall, Wall Street says UPBD stock is a “Moderate Buy.” Of the eight analysts covering the stock, five rate it a “Strong Buy,” one rates it as a “Moderate Buy,” one says it is a “Hold,” and one recommends a “Strong Sell.”

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Apple%20Inc%20logo%20on%20Apple%20store-by%20PhillDanze%20via%20iStock.jpg)

/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

/The%20Shopify%20logo%20on%20a%20smartphone%20screen%20by%20IB%20Photography%20%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)