Popular artificial intelligence (AI) startup Anthropic announced Claude Mythos Preview, a newly advanced model with a limited rollout to a select group of companies as part of a new cybersecurity initiative called Project Glasswing. The Mythos AI model is adept at identifying security flaws in software, so the limited access is intended to prevent exploitation of this capability. Cybersecurity company CrowdStrike Holdings (CRWD) was chosen as a partner in this project.

Wedbush analysts have picked CrowdStrike as a top cybersecurity pick, noting that the company is keeping up with AI model advancements. As the pressure is expected to be lifted from the company’s shoulders, should you consider investing in the stock now?

About CrowdStrike Stock

CrowdStrike Holdings is a global cybersecurity company that operates a cloud-native platform designed to stop breaches across endpoints, cloud workloads, identities, and data. Its business is centered on the Falcon platform, which it sells mainly through subscription modules that combine threat detection, security monitoring, identity protection, log management, and automated response capabilities.

Headquartered in Austin, Texas with a market cap of $96.12 billion, CrowdStrike uses AI to help spot cyber threats quickly and respond faster. Its security platform watches for unusual activity, helps stop attacks, and reduces the work for security teams. In simple terms, AI makes CrowdStrike’s cybersecurity tools smarter and faster.

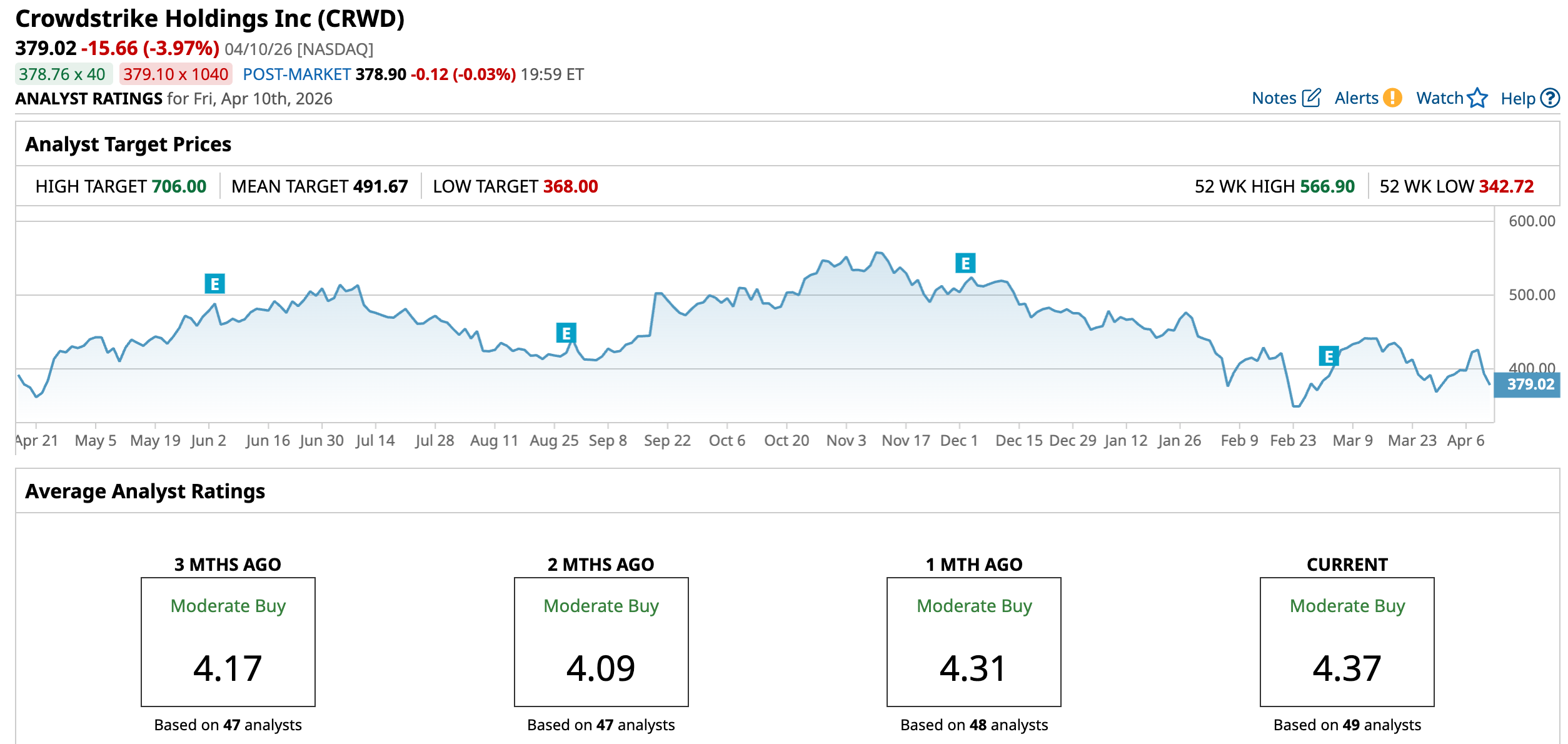

CrowdStrike’s stock has had a tepid time on Wall Street as investors have been balancing strong business growth against a still-rich valuation and periodic risk-off selling in software stocks. Over the past 52 weeks, the stock has gained 2.82%, but is down 19.14% year-to-date (YTD). It reached a 52-week low of $342.72 on Feb. 23, but is up 10.6% from that level.

On a forward-adjusted basis, CrowdStrike’s price-to-earnings (non-GAAP) ratio of 78.03 times is stretched compared to the industry average of 21.67 times.

CrowdStrike Q4 Earnings Showed Bottom Line Tailwinds

