/Meta%20Platforms%20by%20Primakov%20via%20Shutterstock.jpg)

Meta Platforms (META) is on track to surpass Alphabet’s (GOOG) (GOOGL) Google in digital advertising revenue this year, according to projections from market research firm eMarketer. If realized, the shift would mark a notable change in the digital advertising landscape, with Meta overtaking the long-dominant search engine leader.

The parent company of Facebook and Instagram is expected to generate $243.46 billion in global net advertising revenue in 2026, exceeding Google’s projected $239.54 billion. The forecast reflects Meta’s strong momentum in digital advertising, driven largely by the scale and engagement of its social media platforms.

Meta’s advertising business has shown significant growth. In 2025, the company reported $196.18 billion in advertising revenue, a 22% increase from the previous year. Continued expansion in daily active users and rising engagement across Meta’s family of apps are expected to support further growth in advertising revenue in the coming quarters.

However, investor sentiment toward the stock has been tempered by the company’s rising investment in artificial intelligence (AI) infrastructure. Higher spending has raised concerns about near-term profitability amid uncertainty over returns, potentially limiting upside in META stock despite the company’s strong advertising performance.

With Meta scheduled to report its first-quarter earnings on April 29, signals on advertising demand, user engagement trends, and the pace of AI-related spending will likely shape the stock’s trajectory.

Meta Q1 Outlook: Strong Revenue Momentum With Moderating Earnings Growth

Meta entered 2026 with solid operating momentum, supported by steady user growth across its Family of Apps ecosystem. This expansion in engagement is expected to translate into stronger advertising performance during the first quarter.

In the previous quarter, Meta’s Family of Apps generated $58.9 billion in revenue, representing a 26% increase year-over-year (YoY). Advertising accounted for the majority of that total, reaching $58.1 billion and growing 24% YoY.

That momentum is expected to extend into the first quarter. Management has guided for total revenue in the range of $53.5 billion to $56.5 billion. At the midpoint of $55 billion, this outlook implies YoY growth of roughly 30%. Advertising could again remain the primary driver of revenue expansion, supported by higher user engagement and continued advertiser demand across Meta’s platforms.

Notably, ongoing user growth and deeper engagement, particularly with short-form video, are supporting this trend. Reels continues to be a major area of expansion, with time spent watching Instagram Reels in the U.S. increasing more than 30% YoY in the fourth quarter. At the same time, enhancements to Meta’s recommendation systems are expected to improve content discovery and ad targeting as increasing volumes of AI-generated content circulate through the company’s ecosystem.

Advertising pricing trends are also expected to support revenue growth in Q1. Average ad prices are likely to increase compared with the previous year, reflecting strong advertiser demand and improved performance metrics. Overall, higher impression volumes and increased pricing position Meta for another quarter of solid top-line growth.

Despite strong revenue expectations, earnings growth is projected to be more moderate. Wall Street analysts currently forecast earnings of $6.69 per share, representing a 4% YoY increase. Historically, however, Meta has consistently exceeded analyst expectations, beating consensus earnings estimates in each of the past four quarters, including an 8.1% upside surprise in the fourth quarter.

Is META Stock a Buy?

Meta’s ability to surpass Google in digital ad revenue highlights the strength of its ecosystem built around its core social media platforms, including Facebook, Instagram, and WhatsApp. Rising user engagement, expanding daily active users, and strong adoption of formats such as Instagram Reels are strengthening the company’s ability to monetize its user base. These dynamics suggest that Meta’s advertising engine remains strong and capable of sustaining double-digit revenue growth in the near term.

However, higher capital expenditure and pressure on near-term margins and earnings could limit the upside potential.

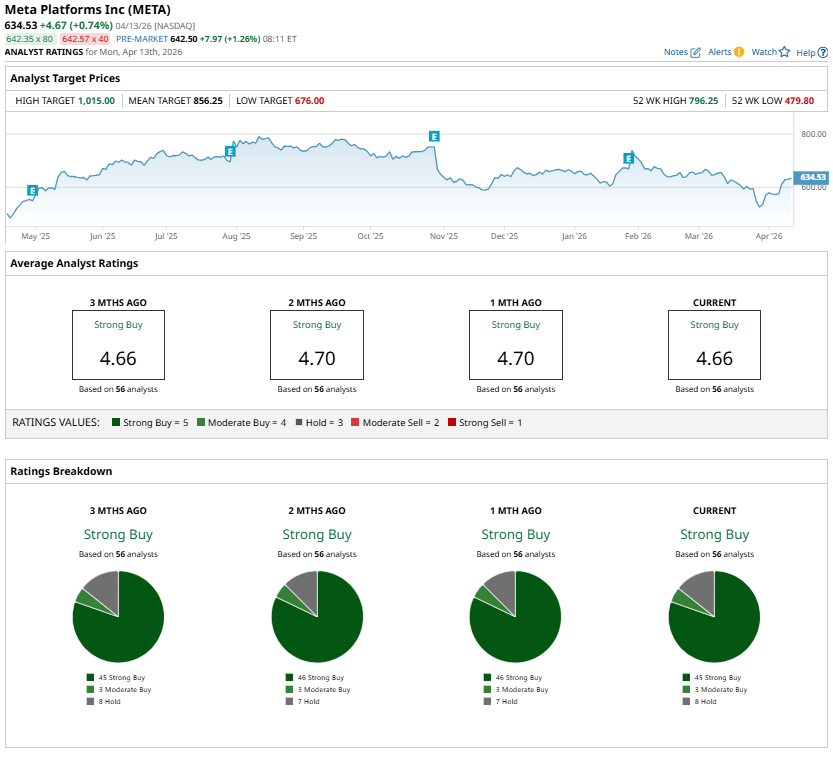

Thus, investors with a long-term view could consider buying META stock. In the short term, Meta’s forward price-to-earnings ratio of 21.1 indicates that most of the positives are priced in. Analysts are bullish and maintain a “Strong Buy” consensus rating on META stock ahead of Q1 earnings.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)