On March 30, 2026, JPMorgan Chase (JPM), the biggest bank in the U.S., introduced the American Dream Initiative (ADI), a long-term plan aimed at creating more economic opportunity in communities across the country. The market liked it right away, with JPM shares rising 3.6% in afternoon trading.

The move follows the bank’s $1.5 trillion Security and Resiliency Initiative, launched in Oct. 2025, a 10-year effort focused on sectors tied to U.S. economic strength, including supply chains, advanced manufacturing, defense, energy, and frontier technology. In that sense, the ADI looks like the community-facing part of a much bigger plan.

Furthermore, JPMorgan is heading into this with earnings coming up. The bank is due to report Q1 2026 results on Apr. 14, and analysts expect earnings of $5.46 a share, up 7.69% from a year earlier. As Jamie Dimon stated, “The American Dream is alive, but it's slipping out of reach for too many people.” The ADI is built around six areas: small business growth, housing affordability, financial health and wealth, jobs and skills, healthcare, and local institutions.

So the real question is simple: with $1.5 trillion already tied to America’s economic strength and a new community push now added on top, is JPMorgan building something that can drive growth over time, or just selling a strong story? Let’s find out.

A Look at the Numbers

JPMorgan Chase's portfolio includes consumer banking, corporate lending, asset management, and capital markets. So it sits in the middle of almost every part of the financial system. Over the past 52 weeks, the stock is up 36.44%, but down 3.83% year-to-date (YTD).

Its shares are not cheap versus peers, trading at a forward P/E of 14.24 times compared with about 10.49 times for the sector, but that premium lines up with how the market views JPMorgan’s earnings strength and durability.

The income story is solid too. The stock yields 1.92% annually, with a quarterly dividend of $1.50 paid on Apr. 6, a forward payout ratio of 26.26%, and 15 straight years of dividend increases.

On the earnings side, Q4 CY2025 revenue came in at $46.77 billion with adjusted EPS of $5.23, a 7.7% beat, supported by $25 billion in net interest income and a tangible book value of $107.56 per share, up 11.8% year-over-year (YOY). With a market cap of $831 billion, it is still the reference point for profit and balance-sheet strength in U.S. banking.

The Fundamentals of JPMorgan’s Growth Play

Through Chase, JPMorgan plans to open more than 160 new branches across over 30 states in 2026 and renovate nearly 600 existing locations, putting real money behind the idea of making basic banking easier to reach.

That follows a plan laid out in 2024 to open more than 500 branches, update 1,700 locations, and hire 3,500 people over three years, with a clear focus on low-to-moderate income and rural areas, as well as faster-growing regions in the Northeast, Southeast, Heartland, and Southwest.

It is also working on ways to keep customers more deeply tied into its ecosystem. Chase and Disney (DIS) rolled out the Disney Inspire Visa Card, a new card with a $149 annual fee that sits alongside the existing Disney cards. The card offers 200 Disney Rewards Dollars after $2,000 in spending per anniversary year on U.S. Disney Resort stays and Disney Cruise Line bookings, a $100 statement credit after $200 in spending per anniversary year on U.S. Disney theme park tickets, and up to $120 a year in credits on Disney+, Hulu, and Plus.ESPN.com.

On investing, J.P. Morgan Asset Management launched the JPMorgan International Dynamic ETF (JIDE) on NYSE Arca. It is built to give U.S. investors exposure to the $2 trillion Foreign Large Blend space, holding leading companies in developed markets outside North America, including Australia, Israel, Japan, New Zealand, Singapore, Hong Kong, the U.K., and Western Europe, with a mix of large- and mid-cap names and no strict style or sector limits.