For the fourth quarter of fiscal 2026 (ended Jan. 31), CrowdStrike’s revenues increased 23.3% year-over-year (YOY) to $1.31 billion, which was slightly higher than the $1.30 billion that Wall Street analysts had expected. This was led by a 23.2% increase in subscription revenues to $1.24 billion.

The company’s annual recurring revenue (ARR) grew 24% YOY to $5.25 billion as of Jan. 31, of which a record $330.70 million was net new ARR added in the quarter. CrowdStrike achieved positive GAAP-based net income of $38.69 million, while non-GAAP net income reached a record $289.11 million. Its non-GAAP EPS was $1.12, up 38.3% YOY and above the $1.10 analysts had expected.

For fiscal 2027, its total revenue is expected to be in the $5.87 billion to $5.93 billion range, while its non-GAAP EPS is projected to be in the $4.78 to $4.90 range. CrowdStrike believes that the AI revolution represents a new, generational growth opportunity, and the company expects to scale to $20 billion in ending ARR in fiscal 2036.

Wall Street analysts expect CrowdStrike’s future earnings to skyrocket. For the current fiscal year, EPS is projected to surge to $1.01, followed by a 67.3% growth to $1.69 in the next fiscal year.

What Do Analysts Think About CrowdStrike’s Stock?

Last month, there was a slew of positive affirmations from Wall Street analysts on CrowdStrike’s stock. Wolfe Research analysts upgraded the stock to “Outperform” and set a $450 price target. As investors reassess the impact of AI on cybersecurity, especially as Anthropic potentially releases Mythos, Wolfe analyst Joshua Tilton predicts it could lead to a machine-speed cyberwar, thereby increasing demand for CrowdStrike’s offerings.

In the same month, analysts at RBC Capital reiterated an “Outperform” rating and a $550 price target. Following CrowdStrike’s fourth-quarter results, the firm’s analysts stated is positioned to benefit from increased customer spending on AI and to consolidate cybersecurity spending.

Morgan Stanley analysts also upgraded CrowdStrike’s stock from “Equal-Weight” to “Overweight” and raised the price target from $487 to $510. Analysts led by Meta Marshall said the company’s strong AI positioning, rising use of newer modules, and improving endpoint trends could support its long-term platform strategy, even though the stock may still look expensive.

