If you read the last minutes of the meetings of the Federal Reserve, you get the impression that the central bank is ready anew to put on armor and go on a crusade against inflation. Officials seriously argue that inflation turned out to be too “sticky” and are starting to whisper about the frightening possibility of another rate hike.

Markets tense up, algorithms prepare to sell. But here is a nuance: if we put aside the microphones and look at the dry numbers of the balance sheet of the Fed, a completely different, paradoxical picture emerges. The Fed says one thing, but does the exact opposite.

Hidden Easing: What Does the Balance Sheet Show?

While the rhetoric of the regulator becomes ever more hawkish, its balance sheet began to demonstrate a highly interesting dynamic.

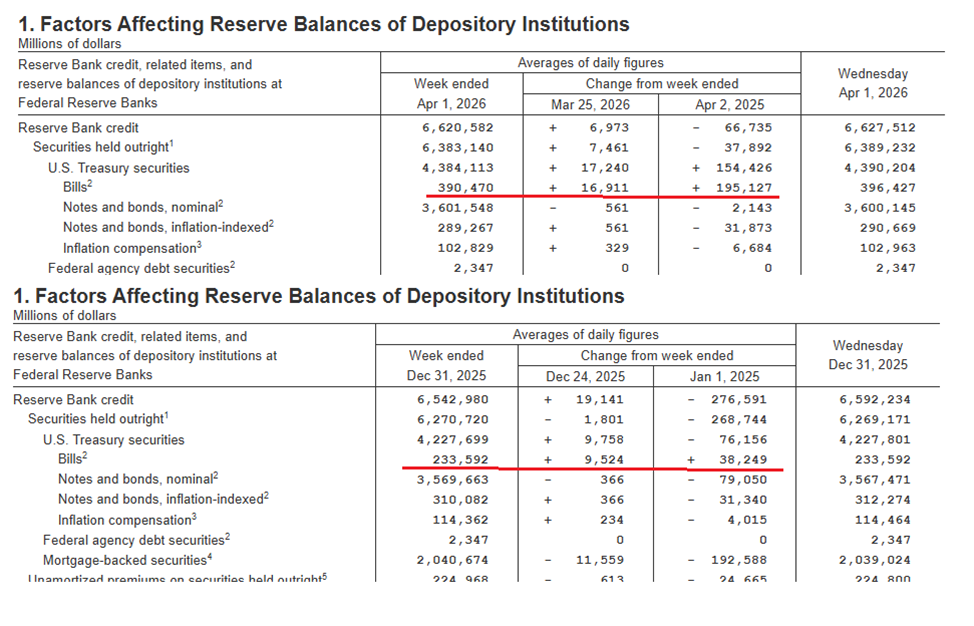

According to the official data of the weekly report H.41, the position of the Fed on short-term treasury bills (Bills) over the last three months sharply grew. We are talking about the infusion into the system of more than $150 billion of fresh liquidity. An amazing dissonance emerges: members of the Fed take the podium and threaten to tighten monetary policy, but at the same time renew hidden quantitative easing (QE), buying out short-term debt and increasing the general volume of dollar liquidity in the system.

To understand why the Fed did this, we need to rewind time back to the December meeting.

The Effect of the Vacuum: Why It Was Necessary to Turn on the Press

At the end of the past year, the U.S. financial system faced a serious threat: a severe deficit of liquidity. The American government itself was the main culprit behind this drought. The U.S. budget deficit is growing at a colossal pace. To finance its expenses, the Treasury is forced to release mountains of new debt securities. This process worked like a giant financial vacuum: The Treasury began to rapidly suck out free cash from the economy. A real threat arose that the government simply will take away all money from the market, leaving the banking sector and corporations starved of liquidity.

That is exactly why in December, the Fed was forced to interfere. To level the effect of this “vacuum” and prevent a paralysis of the financial system, the regulator announced the beginning of a program to buy out short-term bonds. The goal was noble: to knock down the tension in the money market and give the system the very liquidity which the Treasury was ruthlessly devouring. But this action drove the Fed to fear its own shadow.

The Fed’s Afraid of Its Own Shadow

I think that the Fed perfectly understands what it does. It realizes that, in essence, buying out bills is the printing of new money. And although the growth of the balance sheet by $100 or $200 billion seems like a drop in the bucket compared to the general base of $6.5 trillion, this is all the same new money, injected into the system. And herein lies the riddle of the central bank’s current behavior. The Fed is mortally afraid of its own actions.

The logic of the regulator right now is operating in this mode: with one foot it is forced to press on the gas pedal, giving much-needed liquidity. With the other foot, it shakes in fear, worried that it will trigger a new round of inflation.

That second foot convulsively beats on the brake pedal via harsh rhetoric. The Fed attempts to manage expectations and decrease the velocity of money circulation. It increases the general level of “water” in the pool, but attempts to freeze its flow through threatening statements so that primary money does not spill over into explosive consumer growth.

All this inflationary panic in the “minutes” — this is not so much a reaction to real prices, as an attempt to compensate for the effect of its own hidden printing press.

Stop the Fear: Inflation Is the New Norm

The problem is that this fear is excessively exaggerated. The world has changed.

The Fed simply needs to accept that inflation on the level of 3%-4% — this is now not a catastrophe, but a new macroeconomic norm. Having accepted this fact, it could calmly release liquidity and cease to choke markets with threats of high rates. Its main fear is that the increase of the money base inevitably will lead to an uncontrollable growth of the broad money mass (M2) and hyperinflation. But it overlooks the most important structural barrier, which it helped erect.

As I analyzed in detail earlier, the modern banking system is reliably shackled by the norms of Basel III. These harsh rules of reserving work like a powerful concrete dam. Basel III is the exact reason why even when the balance sheet of the Fed inflated to an unbelievable $9 trillion, no hyperinflation in the style of the Weimar Republic occurred, and the aggregate M2 did not skyrocket. The Fed is already protected from the worst scenarios. It is time for the regulator to stop being afraid of its own shadow, stop this exhausting verbal intervention, and allow the economy to breathe in conditions of the new normal.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)