/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)

Intel Corporation (INTC) is a global semiconductor titan undergoing a historic transformation. The company is pivoting from being primarily a chip designer to becoming a world-class systems foundry. Intel is executing its "IDM 2.0" strategy, aiming to regain process leadership through its Intel 18A and 14A nodes. By integrating advanced packaging like EMIB and Foveros with its ubiquitous x86 architecture, Intel powers approximately 70% of the world's PCs. Its mission is to enable "AI Everywhere," spanning from the high-performance data center to the edge, while building a resilient, U.S.-based, leading-edge manufacturing ecosystem.

Founded in 1968. The company is based in Santa Clara, California.

Intel Stock Pops

Intel stock has shown significant signs of recovery, and after a period of heavy capital investment, it is currently trading near its 52-week high. INTC stock is up nearly 40% in the past month and about 72% year-to-date (YTD). The market has begun to reward Intel's progress in its foundry roadmap and the successful launch of its AI-powered Core Ultra processors. While volatility remains due to the massive R&D spending required for its 5-nodes-in-4-years goal, investors are increasingly optimistic about Intel’s ability to capture a larger share of the growing AI PC and sovereign foundry markets.

In comparison to the S&P 500 Information Technology Index ($SRIT), Intel has been a relative laggard over the long term but has recently begun to narrow the gap. While the broader IT index, dominated by pure-play AI hardware and software giants, saw double-digit gains in early 2026, Intel’s performance was moderated by its heavy manufacturing overhead.

However, as the index's growth becomes more concentrated in "AI builders," Intel’s unique position as the only U.S. firm combining leading-edge design with domestic high-volume manufacturing provides a defensive "strategic" premium that many of its index peers lack during periods of geopolitical trade tension.

Intel's Results Shine

Intel concluded fiscal 2025 with a strong fourth quarter, reporting revenue of $13.7 billion, which exceeded guidance despite industry-wide supply constraints. The company achieved a non-GAAP diluted EPS of $0.15, nearly double its $0.08 forecast.

This performance was driven by a 9% year-over-year (YoY) surge in the Data Center and AI (DCAI) segment, which reached $4.7 billion. For the full year, Intel reported $52.9 billion in total revenue and generated $9.7 billion in cash from operations. Notably, the Intel Foundry segment saw a 4% revenue increase, reflecting a shift toward advanced EUV wafers and the early ramp of the Intel 18A process node.

Looking ahead, Intel has provided a cautious but strategic outlook for Q1 2026, forecasting revenue between $11.7 billion and $12.7 billion. While the company expects a seasonal dip and breakeven non-GAAP EPS in the first quarter, management anticipates that factory network improvements will resolve supply bottlenecks starting in Q2. Intel is targeting $16 billion in operating expenses for 2026 and expects to generate positive adjusted free cash flow for the full year.

Up Over 70% YTD, Should You Buy INTC Stock?

Intel has become one of the market's hottest names, surging over 53% across a record-breaking nine-day rally that added $100 billion in market value. This massive momentum, which saw shares jump nearly 40% in the past month, was ignited by the strategic $14.2 billion repurchase of Apollo’s stake in its Ireland fab. Investors are increasingly viewing this move as a "pivot from survival to expansion."

Further catalysts, including a high-profile partnership with Elon Musk’s Terafab and Google’s (GOOG) (GOOGL) commitment to future Xeon processors, have solidified the narrative that Intel is regaining its footing as a critical AI infrastructure provider.