How Analysts See the Road Ahead

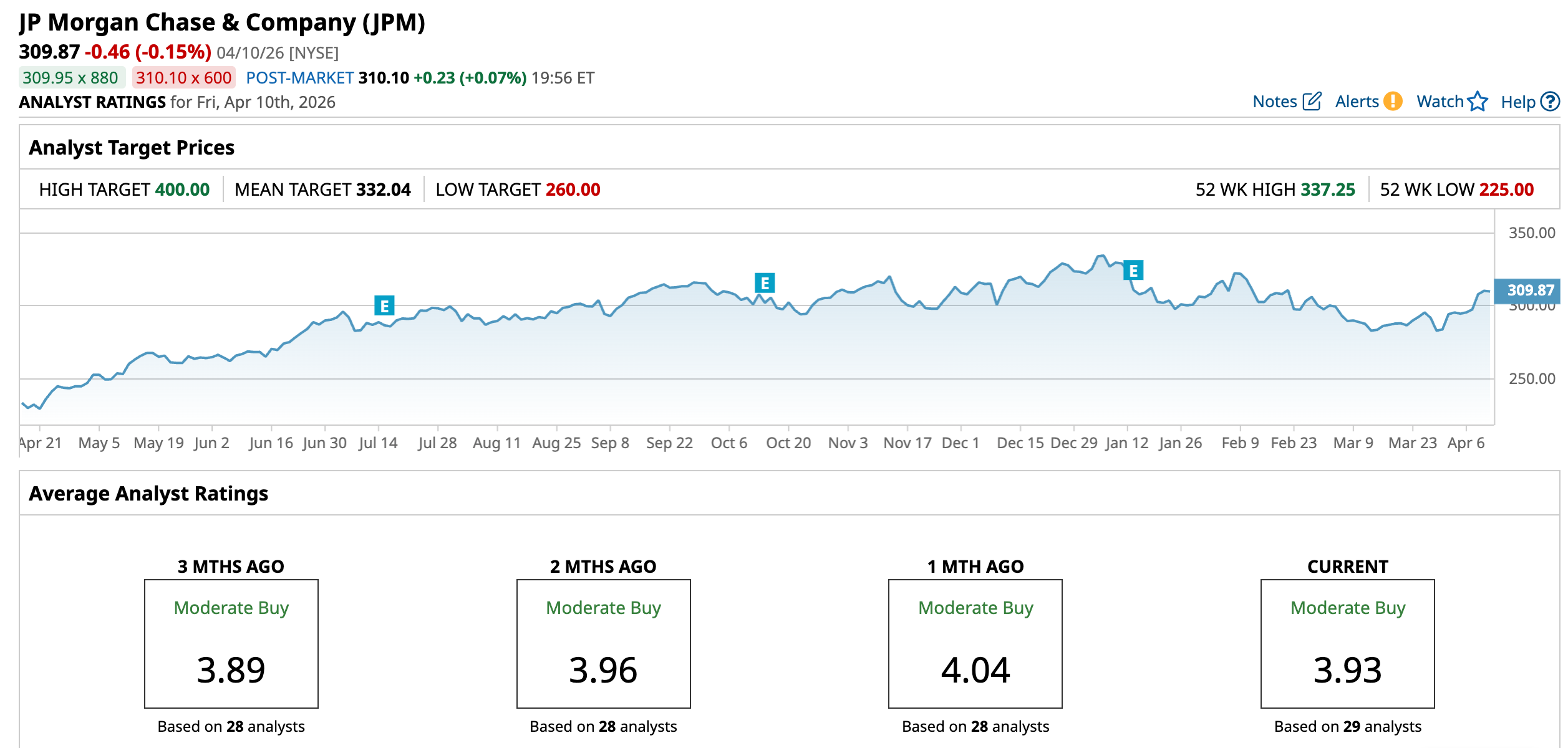

Analysts still see steady growth ahead for JPMorgan. For the March 2026 quarter, the average earnings estimate is $5.46 per share, up from $5.07 a year ago, which points to 7.69% growth. For the June quarter, the estimate is $5.33 versus $4.96 last year, or 7.46% growth. Looking further out, Wall Street expects JPMorgan to earn $21.79 per share in 2026 and $23.34 in 2027, up from $20.34 and $21.79, respectively.

