/United%20Airlines%20Holdings%20Inc%20777%20plane-by%20Laser1987%20via%20Shutterstock.jpg)

U.S. airlines have been facing a turbulent period since the Iran war began. With oil prices regularly hovering above $100/barrel (last night's temporary ceasefire has helped bring down oil prices, for now), carriers have been cutting unprofitable flights and passing higher costs to travelers. For example, United Airlines (UNH) said it will trim capacity and raise first/second checked-bag fees by $10 to offset surging fuel costs. At the same time, demand has shown resilience. Chief Commercial Officer Andrew Nocella noted that United has been able to raise fares without hurting bookings. Still, rising costs have hit margins industry-wide.

In this environment, United is also set to report its Q1 earnings on April 21, which will be closely watched. Investors will listen for clues on pricing power, cost trends, and guidance as United competes in the high-cost, post-Covid market.

About United Airlines Stock

United Airlines is one of the world’s largest airlines. It operates a vast route network to over 370 global destinations on six continents through hubs. United served about 150+ million passengers annually on mixed narrow-body and wide-body fleets. The carrier offers full-service amenities, premium cabins, loyalty programs, etc., on domestic and long-haul international routes, making it a bellwether for U.S. airline trends.

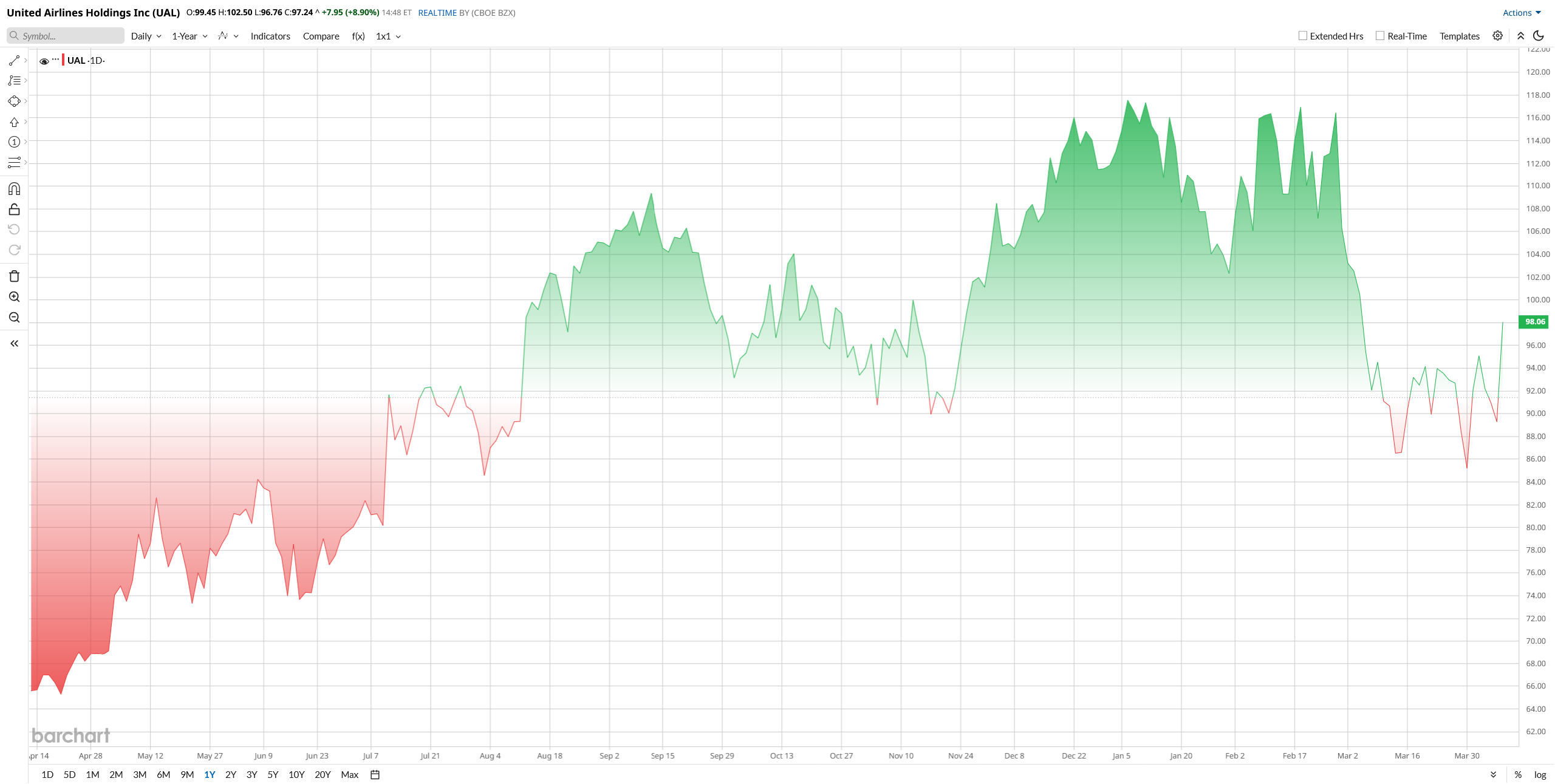

United’s stock has pulled back from early-2026 highs. After trading near $118 in January, UAL slipped into the $85 to $95 range by late March amid fuel and cost worries. Year-to-date (YTD), the stock is 12% down, yet 75% up over the past 52 weeks. The pullback can be linked to higher fuel and labor costs, plus more cautious guidance industry-wide. Overall, UAL’s 2026 drop tracks wider airline weakness even as demand holds up.