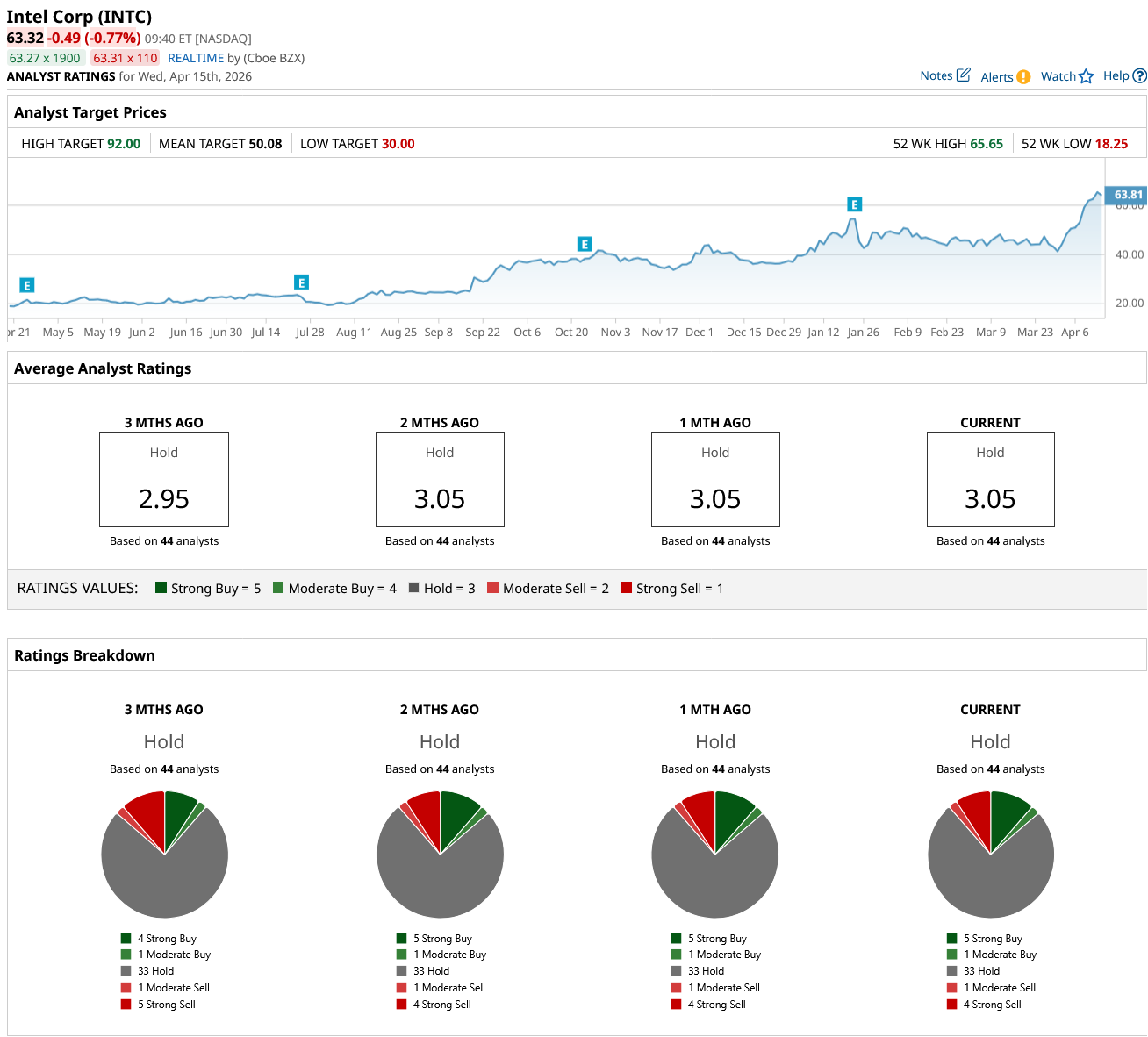

While Intel’s recent 40% surge has electrified the market, the professional analyst community remains notably cautious. INTC stock currently carries a consensus "Hold" rating based on 44 evaluations, consisting of five "Strong Buy," one "Moderate Buy," 33 "Hold," one "Moderate Sell," and four "Strong Sell" ratings. With a mean price target of $48.65, the stock technically faces a 22% downside from its current elevated market price.

For investors, the decision rests on a trade-off: betting on the high-momentum "Foundry" turnaround and Elon Musk-led catalysts versus the reality that the stock has potentially overextended its current fundamental valuation.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

/Space/Cargo%20spacecraft%20in%20low-Earth%20orbit%20by%20Paopano%20via%20Shutterstock.jpg)