That outlook helps explain why in early February 2026, Baird’s David George upgraded JPMorgan from Underperform to Neutral, though he kept his $280 price target in place. His reason was simple: the bank has a very strong capital position.

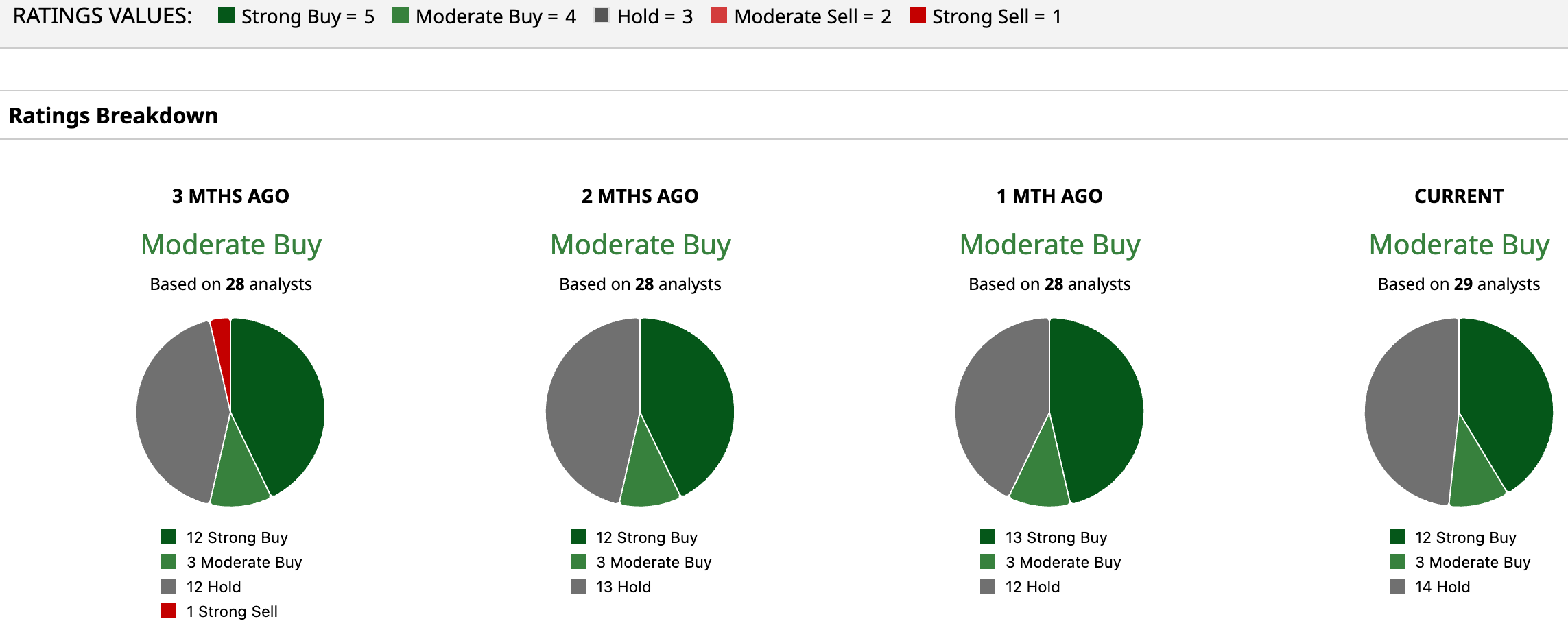

The bigger Wall Street view is still fairly positive. All 29 analysts surveyed rate the stock a consensus Moderate Buy, and the average price target of $332.04 suggests about 7.15% upside from current levels.

Conclusion

At this point, this looks like more than just a PR move. JPMorgan has the size, profits, and financial strength to back a plan like this, and the market’s reaction shows investors are taking it seriously. My view is that the stock is more likely to keep moving up gradually than jump sharply, because the story here is about steady execution over time. If the bank keeps delivering strong earnings, that should help support the shares.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)