Howdy market watchers!

Did the week seem to fly by fast for you as well? After the holiday and endless headlines out of the Middle East, it sure seemed to with high anxiety in the markets. The anticipation of the ceasefire with Iran and all the positioning around it was the main culprit I’d say and we’re still not sure where we stand at week’s end.

The Strait of Hormuz is still not re-opened. Iran blames Israel’s attacks on Lebanon as the reason for the muted ceasefire. Vice President Vance is heading to Pakistan for additional talks with Iran and to clarify the so-called misunderstandings. While there are high hopes for an agreement, it seems the risk is also higher for a re-escalation.

With the tone of rhetoric out of the White House, I believe President Trump is looking for an off-ramp that initially came via the Pakistan Prime Minister offering up a two-week extension “from” Iran. However, the situation remains extremely fragile with Israel’s unpredictability the most likely to spoil the quasi-truce.

As oil and fuel prices remain high back home as politicians prepare for upcoming primaries and the mid-term elections, the pressure is increasing on the Trump Administration to bring the focus back to domestic issues important in the immediate term with voters.

US Consumer Price Index for March rose 3.3 percent year-over-year that was up considerably from February’s annual 2.4 percent increase. Fuel prices are one of the most visible costs to consumers as it is necessary on a weekly basis for transportation and also factors in quickly to increased food and utility prices. Higher fuel costs are one of the biggest threats to triggering softer consumer spending in the weeks and months ahead.

Energy prices also increase inflation and threaten Fed interest rate cuts with the next FOMC meeting on April 28-29th. With the end of the school year and summer travel plans only one month away, these higher costs will likely impact the extent to which plans remain as airfares will also be increasing unless a resolution is reached in short order.

