On Monday, the U.S. Treasury announced its designation of The Bank of New York Mellon Corporation (BK) as the financial agent to implement the newly created Trump Accounts program, established as an IRA in One, Big, Beautiful Bill, signed into law by President Trump. Big Wall Street banks had thrown their weight behind Trump Accounts, possibly hoping to be chosen as the accounts manager. While the contract itself is not a moneymaker, it comes with millions of new customers whose wealth might grow over time.

BNY partnered with Robinhood Markets (HOOD), in which capacity the fintech would serve as a brokerage and initial trustee for the accounts. Additionally, Robinhood and the U.S. government's National Design Studio are working on the Trump Accounts app.

The tax-deferred investing accounts for children born between 2025 and 2028 are set to be released on July 4, and include a one-time $1,000 deposit from the Treasury. This was seen as a fruitful opportunity for large employers, as they had earlier pledged to match the Treasury’s seed money for children of U.S. employees.

As Robinhood grabs this opportunity, should you consider investing in its stock?

About Robinhood Stock

Robinhood is a U.S.-based financial technology company that offers a mobile-first trading platform enabling individuals to buy and sell stocks, options, exchange-traded funds (ETFs), and cryptocurrencies. It operates primarily as a zero-commission brokerage platform, generating revenue primarily through payments for order flow (PFOF), margin lending, and interest-bearing cash sweep products.

Also, Robinhood has expanded beyond basic trading to broader financial services, including advisory offerings, expanded banking features, and wealth management and private‑banking‑style products. The fintech has made strategic acquisitions, such as TradePMR, and is now planning to integrate the crypto-focused Bitstamp to strengthen its market-making infrastructure and global crypto capabilities. Headquartered in Menlo Park, California, Robinhood has a market capitalization of $62.82 billion.