Even better, the stock isn't looking cheap considering its impressive growth rate. United trades at a very low trailing P/E of 9×, well below the 21× median of the Industrials sector. However, its enterprise value/EBITDA is about 7.7×, slightly above the airline industry median of 6.3×. If it seems like UAL is inexpensive on current earnings but not extremely cheap on an asset basis.

Upcoming Earnings on April 21

On April 1, United confirmed it will release Q1 results after the market close on April 21 and host a conference call on April 22. Market watchers are focused on how fuel surcharges and labor costs will affect the quarter. CEO Scott Kirby set an upbeat tone in January, saying Q4 2025 was “the highest-revenue quarter in United’s history” with “strong revenue momentum… continuing into 2026”.

Wall Street currently expects roughly $1.19 in adjusted EPS and about $14.2 billion in revenue for Q1. That range sits around United’s prior outlook: the company’s guidance page lists 1Q26 EPS of $1 to $1.5, which implies a midpoint of $1.25.

Over the past year, United has generally met or modestly beaten estimates. For example, in Q4 it delivered a record $15.4 billion in revenue, 3.5% YoY, and $3.10 in adjusted EPS, coming in at the upper end of its $3 to $3.5 guidance range. Management’s full-year 2025 EPS of $10.62 was up 8% from 2024.

Looking ahead, Wall Street surveys imply relatively muted top-line growth for Q1, as on-year demand was very high in 2025. Investors will watch closely whether United can hold fares up or if traffic falls short. The 2026 outlook is complicated by oil price swings. Morgan Stanley analysts note airlines may provide broad guidance ranges this year because of fuel uncertainty.

United’s earnings call on April 22 will be crucial. Any surprises on fuel hedging, capacity changes, or international demand could swing the stock, as airlines often see 5% to 10% swings on earnings.

Recent Company Developments

Several recent moves set the stage for Q1 results. On March 27, United announced a tentative five-year contract with its flight attendants union, the last of its big labor pacts, promising industry-leading wage hikes and a $740 million signing bonus.

In partnership news, United continued building its “Blue Sky” alliance with JetBlue (JBLU). In February, United and JetBlue enabled joint cash bookings and loyalty redemptions on each other’s websites. This cross-selling arrangement expands United’s network strength (especially leisure routes) and broadens loyalty options. Later enhancements, rewards, and perks, new joint vacation packages are planned for 2026.

Wall Street Opinion on UAL Stock

Analysts remain generally bullish on UAL, though 2026 estimates have been pared back. For example, BofA Securities recently raised its UAL target to $145, up from $130, citing strong demand and a beat in Q4 revenue/EPS.

Goldman Sachs lifted its target to $135, highlighting United’s better-than-expected Q4 results and positive Q1 guidance. UBS has a $147 target after calling the company’s latest results “strong”.

By contrast, firms like Jefferies and TD Cowen have more moderate targets around $118 to $140 after trimming estimates in light of fuel costs.

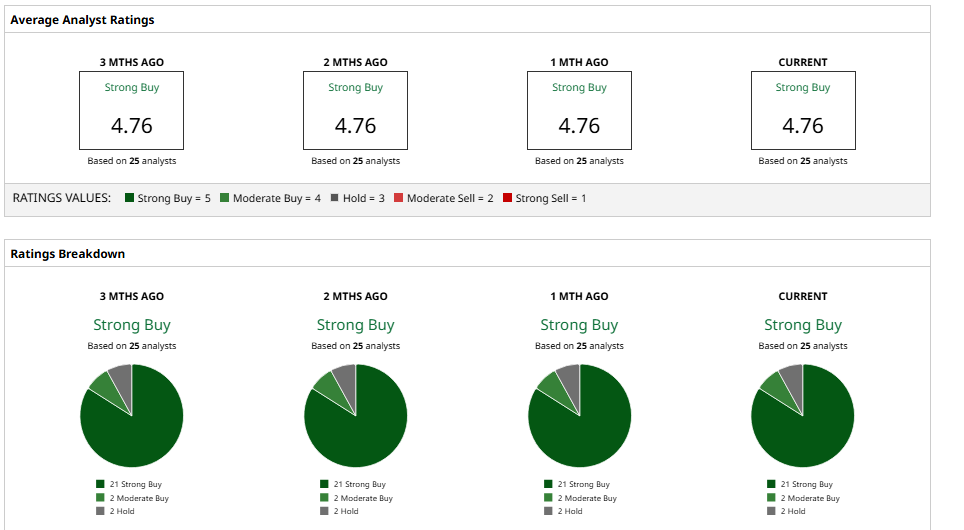

The consensus among 25 Wall Street analysts is a “Strong Buy” recommendation. In fact, Barchart reports a consensus 12-month price target around $130, roughly 34% above the current price. In other words, Wall Street sees considerable upside if United can deliver on its 2026 strategy.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)