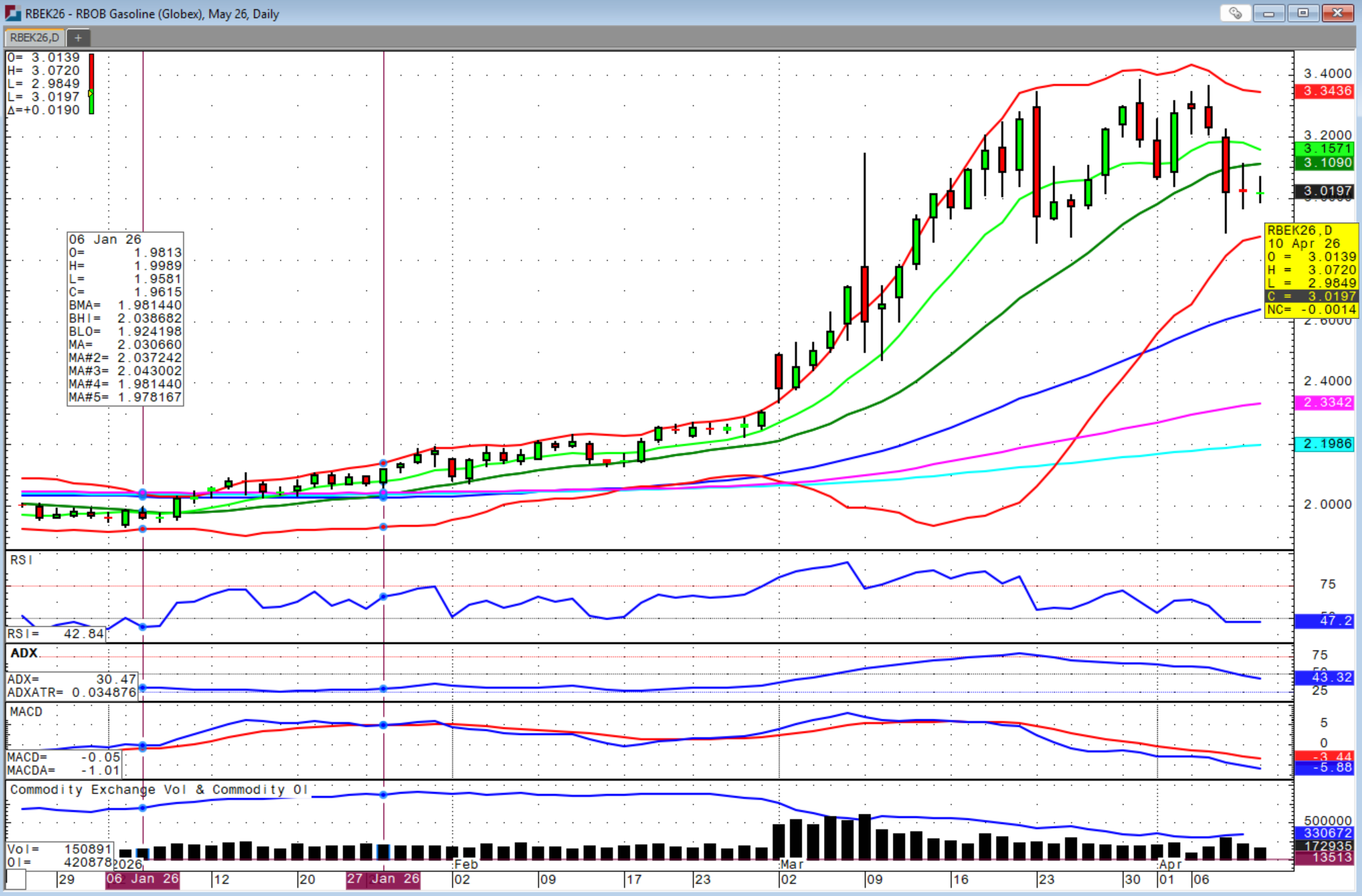

The US dollar plummeted this week after weeks of stronger trade and the softness will be a tailwind for commodity contracts.

Surprisingly, oil prices have remained fairly muted, all things considered, as has the stability of the stock market. Even if oil prices do not trade back into the $70s or $80s, as long as we stay below $100 per barrel, I think the overall market will absorb an ongoing shock in stride.

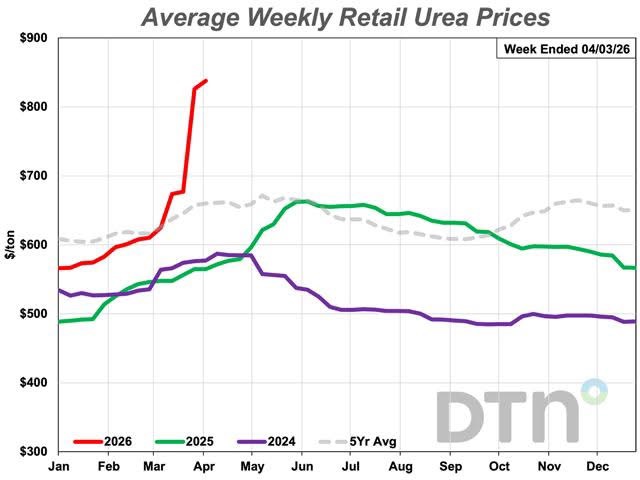

For agriculture however, the elevated costs of fuel and fertilizer are going to be a critical factor if they remain elevated. With US winter wheat harvest about 6-8 weeks away and row crop planting underway, fuel and fertilizer usage will soon be increasing. Urea prices have surged with supplies limited and even seeing delays in even a price being offered in some cases. Even if the Hormuz Strait were to reopen next week, facilities have been damaged and there is a large backlog of ships that will take weeks if not months to sort out.

Source: DTN

The threat of continued US bombings is an incentive for the Iranian regime to make a deal, but the situation is also becoming more vulnerable for the Trump Administration as boots-on-the-ground is becoming more of an inevitability should the fight continue. The threat of the Iranian regime to the world is undeniable, but the immediacy of many pressing issues for US voters also cloud the importance they place on greater expense and involvement there.

For agriculture markets, the war premium still supporting oil markets is waning for grains. The first national winter wheat rating released on Monday afternoon showed US ratings at only 35 percent Good-to-Excellent versus 42 percent expected and compared to 48 percent last year. This put US winter wheat ratings below the 5-year average and the lowest level in 3 years and the 3rd lowest of the last 8 years for early April. Spring wheat planting has started, but one percent below expectations and the average.

In the central and southern part of Oklahoma, we are hearing that many producers where wheat is being adjusted out at 5-7 bushels per acre or below and will not be harvested. However, the wheat market didn’t find much support from this bullish surprise.

USDA’s Crop Production and WASDE reports released on Thursday at 11 AM added to the downside pressure in wheat with both US and world ending stocks increasing more than expected due to increased production in Russia, the EU and Argentina.

US corn plantings are reported as 3 percent complete, in line with expectations and ahead of last year despite some concerns about wetness delaying planting due to heavy rains. It is still early, but the next 3-4 weeks will be critical if any weather delays persist.

The USDA kept US corn and soybean ending stocks unchanged from last month despite expectations for a slight increase. Global corn stocks increased more than expected. Global soybean stocks were reduced while a slight increase was expected.

Brazil and Argentine corn and soybean production was unchanged from last month while slight increases were expected. Brazil’s soybean harvest is in its final stretch and is in line with the average and so no issues there. Brazil’s first corn crop harvest marginally behind average. With bioethanol and biodiesel production in Brazil from corn and soybeans increasing, there is some optimism that increasing production there will not all land on the export market to compete with US exports. However, the expansion of biofuels will unlikely keep pace with the expansion of acres being added each year in Brazil.

While many have been expecting soybean futures to sell of given the large Brazilian crop and questionable US exports to China given rising trade tensions, old crop futures prices kind of broke out higher on Friday. We could see some continuation into this next week based on Friday’s close.