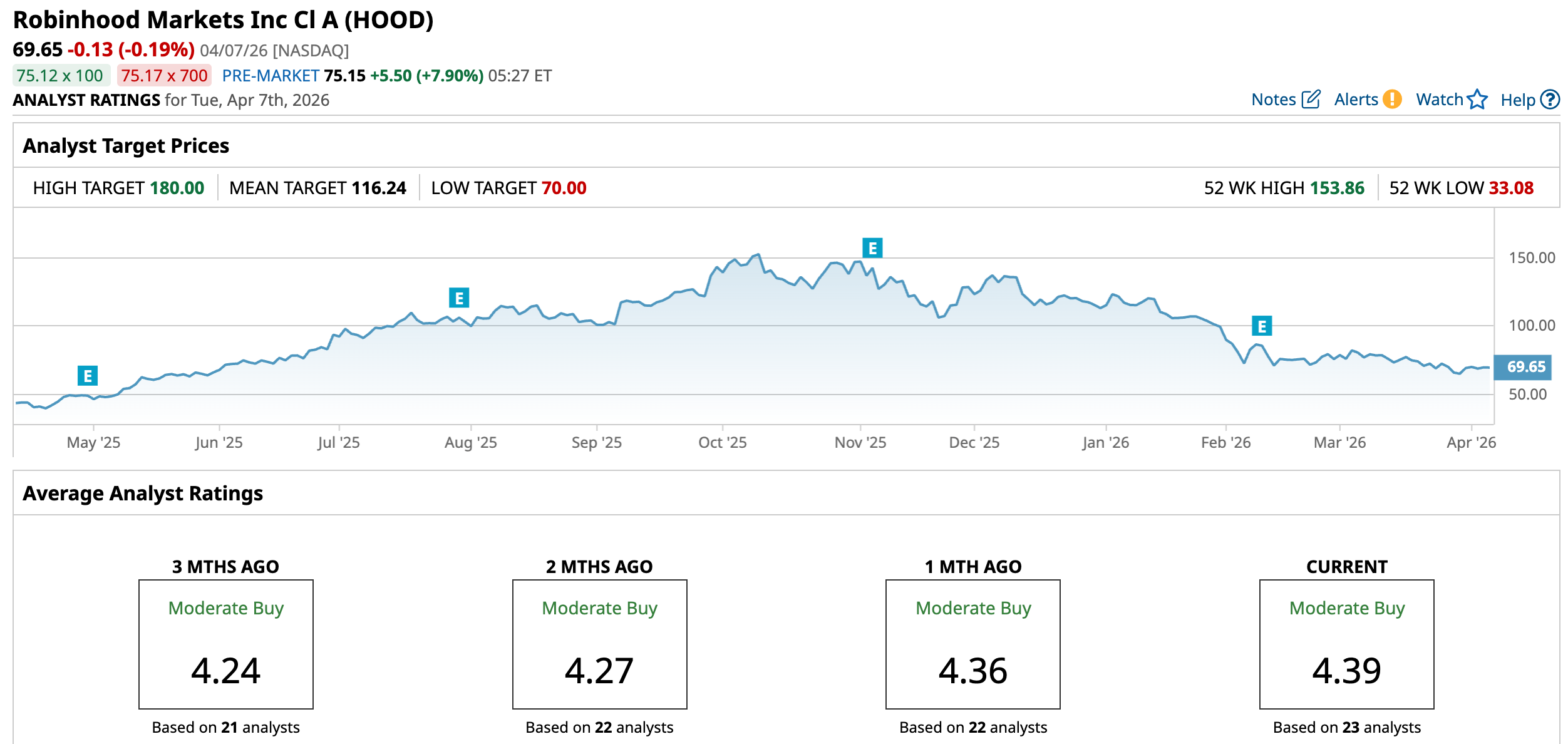

Over the past 52 weeks, the company’s stock has risen 96.7%, underscoring its strong fundamentals. However, it has come under pressure this year, declining 38.42% year-to-date (YTD). The shares had reached a 52-week high of $153.86 in October 2025, but are down 54.7% from that level. While Robinhood’s underlying customer base and long-term growth story look robust, the company is facing weaker crypto-driven revenue and a tougher macroeconomic backdrop.

On a forward-adjusted basis, Robinhood’s price-to-earnings non-GAAP ratio of 27.24 times is higher than the industry average of 10.13 times.

Robinhood Reports Record Q4 Revenue, Profit Beats Expectations

On Feb. 10, Robinhood reported solid fourth-quarter fiscal 2025 results. The total net revenues increased by 27% year-over-year (YOY) to a record $1.28 billion. However, Wall Street analysts had expected revenues to be higher ($1.34 billion). Its transaction-based revenues grew 15% YOY to $776 million, though they were partially offset by a 38% drop in cryptocurrency revenue.

The platform’s funded customers increased 1.8 million, or 7%, YOY to 27 million, while total platform assets rose 68% to $324 billion, driven by continued net deposits, acquired assets, and higher equity valuations. On the other hand, its EPS (diluted) dropped to $0.66 in Q4 2025 in comparison to $1.01 in Q4 2024. Despite this drop, the figure was above analysts’ expected $0.64.

Wall Street analysts are optimistic about Robinhood’s future earnings. They expect the company’s EPS to climb 40.5% YOY to $0.52 for the first quarter (to be reported on Apr. 28, after the market closes). For fiscal 2026, EPS is projected to surge 10.2% annually to $2.26, followed by a 22.6% growth to $2.77 in fiscal 2027.

How Do Analysts Regard Robinhood Stock?

This month, Jefferies analyst Daniel Fannon maintained a “Buy” rating on the stock but lowered the price target from $88 to $84, exhibiting cautious optimism on Robinhood.

And analysts at Needham lowered the price target from $100 to $90, but maintained a “Buy” rating on Robinhood’s stock. As the company’s recent metrics showed a slowdown across its platform, Needham analysts reduced their estimates across nearly every segment for the first quarter of 2026.

