/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

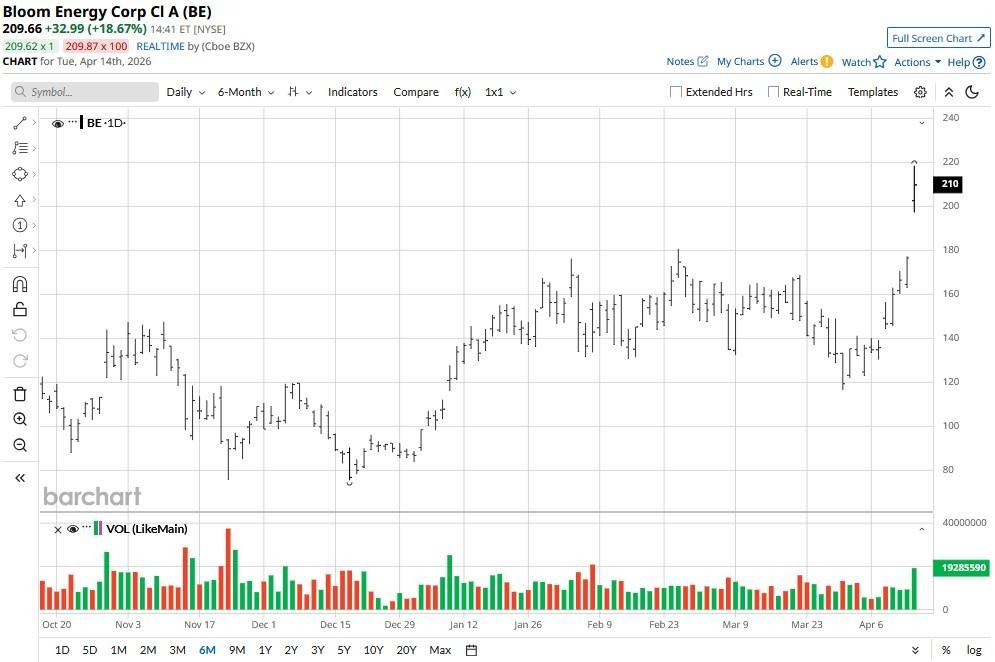

Bloom Energy (BE) shares are rallying on April 14 after the clean energy firm announced a massive expansion of its partnership with Austin-headquartered Oracle (ORCL).

As investors cheered BE’s new deal aimed at supplying up to 2.8 gigawatts of fuel cell energy for AI data centers, its relative strength (RSI) rose into the mid-70s, indicating overbought conditions.

Bloom Energy stock has been a major outperformer in 2026, now up more than 100% year-to-date.

Why the Oracle Deal Is Bullish for Bloom Energy Stock

The expanded agreement with Oracle is a game-changer for BE shares as it significantly boosts revenue visibility through 2027.

ORCL’s announcement signals enterprise-grade confidence in the reliability, uptime, and scalability of Bloom’s solid-oxide fuel cells, validating the technology as a credible solution for AI-era power demand.

Other than deepening BE’s recurring service revenue base, the deal strengthens its balance-of-plan economics and positions the company as a strategic supplier to hyperscale-adjacent workloads.

Analysts at Jefferies noted that it likely adds $3.8 billion to Bloom’s backlog, potentially leaving it sold out of capacity for the next two years.

In short, the transaction evolves Bloom Energy from a niche clean-tech name into a mission-critical infrastructure partner.

Why BE Shares May Retreat in the Near-Term

As part of the expanded collaboration, Oracle has received warrants to purchase 3.5 million Bloom Energy shares at about $113 each.

Since these warrants are deep "in the money” already, with BE trading at north of $210, the firm’s shareholders are in for massive dilution if ORCL chooses to lock in gains in the days ahead.

Put it together with the COO and CLO unloading millions in company shares last month, and BE immediately starts to look rather unattractive at a super-stretched 170x forward earnings multiple.

Meanwhile, the risk of “mean reversion” and the absence of a dividend yield also warrant keeping on the sidelines in this clean energy stock.

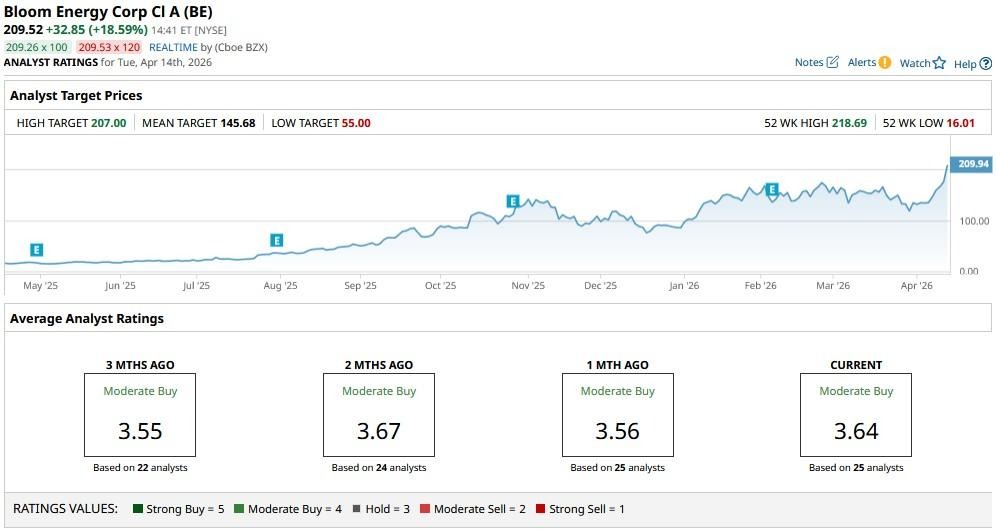

Wall Street Remains Cautious on Bloom Energy

Wall Street seems to agree with what the RSI is indicating currently: Bloom Energy’s year-to-date rally has gone a bit too far, and the company may, therefore, see a correction in the near term.

While the consensus rating on BE stock sits at a “Moderate Buy,” the mean price target of about $145 signals potential downside of more than 30% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)