The wheat and corn markets need help after a tough couple of weeks. Depending on the coverage of this weekend’s rains in the Southern Plains, we will know more about the immediate fate of the wheat market. The corn charts need some weather premium and export demand to factor back into the mix with the charts looking pretty ugly as planting is underway.

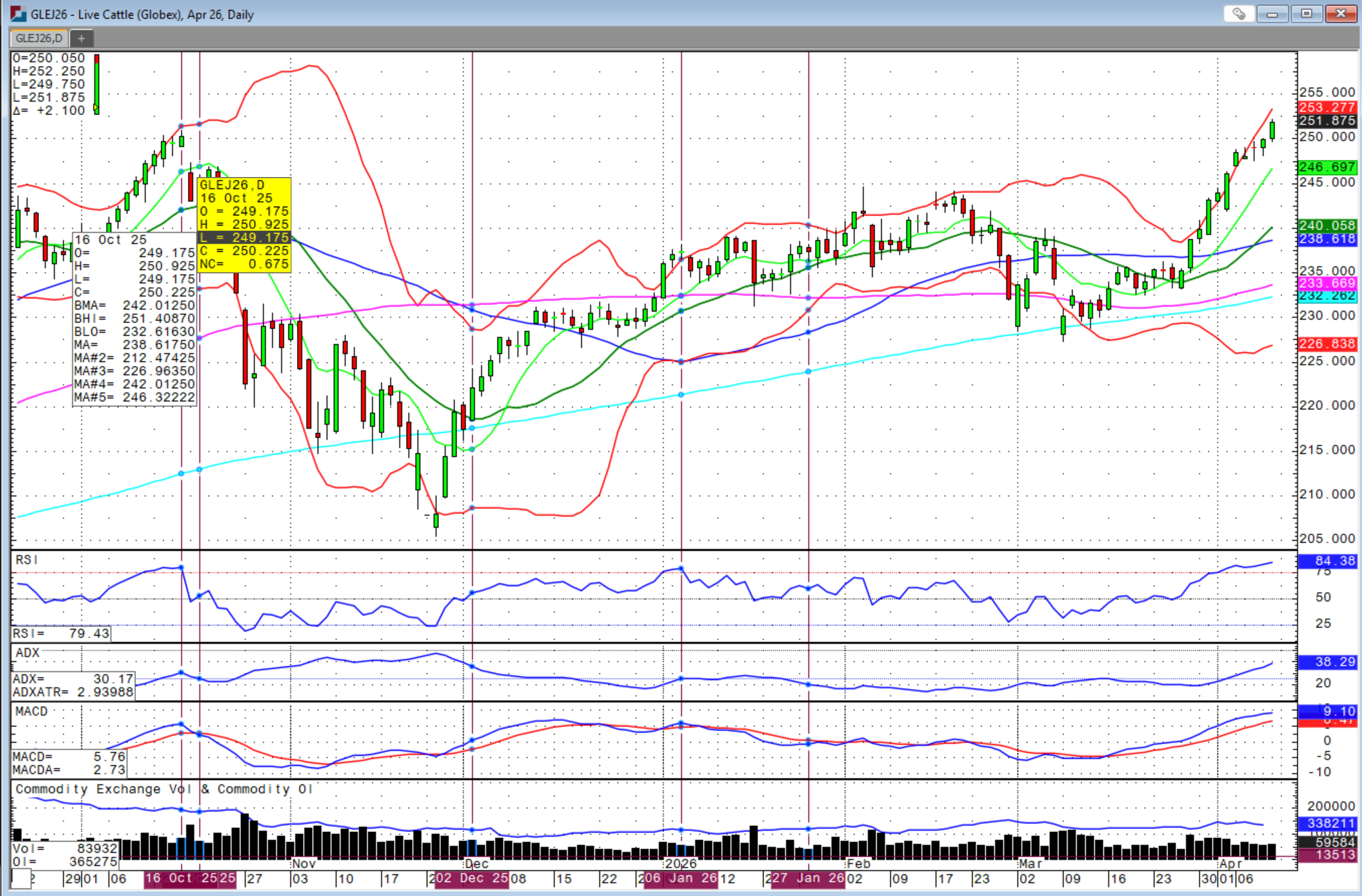

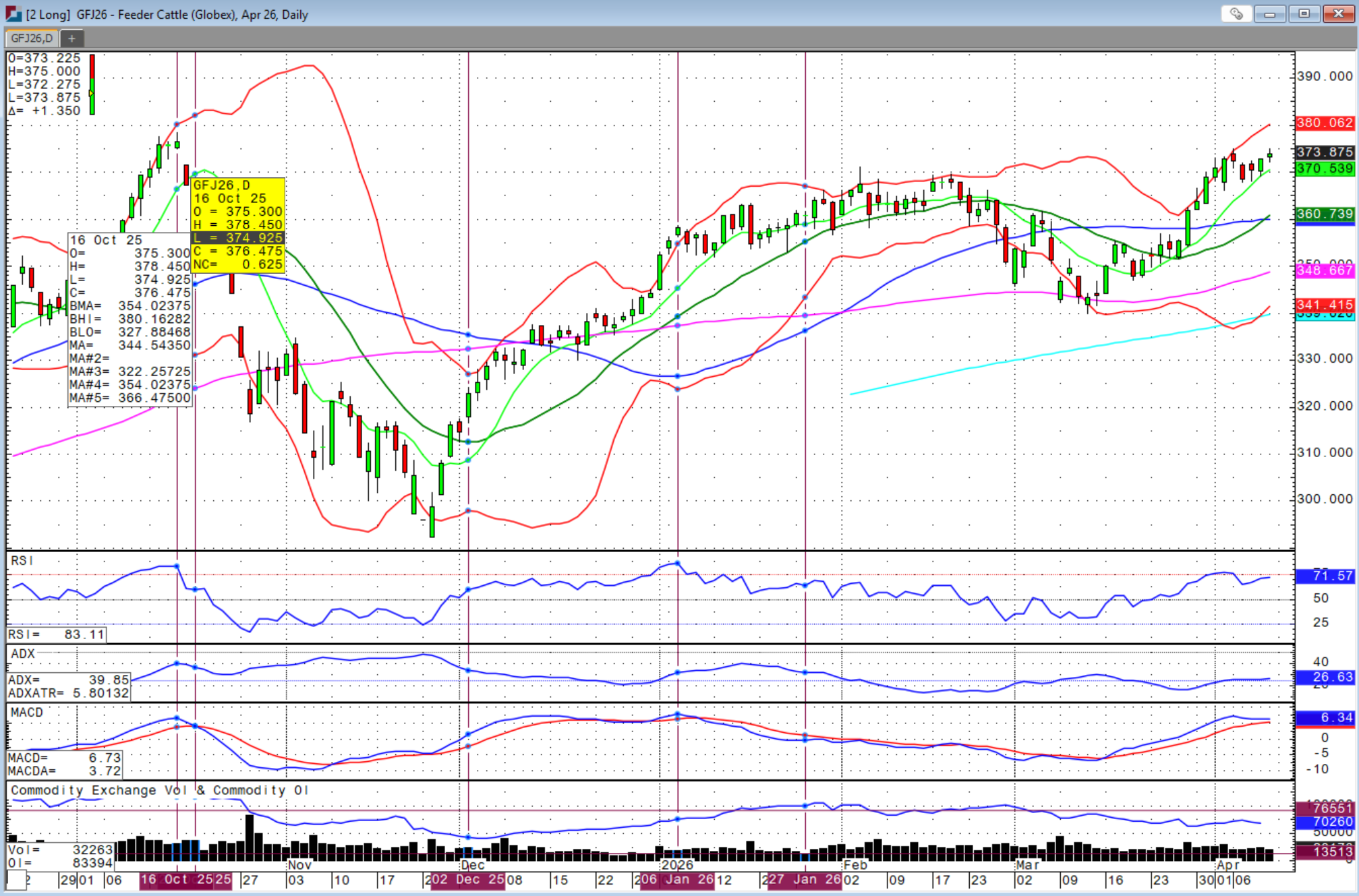

Weaker corn prices have helped provide support to the cattle complex that bottomed one-month ago. Several more feeder chart gaps were filled on Friday with light, fed cattle cash trade. However, the trade that did occur was higher than last week’s $10 per cwt jump over the prior week. The fed cattle cash trade this week peaked at $249 in Kansas. I would expect to see $250 next week that may be strong resistance.

Fed cattle futures made new, all-time highs on Friday. If fuel prices can ease or at least show signs that they could ease in the weeks ahead, this could be a major supportive factor for the cattle complex. However, the insatiable appetite of American consumers for higher priced beef may finally capitulate if fuel prices continue to remain high and increase further. I think cheaper energy prices up until now and more remote work and less driving have increased the disposable income of consumers to spend on beef.

That financial situation is now changing rapidly with higher fuel, food and utility costs. I believe we will see all feeder chart gaps filled next week and we could see new, all-time highs with fed cattle futures already trading above previous highs. Feeder futures reaching $380 could very well be in the cards and then we’re going to have to see if the overall market can sustain these levels.

Be aware that these elevated prices could again spark political rhetoric and even the reopening of the Mexico crossing with Arizona. This level is a second bite of the highest future price levels and so be ready for anything to trigger the market for another leg higher or a double-top.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/Visa%20Inc%20gold%20card-by%20hatchpong%20via%20iStock.jpg)