Consumer tech stocks have been shuffling lately, and smaller hardware names have been hit especially hard. When buyers get cautious and smartphones continue to improve, companies that rely on one main product can quickly find themselves under pressure.

That is undoubtedly the challenge GoPro (GPRO) is facing right now. The action camera maker’s sales have slumped as budget-conscious buyers and smartphones eat into its market. This week, GoPro announced a major restructuring. According to the announcement, the company will axe about 145 jobs, nearly 23% of its workforce, by year-end to save costs. The layoffs will roll out through late 2026, with roughly $11.5-$15 million in severance and benefits expenses. The move is aimed at slashing overhead after several unprofitable years.

For investors, the question is whether this deep restructuring can help GoPro protect profits and set the stage for a comeback, or whether it is another sign that the company still has a long road ahead.

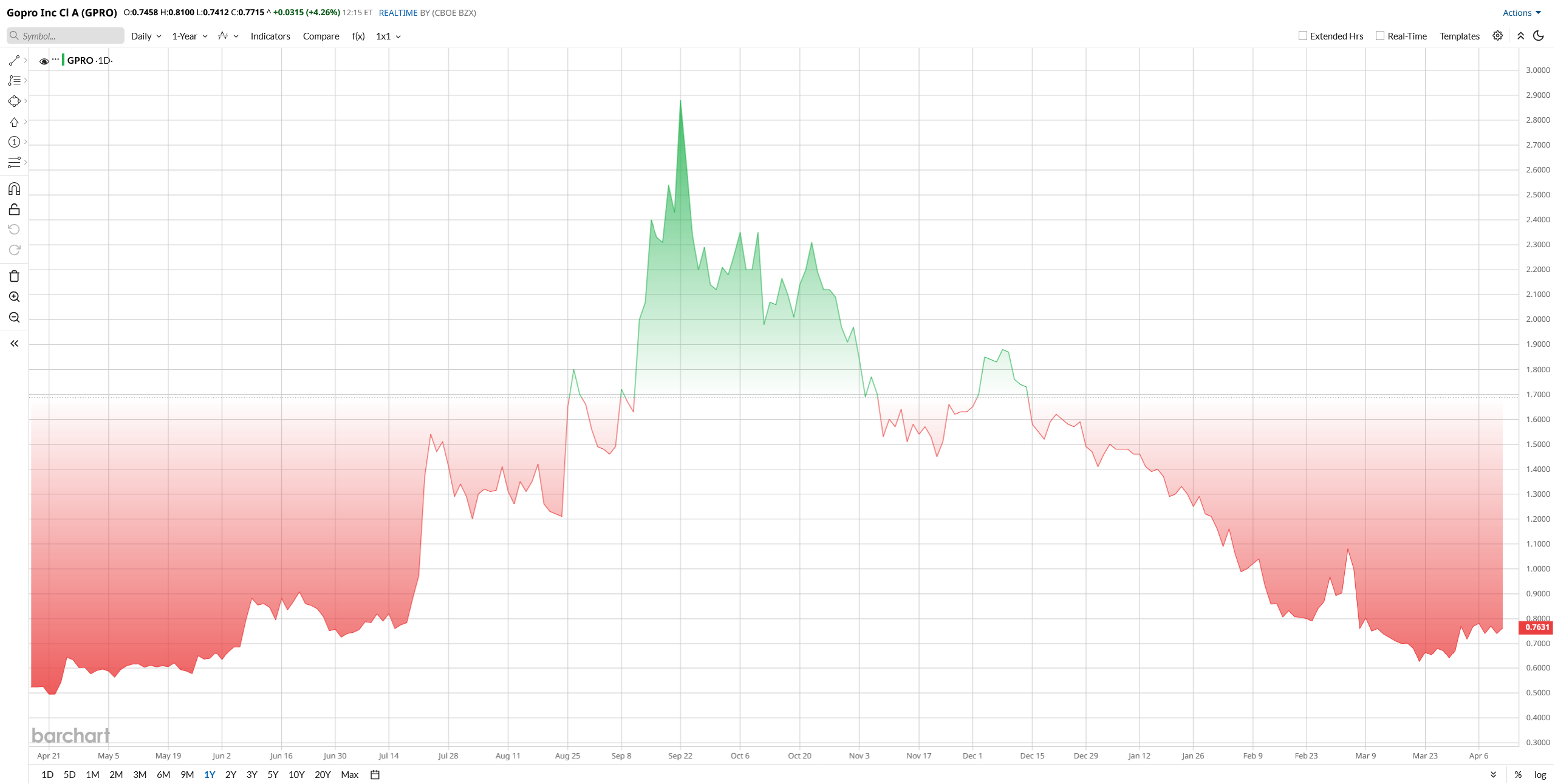

How Did GPRO Stock Perform?