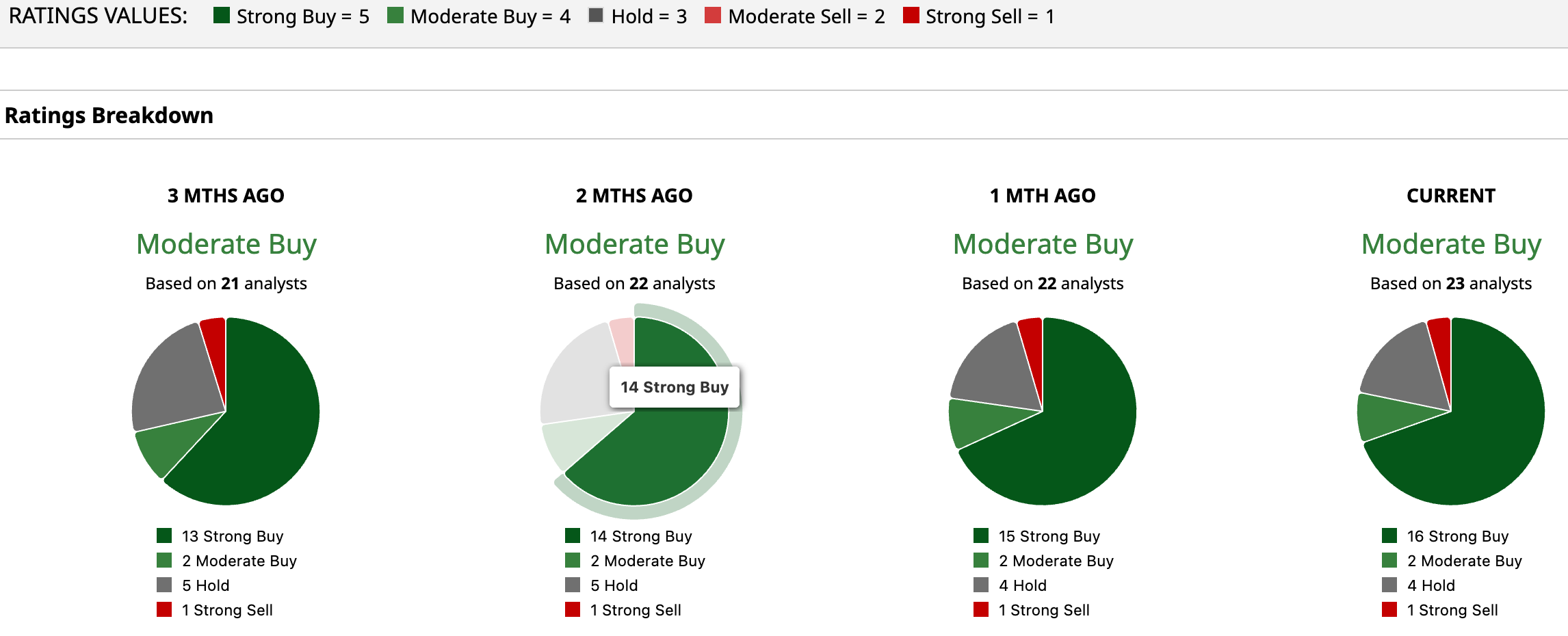

Robinhood is a sound favorite on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating. Of the 23 analysts rating the stock, a majority of 16 analysts have rated it a “Strong Buy,” two analysts suggest a “Moderate Buy,” while four analysts played it safe with a “Hold” rating, and one analyst rated it “Strong Sell.” The consensus price target of $116.24 represents a 66.89% upside from current levels. The Street-high price target of $180 indicates a 158.4% upside.

Key Takeaways

Robinhood’s solid fundamentals and growth prospects position the stock favorably. Moreover, landing this deal with BNY and Trump Accounts reflects well on the company as it tries to build the “Financial SuperApp.” Therefore, it might be worth looking into the stock now.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)