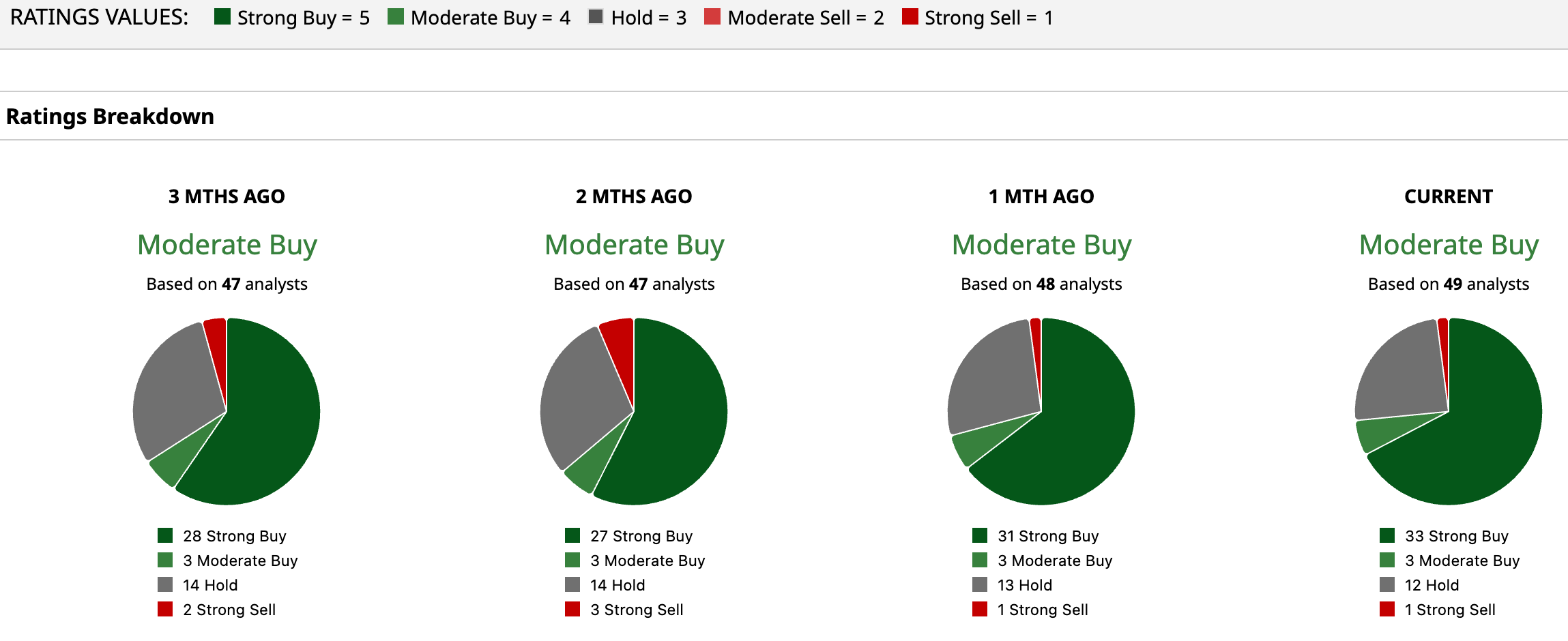

CrowdStrike Holdings is gaining some praise on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating. Of the 49 analysts rating the stock, a majority of 33 analysts have rated it a “Strong Buy,” three analysts suggest a “Moderate Buy,” while 12 analysts are playing it safe with a “Hold” rating, and one analyst gave a “Strong Sell” rating. The consensus price target of $491.67 represents a 29.7% upside from current levels. The Street-high price target of $706 indicates a 86.27% upside.

Key Takeaways

Cybersecurity companies like CrowdStrike, which have recognized the potential of AI, are poised to benefit from the wave of threats the technology can pose to digital infrastructure. Being chosen as an Anthropic partner might mark a step in that direction. In fact, Wedbush predicts that cybersecurity spending, which accounts for roughly 5% of IT budgets, will likely double over the next few years to 10% as AI use cases and broader technologies pose risks to many organizations. Therefore, CrowdStrike might be a buy now.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)