GoPro is known for its rugged, waterproof action cameras and related gear. It also offers video-editing software and a growing subscription service for cloud storage. Once a fad favorite for sports and travel, GoPro has struggled in recent years against smartphones and cheaper cams. CEO Nicholas Woodman returned to lead the company in 2022, aiming to revive the brand with new tech like AI-enabled camera chips.

GPRO stock has had a pretty rough year this year. It plunged about 45% year-to-date (YTD) due to weak sales and skepticism. In early April 2026, it traded near $0.75, a low level not seen since 2020, but investors' hopes for a pullback on hopes that cost cuts and new products will help.

On paper, GoPro looks extremely cheap. Its market cap is only a few hundred million, while annual revenue runs in the high hundreds of millions. Price-to-sales is well under 1×, far below typical consumer-tech averages of 3x. The company is still loss-making, yet trades at a deep discount to both its history and peer benchmarks, but that cheapness reflects very low growth expectations.

Revenue Flat but Losses Narrow Sharply

GoPro’s latest quarter suggests the business may finally be stabilizing, even if growth is still difficult to find. Revenue came in at $201 million, roughly flat from a year ago. Camera unit sales dropped sharply to about 625,000, but higher pricing and product mix helped offset the decline. Retail sales were a bright spot, rising to nearly three-quarters of total revenue, while direct-to-consumer sales slipped.

The bigger story is profitability. GoPro dramatically reduced its losses, reporting a net loss of $9.4 million compared to a much steeper loss last year. On an adjusted basis, the loss was minimal, and EBITDA even turned slightly positive. That’s a meaningful shift, driven largely by aggressive cost cuts.

Cash flow also improved, giving GoPro more breathing room without burning through its reserves.

Looking ahead, management is betting on its upcoming GP3 processor to power a more premium camera lineup. The goal is simple: move upmarket and compete on quality, not just price.

For 2026, GoPro expects revenue between $750 million and $800 million, with results hovering around breakeven. It’s progress, but the real test will be reigniting growth.

Make-or-Break Year for GoPro

GoPro’s 2026 depends on the new GP3-powered cameras, expected in mid-year. If these work as planned, they could boost sales and margin. Woodman also mentioned expanding GoPro’s presence, noting that GoPro cameras are flying on NASA’s Artemis II mission, which is one of the best marketing highlights.

On the cost side, the new layoffs should shave millions off annual expenses going forward. Meanwhile, GoPro continues pushing its subscription service; the user base was 2.36 million at year-end 2025. However, with smartphone cameras improving and tech demand weak, the company still faces an uphill battle. The restructuring and new product launches together set the stage; either these moves reignite interest, or GoPro risks more downside if sales don’t materialize.

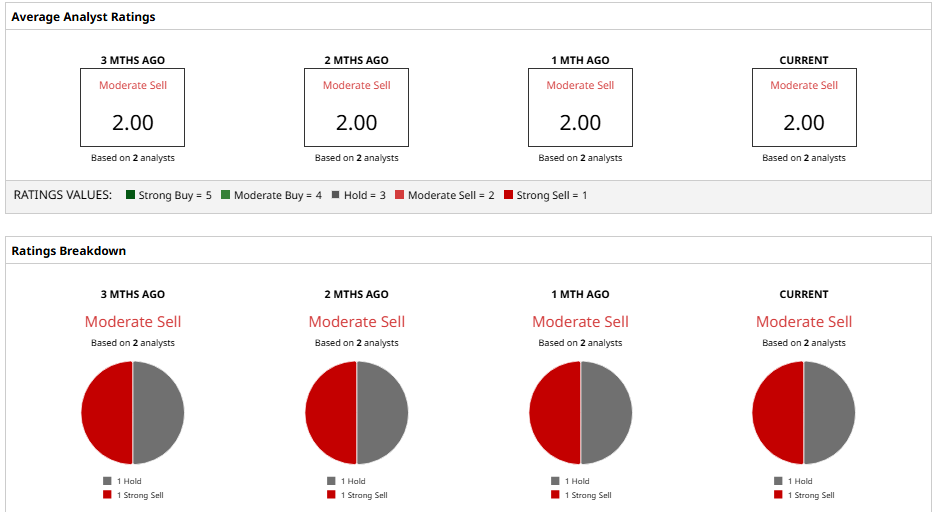

Wall Street's Take on GPRO

Wall Street has generally been pessimistic on GPRO stock. Currently, only two analytics firms cover the stock. One is Morgan Stanley, which reiterated its “Underweight” rating, essentially a “Sell” rating, even as it raised its 12-month price target to $1.30 from $0.80. MS analysts say new products and deals like the Artemis mission and GP3 chip could help, but they still see tough conditions.

The second one is that Wedbush maintains a “Neutral” rating with a target of $0.75, which shows low expectations for unit growth.

Overall consensus is bleak, but the consensus price target is surprisingly optimistic. According to Barchart data, analysts’ 12-month average price target is $1.30, implying a massive 69% upside. That said, there are no bullish outliers right now; most firms expect breakeven or losses.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)